Someone having a 50/50 portfolio wanting to replace it with a 100/100 and expecting similar drawdowns, will have a bad time of course.

On the other hand someone having say a 100% VT portfolio and replacing 20% of it with this fund, will not have a materially different drawdown experience, as it has similar volatility.

Or someone already being 60/40 VT/bonds, could replace 20% VT with it and then having 20% of an alternative 3rd asset instead of bonds i.e. managed futures or gold or similar. You’d still be 60/40 stocks bonds, but would have 20% exposure to a diversifying/uncorrelated 3rd alternative that way.

Which is also completely reasonable and suitable for the majority of people.

You could do it the other way round and have real bonds and then buy mostly equity futures, but there you are pretty limited in markets and especially in the US they are tax inefficient. And you have the taxable coupon payments.

That‘s what Pimco does with their stock plus funds.

If you otherwise wanted a leveraged product, you would need daily leverage reset swap etfs and there we are talking about something very different. Think SSO/TMF kind of thing in a single fund (while tmf also only being long bonds for example)

Not sure about the TER. The prospectus allows them to charge 95bp + trading costs. Maybe they use a lower one initially as the fund is new, don’t know. But I’d conservatively assume 95bp + trading cost as that’s what they seem to be allowed to charge.

Yes, you can rebalance the portfolio back to 100/100. The stock physical/ futures part may need to be adjusted though. Also, not sure what realized gains/ losses mean for distributions and taxes however (and how the futures are treated anyway). And, as described in the prospectus, rapid selling assets to acquire necessary margin may need to take place at unfavorable prices, and future markets may experience moments of distress

But I can see your argument, maybe I am a bit pessimistic. I understand the product now better also. For my personal taste I still see too many risks/ unknowns for which I am not fully convinced one is well remunerated for, taking also the high TER into account. Even 56bp “only” is 8 times more expensive than VT…

It is my understanding that those ETFs distribute dividend/income at the end of the year (please tell me if being completely mistaken). What would be a simple and efficient way to achieve total return ?

In a ideal world, I would like the ETF to be accumulating so the burden of reinvesting the yearly distribution (fairly small amounts in my case yet ? What would be the distribution ratio?) into the strategy would not be placed on the investor shoulders.

On the other hand I see that it should not matter that much over time : testfol.io

US etfs sadly can‘t be accumulating, their tax code prevents them from having tax efficient accumulating versions of funds.

Now in the case of RSST, you will have fairly large distributions per year due to them having to distribute basically any and all gains from the futures.

This creates quite a few implications and it‘s also not yet clear how ictax will treat it.

On the futures side you then have 25% S&P 500 futures, that are always long.

This gives you 100% effective S&P 500 exposure.

On top of that goes 100% of their managed futures strategy that aims to replicate the SG trend index (DMBF btw replicates the SG CTA index, small difference)

Now on the distribution side you will therefore have quite some:

The interest on the 25% cash will be distributed as income → fully taxable

the gains on the s&p 500 futures will be 60/40 distributed as long term capital gain & short term capital gains. This is adhering to IRS tax code. For swiss investors this potentially means 60% is tax free and 40% taxable as income. There has been some change in the tax code for us, that treat short term cap gains as income distributions. But it‘s still not fully clear and it may (if we are lucky) be treated as full cap gain and therefore tax free, but I would not count on that.

dividends on the S&P 500 etf, will of course be fully taxable.

distributions on the managed futures: basically simar to the s&p futures. But for example technically commodity futures are treated 60/40 as cap gain/income. This is also IRS specific and ictax interpretation is at their discretion essentially. They do however have shown to interpret it as income with many funds.

So in the end you will have, my guess, 4 (5) different distributions at year end:

interest

dividends

long term cap gains

short term cap gains

(maybe a 5th in income distributions from the commodity futures)

I’m also waiting to see how RS** ETFs distribution ( dividend and cap gains) are taxed in 2024 in ictax. Dividends would be taxed as income and capital gains should be tax free. If things look as expected, and dividends are low (under 2-3%), I’ll be quite interested in them.

Yes, I knew that DBMF was not replicating the same index, but thought it was a good enough proxy.

Would you have an educated guess of what amount we should discount from the portfolio return (i.e. the ?E=x in testfol) to reflect the net-of-tax return ?

I just checked some funds like CTA over the years and cross-checked on the fund websites, what is defined as what.

From 2022 to 2023 something changed and lots of the distribution were classified as taxable.

I think I also remember reading in some federal document the definition of taxation of short term cap gains. But dont have it on hand right now.

Yes, but does this 60/40% rule apply to us in Switzerland? Isn’t the classification cap gain/income relevant for US investors and their tax declaration?

P.S. Okay I think I understand better. I actually had an idea of a similar portfolio, holding cash + futures on stock indices and gold, but never did even a smallest step towards the implementation.

I don’t think it makes that much sense to talk about these without at least touching on the holdings.

options (swap) based daily reset leverage etfs, always lever a single asset up/itself and they will give you the daily return of the levered index x2/3. While stacked funds will have two separate asset classes, one of which is entirely unlevered essentially.

They are also all 2x levered overall.

They will not behave exactly the same way, but they can suffer from volatility decay, if both assets go down at the same time.

But that‘s the catch, it is pretty unlikely that this happens for a long time.

For Upro etc. vol. decay will always happen, as it‘s just one asset.

The swap levered funds are something very different in my opinion.

