i would like your point of view of adding a bond component to my portfolio. I am struggling to take a decision and i’m not sure how to proceed, i am looking for an opinion exchange and hopefully to have some doubts cleared out

current asset allocation:

95% Stock (VT, 3a with Viac and Finpension both with global100 strategy)

5% Crypto (= BTC, it’s the only fun money part)

Investing strategy:

Monthly DCA: I started investing 5y ago and the only market crash i experienced was covid, even though it did not bother me since my invested capital was not that high to be scared of the loss.

Thoughts:

I am based in CH, the VT and chill strategy was good at the beginning, where i was accumulating my net worth. Due to future uncertainty (having a kid or not) i’d rather preserve my capital, trying to optimize for the worse scenario rather than for the best → hence, should i add a more conservative bond component? I’m not risk adverse but every time we reach an ATH and markets are greedy i tend to think more conservative rather than excited

Doubts:

I’d pick bond ETFs (long term: BNDW / SEGA… short term: IBGS), i am just not sure if it’s better a short term bond ETF (to park cash) or long term bond ETF where you are kind of speculating on the interest rates.

I would like a “safe” option to reduce volatility of my VT and chill strategy and growing my bond component for a 80-20 strategy)

are you picking long term or short term bond ETF for the bond portfolio component?

would you keep a cash component for a bond allocation or a short term 0-3 bond ETF knowing that if you keep the bond ETF at least for the average duration you get back the expect yield?

Currently i am at 77% stock, 13% Crypto (did not sell yet) and 10% Bond aka 2nd pillar in that case, i usually don’t like to count it as a Bond component since is not liquid and it would not allow me to rebalance it. But still… i keep this in mind as well

In my opinion “safe” time you need to hold a bond etf to guarantee the initial yield is 2X the duration. Obviously it depends on what is the interest rate hike, what is the initial yield and how much is duration.

How much bonds to hold to manage volatility comes down to individual risk tolerance. Many people will have different views. But it would be mostly be their own position and would not help you much. I think if 100% stocks is making you worried, you should start adding bond allocation knowing following

you will have lower gains in long term in terms of probability.

bond ETFs would also fall in value if interest rate j creases. However #1 will dictate how long you need to hold.

you can start with 20% and see because you need to remain consistent. Otherwise you will always feel you are making a wrong move at wrong time

most investment managers hedge their bond allocation. So something to think about. There are some regional and global ETFs with CHF hedging.

I notice you don’t count your 2nd pillar. Most likely because it’s locked and have a minimum guaranteed return too. It’s alright. But perhaps that should give you a bit more confidence to hold a higher percent of stocks.

I used to pursue a 60/40 strategy for close to a decade shortly after the Great Financial Crisis (GFC).

For the bond portion I initially held some fund (with high fees …) tracking Barclay’s Global Aggregate Bond Index* (Global Agg or just Agg in finance speak). For rebalancing the 60/40 portfolio I later added BND and BNDX as well as VDET instead of further buying/selling the initially selected high-fees fund.

Gradually got rid of the high-fee fund as I abandoned my 60/40 strategy and ventured into stock picking.

Still holding on to BND, BNDX and VDET, will probably keep them for now, mainly for psychological reasons.

For parking cash I used to use BSV. Not risk free, but good enough for me at the time. Sold them all as my appetite further grew for stock picking.

Can’t really advise you on what bond ETF to pick as you don’t say much about your investment horizon and your literacy in financial instruments. But then again, even if I knew more about you, I’d hesitate to give you advice on what strategy to pick and what instruments to use.

Good luck!

* Now it’s called the Bloomberg Global Aggregate Bond Index. It’s essentially market-cap weighted “all” intermediate term US traded (includes non-US debt) investment grade corporate debt plus government debt, mortgage-backed securities (yeah, those from 2008/9 GFC … ) and asset-backed securities.

Two comments:

1)

Having a kid should not really impact your asset allocation. You should never have to touch your savings. Make sure you have a big enough emergency fund to feel comfortable. Make sure you can afford a child with your regular income.

2)

If your bond allocation part is less that 100’000 (not including 2nd pillar), you could also think about keeping it in a savings account instead of buying a bond ETF. Preferably with a bank with state guarantee (cantonal bank). Make sure it’s in CHF.

It’s illiquid,* but you can think of pillar 2 as bonds that never go down and that have a government dictated (for the mandatory part) positive, low return, and at retirement suddenly become liquid or provide you with a (mostly) fixed, guaranteed return.

From your perspective though probably something far in the future more relevant for retirement planning than for current near and mid-term future life planning, potentially with a child?

