The HSLU (Lucerne University of Applied Sciences) has published a study with the title “Study on saving and investing: Why money often stays in the account”. Unfortunately only in German. Found the numbers in it interesting. Maybe someone else will find it interesting too!

In den vergangenen 30 Jahren erzielten Aktienanlagen in der Schweiz eine durchschnittliche Jahresrendite von rund 8 Prozent (unter Annahme reinvestierter Dividenden). Spargelder hingegen wurden im gleichen Zeitraum lediglich mit knapp 0.9 Prozent pro Jahr verzinst.

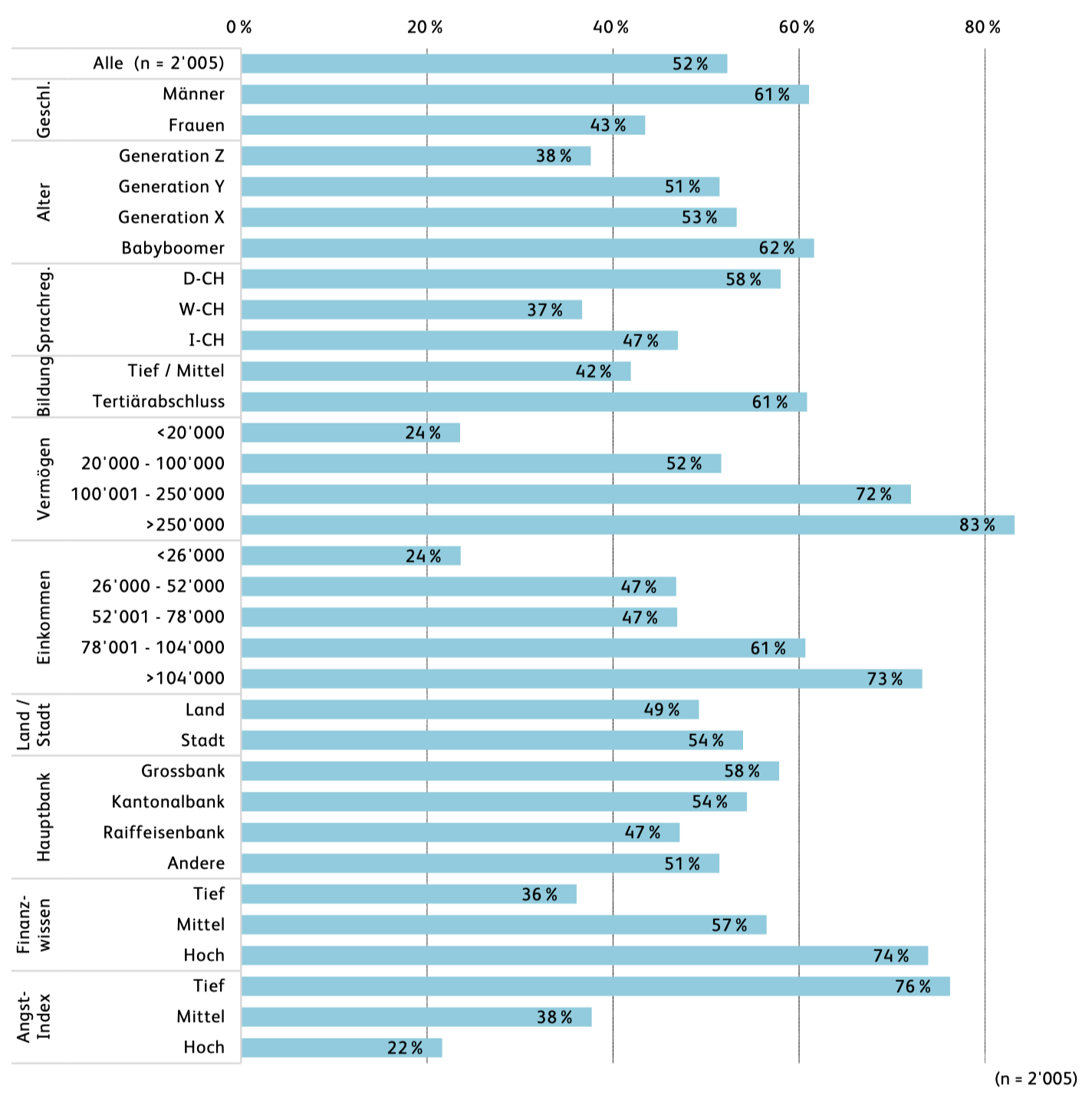

Der Anteil der Investor:innen unter den befragten Personen liegt bei 52 Prozent. Dieser Wert entspricht in etwa den Ergebnissen früherer Befragungen und bewegte sich in den letzten Jahren je nach Befragung zwischen 49 und 52 Prozent.

Die Ergebnisse der Befragung zeigen, dass 61 Prozent der Männer, aber nur 43 Prozent der Frauen investieren.

