By what metric?

Here is a white paper:

“How Diversification Impacts the Reliability of Outcomes”

You will still have a much wider distribution of outcomes with less stocks.

By what metric?

Here is a white paper:

“How Diversification Impacts the Reliability of Outcomes”

You will still have a much wider distribution of outcomes with less stocks.

Reduction of idiosyncratic risk

First of all this is not an academic paper and therefore should be enjoyed with some lets says scepsis since it promotes their own products.

If you read the paper you realize that they are talking about the premiums: I quote: “As shown in this paper, diversification can increase the odds of capturing the premiums when they appear.” We arent talking here about factor premiums, are we? If you want to capture factor premiums, you need a factor portfolio. VT is not a factor portfolio.

The Appenix might have interesting data.

I dont understand why they used a sample period from July 1979 to June 2016 if you have data on the us stock market that goes further back ![]()

That is not a metric.

Median outcome, standard deviation, 5th/25th percentile result are metrics.

Portfolios formed with 30 stocks will not beat portfolios formed with 1000 stocks on these metrics.

Yes, this paper relates to factor investing.

But the point about the reliability of outcomes also applies to a market cap weight.

isnt just a number, idiosyncratic risk is part of the standard deviation of stock returns.

they actually do, check out low beta, eventhough it is disputed.

No it doesnt. Factor investing sorts the stocks in advance. Therefore you get with factor investing a selection of a preselection. Market cap weighting doesnt do that.

Lets for example take the value factor: First you sort all 100 stocks in value stocks and non value stocks. Out of the 10 value stocks then you choose the stocks for the ETF. Choosing out of 10 stocks isnt the same as choosing out of 100 stocks.

I do not understand this sentence.

So you mean factor investing?

Yes, the excess return of a factor may make up for the additional idiosyncratic risk that you get by selecting fewer stocks.

But the idiosyncratic risk is still there with 30 companies.

Can you be a bit more precise about what exactly is unclear about that sentence?

Low beta is a factor discussed in factor investing. I looked for an example since you came with factor investing.

This sentence doesnt make sense. Idiosyncratic risk isnt compensated by the market, why would you want to make up for it with factor returns?

No it isnt.

And again we are here not talking about factor investing or is the VT ETF according to you a factor portfolio?

It just doesn’t make any sense.

With a concentrated portfolio you are generally able to get higher exposure to the factors. But this comes at the cost of less diversification and an increase on idiosyncratic risk.

Idiosyncratic risk doesn’t just disappear. It just decreases when you diversify over more companies/sectors and regions.

With 30 companies you still have a relevant portion of idiosyncratic risk. Your returns will be less reliable than a portfolio of 100 or 500 companies.

Just because the difference between 15 to 30 gives a bigger reduction than 30 to 100 doesn’t mean you don’t gain anything from 30 to 100.

As already stated, standard deviation is only one metric to measure idiosyncratic risk. Median, 5 and 25 percentiles outcomes after 10 or 20 years are much better metrics to capture idiosyncratic risk.

What I tried to say was that you shouldnt see standard deviation of returns just as metric, but consider the components explaining it.

Obviously it doesnt just disappear ![]() we call it diversification. And concerning the regions how to do you handle large multinational companies as for example Nestle?

we call it diversification. And concerning the regions how to do you handle large multinational companies as for example Nestle?

That is your claim, not a fact. There is no consensus on this topic.

You might gain something the question is at what costs. An optimization gives a clear result. You are talking about 30 to 100 lets say for sake of it you hold 100 stock, how big do you thing the diversifaction benefit will be after 100 or 1000 stocks ![]() see where I am going?

see where I am going?

Agree that standard deviation is only one, but it is the most used one ![]()

Diversifiing is free, so it won’t cost anything.

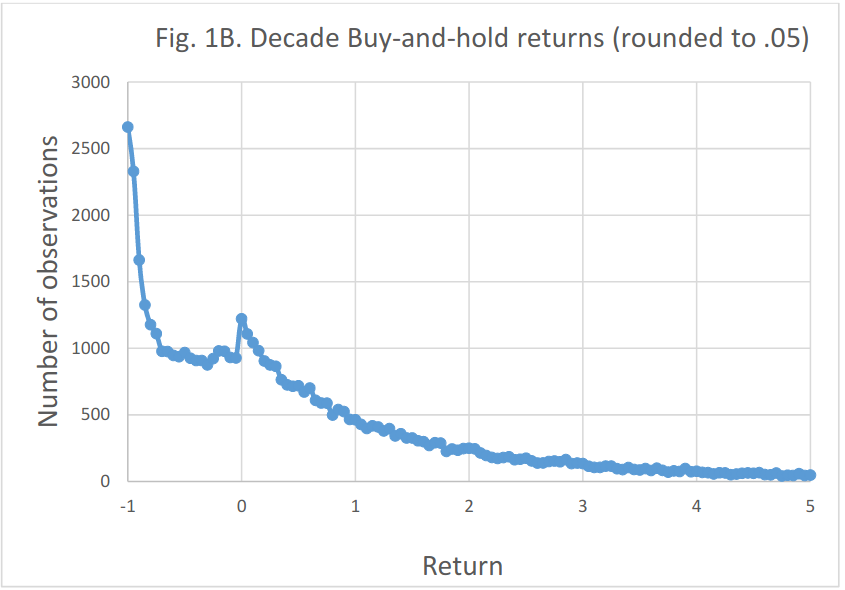

It is a consequence of the skewness of stock returns.

It is a pretty bad risk metric overall. I wouldn’t base decisions on it.

Nothing is free ![]() I agree that it is cheap with ETFs, but another question would be if it is even necessary or not.

I agree that it is cheap with ETFs, but another question would be if it is even necessary or not.

You might have to elaborate on that since afaik a normal distribution is a pretty good approximation for stock returns in developed markets.

Would not agree. For risk management a bad metric but not in general a bad metric.

I havent yet read the whole paper but to keep it short (conclusion):

It would be helpful if you can point exactly to the passage where is written that you need more than 30 or lets say 100 stocks to get a well enough diversified portfolio.