I am relatively new to investing and I am looking to rebalance my US. IRA rollover pension (I am a swiss resident and intend to retire in CH). It currently has quite a weighting on BOXX + SGOV to get about 4.5% low risk return on US treasury bonds. I wanted about 30% bond weighting to reflect traditional investment portfolios and lower volatility. But I now realise this doesn’t make sense given FX I’m largely just loosing money, and at 43 I don’t need such a weighting anyway. The rest of the IRA is in VT + VXUS + SCHD. VXUS to reduce us exposure and too much Mag7 weighting, and SCHD as my research at the time suggested this helps diversify from purely growth companies to higher quality companies.

JQUA looked good with 283 holdings with some mid and small cap, vs SPHQ 100 selected from S&P500. But looking at industry weightings and top holdings, JQUA doesn’t really seem to diversiy risk from a possible tech crunch

At the same time, these are all only US holdings and contradicts the choice I made in VXUS, which at least YTD has performed identically to VT…

I do have a separate Swiss private investment portfolio in IBKR (mostly VT + CHSPI) but again a little BOXX which almost certainly doesn’t make sense.

I guess my main question is, as a Swiss investor, what can be done to reduce risk (and returns), or do we really just have to go all in on VT and forget?

Exactly. If you see yourself as a current and future resident of Switzerland, start thinking about your finances in CHF. Short term borrowing rates in CHF are zero, 2 and 3 years interest rate swaps are slightly negative, so no matter how you slice and dice bonds, the return in CHF after fees and taxes is going to be negative.

