I’ve been following the blog for a while and I’m excited with my first post to share my financial goals and future with you guys

I’m very curious to hear your thoughts on the financial future for myself and my soon-to-be wife.

I (M31) am a Swiss citizen and my fiancé (W31) is a US citizen with a B-Permit in Switzerland. She can apply to the C-Permit hopefully soon and then would switch from the “Quellensteuer” to the regular tax. Current situation:

We both live in Baselland

My gross wage is CHF 122k and hers is CHF 66k

We bank with UBS, as other banking options are too frustrating for a US person

We both have an individual account and also a shared account

As of right now we do not have any significant amount in savings or investments

Goals:

Enough financial safety net for family planning

Equity for a house

FIRE

Money Distribution:

I was thinking of managing the finances this way

20-25% of our individual monthly income goes into an individual tax savings account

90% of the remaining income goes into our shared account

ALL expenses are being paid with the shared account, therefore we can hold each other accountable

ALL the savings / investments will go from our shared account

10% of the remaining income we can keep to ourselves for personal fun which does not involve the other person (e.g. hobbies, tech gadget for me, etc.)

Order of Operation:

Create an emergency fund of CHF 10k (3x monthly expenses)

Max out Pillar 3a (US citizen might be a problem, see later)

Invest via IBKR

I hope this was somewhat easy to understand and to follow . Since my fiancé is a US citizen, certain things won’t be as easy and I hope people with some experience can help answer some questions.

Questions:

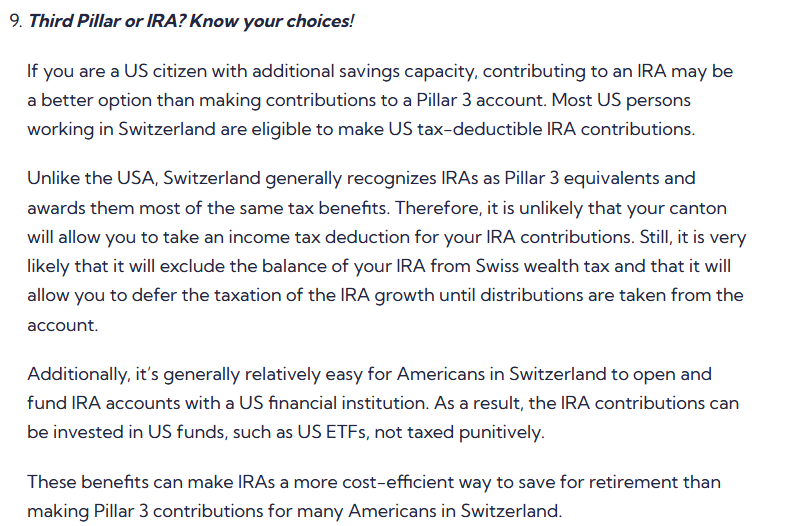

VIAC is the only provider so far that has agreed to accept my fiancée due to her citizenship. Does anyone have experience with VIAC for “US-Persons”?

Could she potentially profit by investing in the American RothIRA?

What makes the most sense, since she (once we are married we, I assume) have to declare and pay US taxes?

I’ve read that she has the option to file US taxes separately rather than jointly. Is this true, and would it make sense given that her salary is likely lower than mine?

What should we keep in mind, given our situation?

Thank you for taking the time to read my post, and I eagerly await your insights and suggestions on our financial journey.

EDIT: I forgot to mention that I would also close any pension gaps!

Good to know, was not aware that the “Quellensteuer” would go away for her once we are married.

Yes, I currently have accounts with BLKB and UBS, all of which are still under a student discount that will expire soon. We would pay CHF 15 a month for the UBS family plan, which covers both individual and shared accounts. I really appreciate UBS’s e-Banking for its ease of transferring money between accounts and managing the credit card. For the sake of simplicity, I plan to close the BLKB account and consolidate my banking with UBS for everyday needs and Revolut for travel.

Having a house with a garden is something we always wanted, it’s not something we choose because everybody else talks about it

Based on the other recent thread, I’d say you definitely don’t want to file jointly if you want to keep investing in non-US securities (e.g. pillar3, UCITS ETFs, etc.)

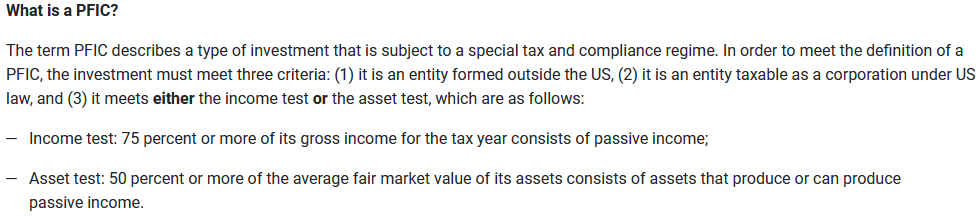

Obviously not an expert here but would the Pillar 3a count as a taxable corporation? I was hoping to invest into the 3a for her not only for retirement but also to lower our taxable income… so if I couldn’t lower our Swiss income, could we potentially lower her income with the Roth IRA?

@WayneWealth

Are you going to take the green card or are you staying 100% Swiss?

If you have the green card will you have to pay taxes in the USA even if you live and work in Switzerland?

If she is soon your wife, does she need a C permit or can she directly ask for the swiss passport ?

Not applicable to me but I think(!), if she would file her US taxes jointly, I would have to pay US tax as well, ergo the move to file seperatly for her.

Also not an expert in that regard but I’m quite sure she would not pass the language or the integration treshhold for the Swiss citizenship yet. Therefore the C-Permit.

Will keep this thread updated if I find some new / interesting information, I‘m sure in the future an other couple in the same situation would also love to read through some experiences!

And if anybody else has some wisdom, I‘m eager to learn

I think in general with that income, you can either have a house with garden eventually and retire normally (maybe a few years earlier if you save agressively) OR fire, but not both.

Thanks @Tony1337, I guess given our current financial situation that is a more realistic approach.

Especially because kids are planned in the future I really want to make sure that the money we have goes to a good place and I can make sure we can have a great future! I don’t see a salary increase in the near future, therefore my focus currently is on slashing our expenses down as much as possible and optimising as much as I can for the whole US tax situation.

Would anybody know, if we use my and my fiancés money and invest it on IKBR under just my name, would that be any problem from a tax perspective? As a Swiss I profit from the Swiss capital gains tax and as an American my fiancé has no foreign investments and therefore has nothing to tax on.

Your comment about buying a home is similar to renting it in terms of cost intrigued me. So I wanted to look for data. I knew that this was the case 5 years back but I think “ownership discount” has significantly eroded over the years. It is now actually a premium. If you look at the annual report from Credit suisse at link below, page 11 shows the ownership premium at its highest level

It could be that your mortgage was concluded at a very attractive rate and hence for you personally it’s still a very good deal. However I believe for new mortgages this might not always be true. As with most real estate markets this depends on the area too.

If the rates go down again, this balance could change.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.