Those leveraged ETFs are a pretty bad idea (they give you the daily leverage which is ~never what you want, edit: unless you do daily trade and always reset your positions every day).

IIRC there’s some new ETF that work over longer period of time, but you need to invest in them at the start of the period of it to make sense.

From one of the best financial newsletter there is:

The intuition is this. A 3x leveraged ETF is designed to give you three times the daily return of a stock, whenever you buy it. So on Monday morning, say, the ETF price is $100 and the stock price is $100. The ETF gives you exposure to the return of three shares of stock. The stock goes up 10% that day, so the ETF goes up 30%, so that at the end of the day the stock is at $110 and the ETF is at $130. On Tuesday, you buy a share of the ETF. You pay $130, and if the stock goes up 10% again, you want your money to go up 30%. So the ETF now has to give you exposure to more than three shares of stock: It has to give you exposure to three times $130 worth of stock, or about 3.55 shares. And then if the stock goes up 10% again, the stock will end the day at $121 (up 10% from $110) and the ETF will end the day at $169 (up 30% from $130).

To get this result, the ETF has to buy more shares at the end of the day on Monday: It started Monday with each ETF share representing three shares of the underlying stock, but it needs to start Tuesday with each ETF share representing 3.55 shares of the underlying stock. So at the end of Monday it needs to buy 0.55 more shares, to continue to offer three times the return of the underlying stock.

But what if, instead, the stock goes down 9% on Tuesday? Then:

The stock closes at $100.10, down 9% ($9.90) from $110.

The ETF closes at $94.90, down 27% ($35.10) from $130.

So the two-day return of the stock is +0.1%: up 10% Monday, down 9% Tuesday, so from $100 to $110 to $100.10. The two-day return of the ETF is -5.1%: up 30% on Monday, down 27% on Tuesday, so from $100 to $130 to $94.90. The ETF gives you three times the Monday return, and three times the Tuesday return, but negative 50 times the Monday-and-Tuesday return.

I‘m not quite sure what you mean mean with treating the asset class differently?

Futures are one of the least expensive ways to get leverage actually

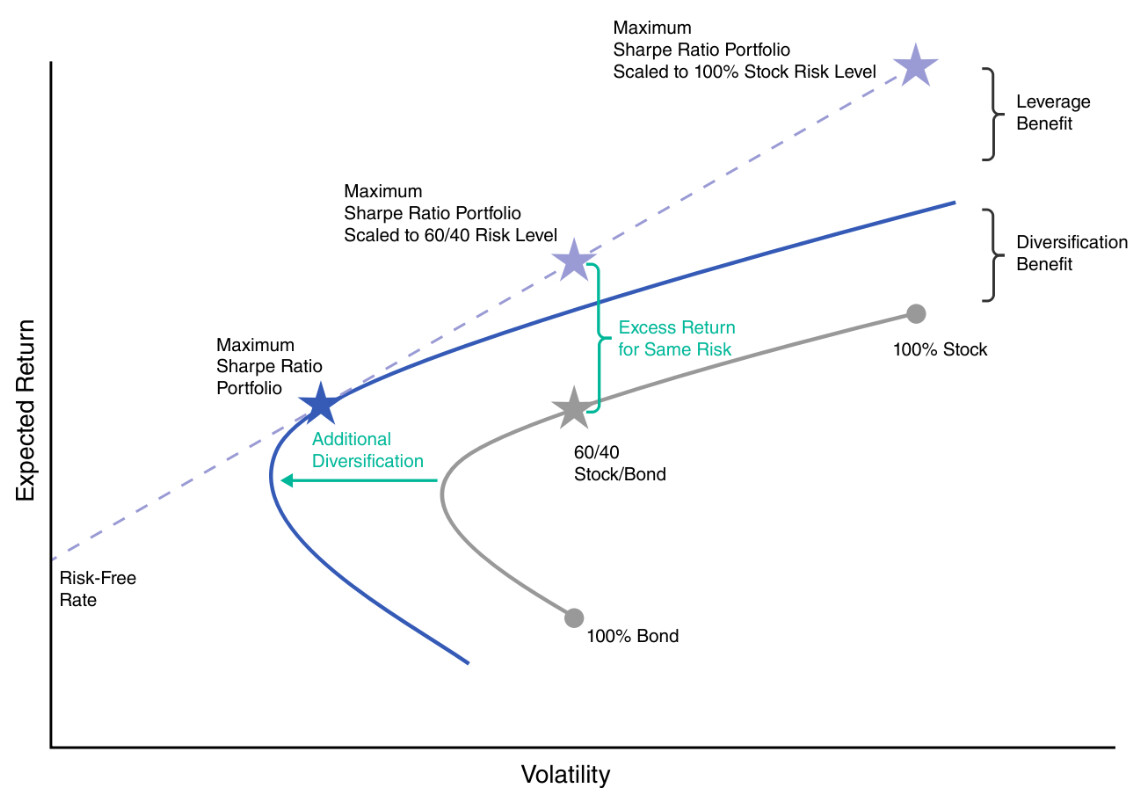

The stacked funds are a very cost effective way to get 100% exposure on one asset class in bonds/stocks and get another 100% exposure in a diversifiyng asset class in bonds/managed futures/carry.

In essence you stack two uncorrelated assets together, while having 100% exposure to both.

You can the use them like lego pieces for your portfolio. You want to keep your 60/40 stocks/bonds? You can do that while adding some managed futures on top for example, as further diversifier.

For example replace 20% stocks with RSST and you get 60/40/20 stocks/bonds/managed futures.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.