* Except if you’re looking into a mortgage, or if you plan to leave CH.

i am 35, quite far away from the Swiss retirement age and not planning to leave CH. The interest in bond (not counting on the 2nd pillar) was just to decrease drawdown and be able to rebalance without adding extra cash if needed.

From your (age)* point of view I also wouldn’t count in my pillar 2 for short and intermediate term financial planning.

* I’m about 20 years older,** my kid is an adult and is about to become financially independent of me, and I do consider pillar 2 as an increasingly essential part of my financial (mainly retirement) planning.

totally agreeing with you, to be honest i was looking at AGGS as well (global aggregate bond currency hedged chf) but Ben Felix (yes i trust him) says there’s no evidence that currency hedging is better than non currency hedged… so i always come back at square one. On top of that it’s true that my future expenses will be in CHF but at the same time i am exposed to CHF with my salary and my 2nd pillar. I find the bond component way more complex than stocks

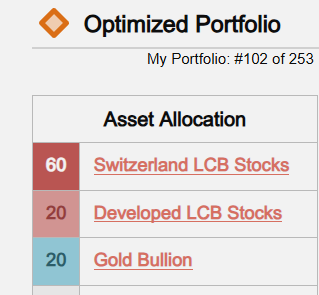

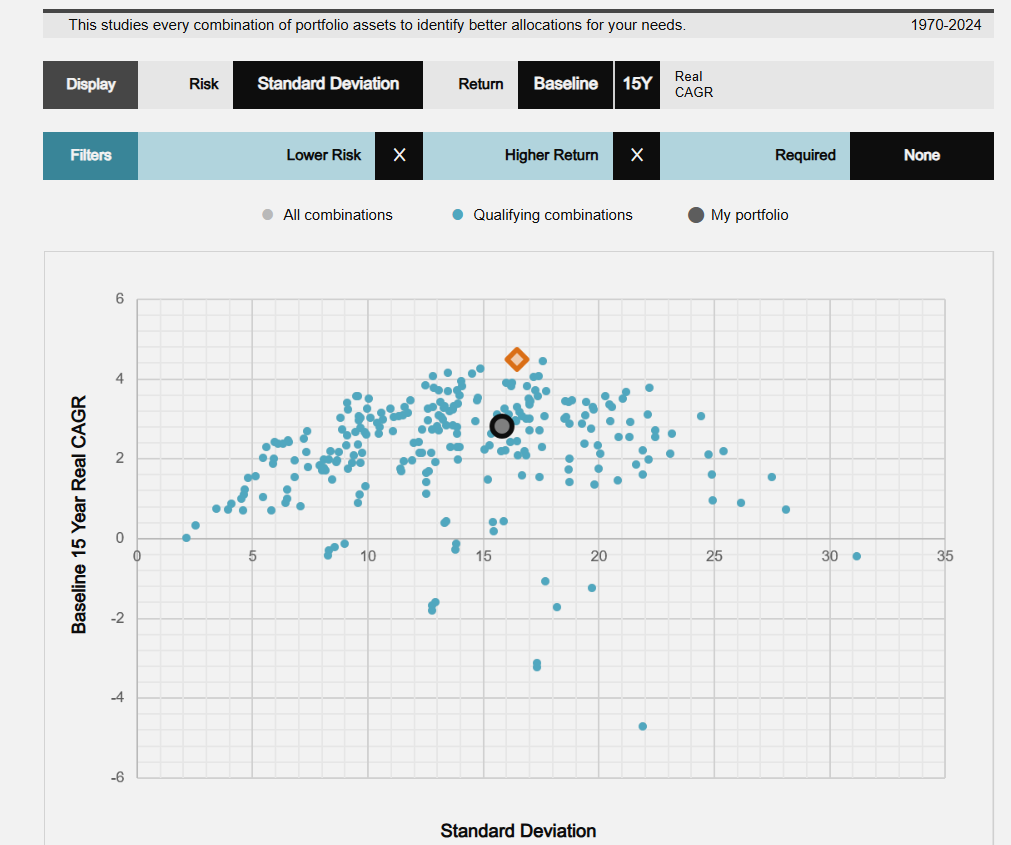

I tried to use Poltfolio charts to see what do they recommend as highest return portfolio based on history. Its interesting that it suggests a very high Swiss home bias. This is shown as yellow marker on the chart.

I was using 75% Global stocks (5% Swiss, 63% DM, 7% EM), 5% Gold, 15% Bonds , 5% Cash as input. The portfolio is shown with grey circle in chart

Has anyone used this tool before? Not sure if I am doing something wrong. The results are a bit weird.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.