In der Deutschschweiz ist der Anteil der Anleger:innen deutlich höher als in der Romandie oder im Tessin. Zudem legen Personen, welche in städtischen Gebieten wohnen, häufiger an als Personen auf dem Land (54% vs. 49%).

Personen mit Tertiärabschluss investieren deutlich häufiger (61%) als Personen ohne Hochschulbildung (42%).

Personen mit hohem Finanzwissen legen deutlich häufiger an den Finanzmärkten an als Personen mit geringen Finanzkenntnissen.

Personen mit wenig Angst vor Verlusten investieren deutlich häufiger als Personen mit viel Angst (76% vs. 22%).

Personen mit höherem Einkommen und Vermögen investieren häufiger als Personen mit geringerem Einkommen und Vermögen.

Tendenziell investieren ältere Generationen häufiger als jüngere. Von den Befragten der Generation Z investieren 38 Prozent. Bei der Generation X und Y sind es 53, respektive 51 Prozent. Am höchsten liegen die Werte bei den Babyboomern, welche zwischen 61 und 79 Jahren alt sind (Stichprobe ist beschränkt auf Alter bis 79 Jahre).

74 Prozent der befragten Personen (vor der Pension) sparen über die gebundene Vorsorge (vgl. Abbildung 3). Die rund drei Viertel aller Personen teilen sich auf in 34 Prozent, welche lediglich ein Säule 3a-Konto haben und 40 Prozent, welche innerhalb der Säule 3a auch in Wertschriften investieren.

A feq quotes (English, translated with AI)

Over the past 30 years, equity investments in Switzerland have achieved an average annual return of around 8 percent (assuming reinvested dividends). Savings deposits, on the other hand, earned only about 0.9 percent per year over the same period.

Among the respondents, 52 percent identified as investors. This figure is roughly in line with previous surveys and has ranged between 49 and 52 percent in recent years, depending on the survey.

The survey results show that 61 percent of men invest, compared to only 43 percent of women.

In German-speaking Switzerland, the proportion of investors is significantly higher than in French-speaking Switzerland or Ticino. In addition, people living in urban areas invest more often than those in rural areas (54% vs. 49%).

People with tertiary education invest much more frequently (61%) than those without higher education (42%).

People with strong financial knowledge are far more likely to invest in financial markets than those with limited financial literacy.

People with low fear of losses invest much more frequently than those with high fear levels (76% vs. 22%).

Individuals with higher income and wealth tend to invest more often than those with lower income and wealth.

In general, older generations invest more frequently than younger ones. Among respondents from Generation Z, 38 percent invest. In Generations X and Y, the figures are 53 and 51 percent, respectively. The highest levels are seen among baby boomers aged between 61 and 79 (the sample is limited to respondents up to age 79).

Seventy-four percent of respondents (before retirement) save through the tied pension system (see Figure 3). Of these roughly three quarters, 34 percent have only a Pillar 3a account, while 40 percent also invest in securities within Pillar 3a.

The statistical graphs in the study are also interesting.

I think it is important that so many people keep their cash in CHF, EUR or USD. Inflation needs to be fed! For me I like to say what makes people shout at me: cash is trash!

Cash is debt and everybody holding cash helps the debtor because the unit controlling cash is targeting a bigger than zero inflation. I never hold cash bigger than my debt in any currency.

Now, money is a nice thing and I like to have a lot of it… covered by debt just to make it a zero game for me.

The two links posted are already summaries of the study. And the study itself also contains an introduction. And I have already posted a few quotes from the study

I do wonder which direction the causation is for some of these

that phrasing makes it sound like obtaining this knowledge causes someone to invest. But my knowledge of financial markets has definitely increased substantially due to my investing

same with this one, my fear of losses has definitely moderated as my financial literacy has improved once i started investing

Yeah, they didn’t write about this in the study (checked the full one behind the summary).

But also, education itself did not have a significant effect when other factors were controlled regarding overall probability to invest vs not invest. That basically means that the effect you see that people with higher education invest more, is primarily due to correlated features such as higher income (makes sense) and not due to a direct link of education → investment.

Some of those conclusions don’t sound too surprising, such as if you are financially literate, have a high income and don’t mind taking risks, you are more likely to invest.

However, while the title highlights that many people don’t invest, I’m rather surprised how many do. Some 50% do and some 75% have 3a according to the study.

I would have guessed even lower numbers, and for 3a even read about it somewhere (hat lower number might have been max 3a amount, not 3a in general, though).

That surprised me too. I read the following in the PDF:

Der Anteil der Investor:innen unter den befragten Personen liegt bei 52 Prozent (4)

Then I thought: Well, probably enough people invest within 3a unknowingly, so it seems rather low to me. And then I read the Footprints and was even more surprised:

(4) Anlagen über die Pensionskasse und die Säule 3a ausgeschlossen.