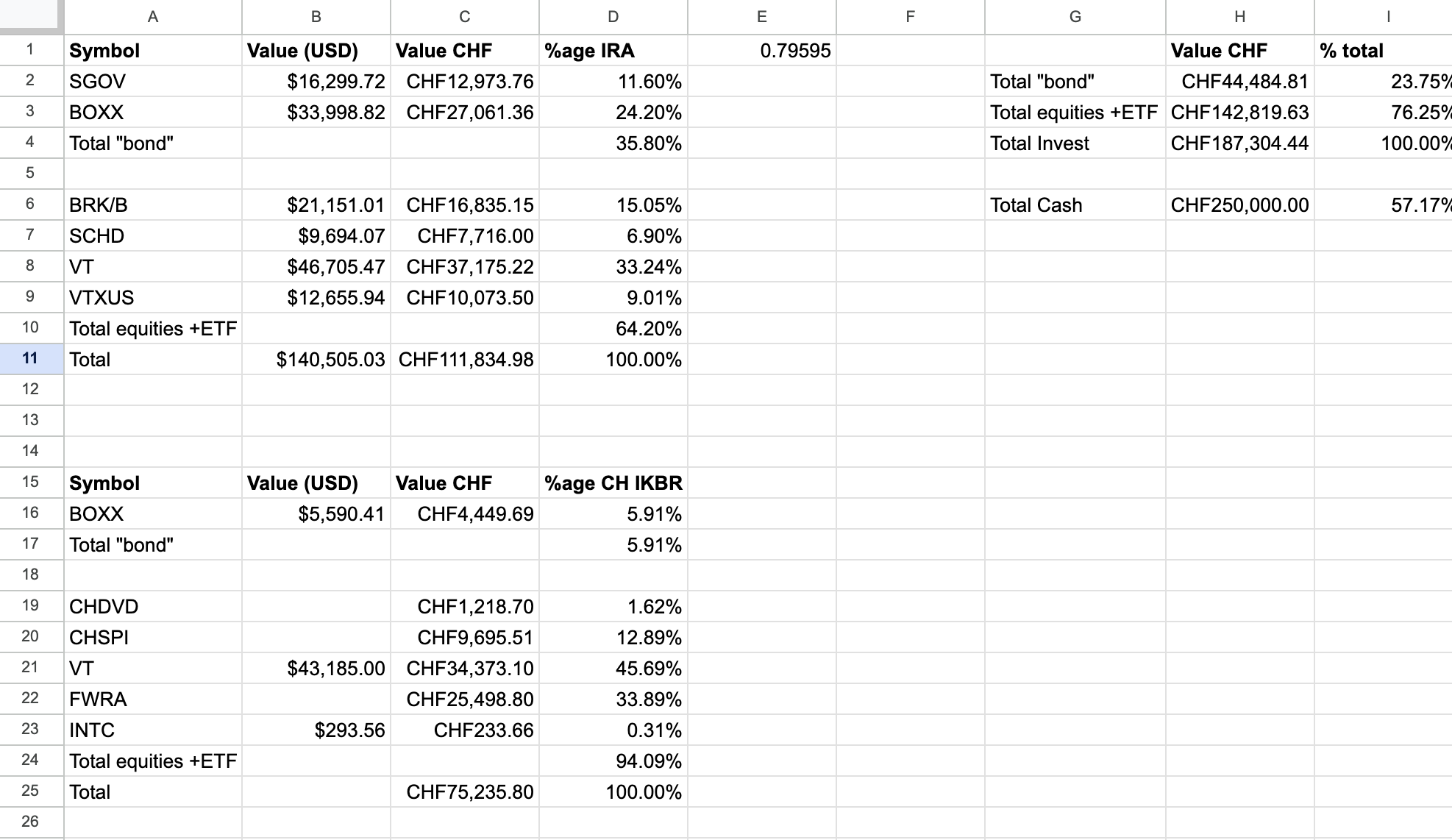

Top left is my US Rollover IRA. There are tax penalties for withdrawing this before age 55 so I have at least 12 years minimum, but I don’t really foresee retirement before 60.

Bottom left is investments I started this year moving some of my savings and then adding monthly, in Interactive Brokers

Top right give global breakdown, and adds current cash in bank doing nothing

My plan was to slowly CDA my savings into more equities but a month after investing Trump started with Liberation day etc. and I got spooked and slowed down. For the US IRA I parked money in BOXX/SGOV, again with an intention to CDA more into equities (which I have done slowly the last months).

I have an unfortunate change in circumstances as recently I found out my wife’s cancer is not treatable. This has further reduced my risk appetite, most importantly because in a few year I will need to re-finance the mortgage on 1 salary so will rely on assets to reduce loan amount. Ergo, what to do with the 250K currently in the bank, and the first step realzing that BOXX/SGOV are not doing anything for me with the USD sliding.

That is why I was re-visiting bonds but this just doesn’t work as a Swiss investor. That is why I was wondering what else exists that has some risk but even lower volatility than VT/FWRA, with a goal of purhaps investing about 100K CHF of my savings and leaving the rest in the bank .

I guess I could also look at paying into Pillar 2 and then withdrawing later to guarantee a tiny return, but there are rules on how soon the withdrawals could be made.

As stated by @Dr.PI, 0% is the current risk free rate in CHF. If the SNB lowers their policy rate some more, 0% checking/savings accounts will be a great deal, providing more returns than banks themselves get on short term cash.

For longer term vehicles, I would look into medium term notes, possibly building a ladder of them if I wanted to preserve some rebalancing possibilities.

Pillar 2 can be used to amortize a mortgage on your primary residency so if that’s the targeted use for it, you should have no problem withdrawing it. There is a 3 years lockup period for buy-ins and you can withdraw only every 5 years so you’d have to plan how you intend to use it ahead of time in order to make it as peace of mind preserving as can be.

You may want to study the insurance part of your second pillar and that of your wife if applicable in order to best understand what they can do for you in your situation and if having more of it, or depleting it, would be a good option (I’d look at the disability and life insurance for both the partner and children (if applicable), as that coverage can also help with hardship).

Sorry for the radio silence after asking for help - I had my own medical issues with a minor operation this last week.

I had already been selling some of the SGoV/BOXX form the IRA in the last few months, but have now accelerated that . From my Interactive Broker account I have closed the BOXX and put it all into VT.

The 2nd pillar buy-in has the advantage of tax savings. If I buy-in 20-50K now, then I’ll save on the marginal tax rates which for this year will be high with the combined salary with my wife. When it comes to re-finance the house in 3 years then the income will be much lower (surviving spouse pension included) and the taxation of pillar 2 withdrawals seems to be reduced. In which case I should act before the end of the year on this.

I have contacted. my wife’s pillar 2 provider and have an estimate of the pension. I’m not worried about hardship, but need to avoid the stress of having to sell the house and potentially move. We live in small village and have a very good support network in place that I need to protect. I don’t imagine interest rates rising sufficiently to impact the mortgage affordability on a personal level, but it would be the compliance with regulations which might force me to have to reduce the loan amount.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.