Looking at the current stock valuations worldwide (except maybe Italy, Russia and Brazil) it feels pretty scary to invest into anything. I was thinking does it make sense to follow this strategy:

Decide on your asset allocation, for me it would be like 80% cash and 20% stocks.

Divide the 20% into five ETFs: USA, Europe, Japan, Pacific, Emerging markets.

Invest once in a year only in ETFs that are the cheapest in terms of the current CAPE ratio, below 20 or so.

Yearly rebalancing consists only in keeping the cash/stocks ratio of step 1 constant by selling the ETFs with currently highest CAPE ratio.

In this way you allow any weightings among the five ETFs, but always buy the cheapest and sell the most expensive. I know it’s not conventional, but does it make sense for the beginner? It seems like this way you keep the trading costs down and psychologically it feels better to buy cheap.

I’m just afraid to buy something expensive now, which will only be falling in the next years.

if you are so sure about it, why would you not buy some inverse ETFs?

What you need is a clear rule how your asset allocation looks like. that rule might contain CAPE-dependent stock fractions, but all in all, if you have to adjust you rule because CAPE is high, then your Asset allocation does not match your risk tolerance => decrease stocks%, and don’t increase it back once CAPE is low.

i am pretty confident that in case CAPE actually falls in the next decade, dividend payments alone will outperform cash. but this is only personal believe

I think you mistake asset allocation with risk and risk profile (from your writings i understand that by asset allocation you mean “allocating a fixed/constant portion of your portfolio in a certain asset class”).

Unfortunately, these are really not the same thing.

Even if someone has a “conservative” 60/40 stocks/bonds allocation, it can perfectely happens that his portfolio is quite risky.

For instance, if your bond part is invested in long term swiss government bonds, then you are in for a surprise when the rates will start hiking and the bonds will lose money.

Same for the stocks. Assuming all other things are constants (especially company earnings), I would argue that stocks are much less risky with a low CAPE ratio than a very high or like currently.

One can intuitively understand that a stock is less risky if you buy it at 20% discount of the intrinsic value of the company, than if you buy it at a 20% premium over the intrisic value. You have much more to lose if you are in the second case, and if the long term price of the stock converge to the value of the compny, then you WILL lose money in the second case.

In this example we find out that the asset class is not enough to define the “riskiness”. The price paid for an asset matters a lot as well (and it may well be that a lot of other factors matter as well).

So if risk cannot be strictly equivalent to an asset class, I do not think an asset allocation alone could be equivalent to defining a risk tolerance profile.

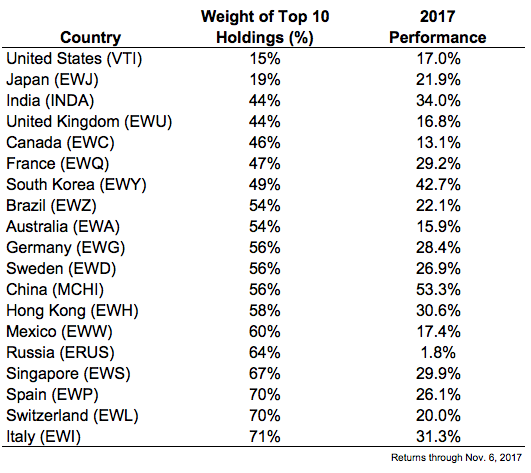

And please consider the fact that you can’t compare CAPE between countries really…particularly when emerging markets are considered. Not every country reports earning the same way, and not every stock exchange has the same acceptance rule for companies. Before doing any strategy based on international cape, dig deeper on how cape is calculated for every country /region you are looking for.

Too much work honestly. Follow the KISS rule ( keep it simple & stupid)

this stuff is VERY heavy into energy, natural resources, financials and little into everything else - quite unlike S&P, if that’s your mental model for a random country’s stock market. Probably ok to buy as a commodities play though (I know a few people who, like you, scream market is overpriced to the moon and buy nothing but commodity companies these days, i’m sure they’d be delighted to invest in russia, but the truth is probably somewhere in the middle and in a good balance of everything)

I wouldn’t invest in such risky countries in a single ETF anyway, only in a total EM ETF.

My question was actually about the validity of the strategy described above, which in my view is a version of rebalancing as there you also buy the cheaper stuff and sell the expensive.

As I’m learning and thinking what kind of investment style makes sense to me I come to the question of why people suggest that you have a constant ratio of elements in your portfolio within the risky stock part. And the answer I come up with is that it seems that everyone it creating their portfolios by backtesting. And you can only backtest if you have a static asset allocation where things are kept in certain proportions through the whole period of time. You can’t backtest any dynamic strategy.

And exactly how do you decide what’s cheap and what’s expensive? And more importantly why should the metric you use be better than the market’s estimation?

Sure you can, it’s just a matter of what data you have. Good data costs good money though. 90+% of most data analysis is data preparation and cleansing

In my naivety I’m only using the country’s CAPE ratio and the current price relative to the average price of the ETF in it’s existence. I use data from these websites and I have no way of knowing what quality this data is:

It’s not really a valid indicator to compare countries with each other: it’s affected by currencies, interest rates, inflation as well as market composition. E.g. russia is little more than oil and gas exporter, it deserves a shitty valuation.

3 Likes

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

{kind=link}