I can’t imagine that 52% of my family and colleagues invest in stocks and co. But perhaps it’s because people in Switzerland don’t talk about money and investing (except buying a house).

I’m surprised, too. Almost none of my friends (excluding one former Google work colleague who became a friend) invest.

When the topic (of investing) comes up even with my friends who could invest, the reaction mostly ranges from “it’s just gambling” to “none except the rich can afford it”.

Latter quote comes from a family who live in a low rent apartment in a beautiful Art Nouveau 3 apartment building that they will inherit probably within a decade or so (which explains the low rent, too: the wife’s mother owns the property).

The building comes with a huge garden (more than 500 m2) on a quiet 20km/h zone (“Spielstrasse”) in the city of Zurich. I’m guessing the property including the building is worth well north of 10M CHF. The heiress will have to share the inheritance with her brother.

The husband shared with me that he once (about 15 years ago) invested a significant amount of CHF (maybe 70k?) into the CAD based on a tip from a friend of his. He’s still waiting to get even, but he won’t sell his CAD until he’s at least getting his CHF money back. Loss aversion at its best.

But yes, certainly, only “the rich” can afford to invest.

Former quote comes from a couple whose wife is a former member of the Zurich city parliament as a member of the SP. She’s best friends with Jacqueline Badran, which I why I unfortunately regularly get to meet Jacky (which is how her friends and acquaintances call her). Anyway …

The couple mentioned at the start of this paragraph inherited part of their parents’ also Art Nouveau 4 really large – each flat is about 200 m2 – apartment building with a slightly larger surrounding of about 1300 m2 (some of it garden, some of it garages and open parking space).

On another tangent: they inherited the property in 2011 – via Erbvorbezug – before the previous inheritance tax initiative was voted on (in 2015, when inheritances above 2M CHF would have faced a 20% tax, retroactively back to January 1 2012).

Off tangent: I guess their property – shared across 3 heirs/heiresses – has a current market value of many times the one mentioned above.

When the parents actually died a couple of years ago, the heirs also inherited a low 7 digit stock portfolio. They asked me to take a look as “there are some really nasty – gruusigi – companies in there, like oil companies like Chevron or Exxon”. I was on vacation in Africa at the time and didn’t even get their message. So their bank rep “cleaned” things up instead and – for a small fee – traded all the individual stock holdings for an ESG product sold by the bank.

To add injuries to insult: shortly after, the couple bought a gas powered car to have an easier transport option to the properties they own or rent now (beside the partial ownership of premium property described above):

a chalet home (owned) in the nearby mountains above Lake Uri

a flat (rented) in the old town on the Rhine river in Bale

a modern flat (owned) in St. Moritz

a multi-apartment building (owned) in the center of the city of Zurich where they (part-time) live in one of the flats

So, uh, yes, most of my friends don’t invest, even the ones who could.

I guess technically they invest (their inherited moneys), but only in real estate. Not the worst choice in CH and if you don’t need to be liquid, ever.

To round off the picture, most of my friends aren’t like that. Many are in the category that either just don’t know at all (about investing) or actually do not have spare cash to invest or prefer to spend a couple of months off every couple of years for e.g. touring Africa in their Toyota Land Cruiser (with an air intake snorkel and a roof top tent). These are my real friends, I think.

Does anyone see in the study how the value of how much people invest was determined? There is a nice graphic, but it is not clear to me which specific question was asked.

In einem ersten Schritt wurde untersucht, wie viele und welche Personen in der Schweiz an den Finanzmärkten anlegen. 3

3 Der Anteil der Anleger:innen wurde basierend auf folgender Frage erhoben: «Sind Sie im Besitz von Wertschriften (z.B. Aktien, Fonds, Obligationen, etc.; ohne Anlagen in 3. Säule, ohne Pensionskasse)?»

If I own just one worthless share, according to statistics I am already invested. That’s true, of course. But it’s not particularly meaningful… I would find a question like “Have you invested more than 25% of your wealth?” more interesting. On the other hand, the study also examines access. From this perspective, it can be said that 52% have somehow access to a stock exchange.

Off topic, but if you have parents or in-laws that once in a while start dinner-table small talk like “oh do you still remember Beat or Ursula? You once played together when you were 3. I ran into the parents and they told me how well XYZ’s business is doing”: you could now return the small talk and casually mention those 8-digit real-estates your cohort is starting to inherit and see the reaction.

(only sounds entertaining if they don’t have big real estate, of course)

Getting a bit off-topiccy, but just to ask, do I understand correctly that these “poor” people got their inheritance “ins Trockene” just before this potential Erbschaftsinitiative and thus tax would have been introduced? (That initiative was very strongly rejected IiRC). That initiative very likely came from Jacky & her friends, amd takes years to get to referendum , so could Jacky have mentioned it once (or twice) for them to “get a move on with that inheritance / Vorbezug ”?

Well, I suppose, why not, what else should one talk about over dinner?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.