Hi, I’ve been asked to suggest which funds to buy from PF and Raiffeisen, for a supersimple investment with low-medium risk for 6-10 years.

I know PF has Funds 3,4 and Global that seems to fit the description, but with a high TER and now with new PF fees.

On the other side, Raiffeisen has now some new ETFs but I know nothing about them (and how much they cost ).

I think ~ 50k, but they didn’t tell me exactly. I suppose 1-2 funds are ok.

I said PF and RF because I know they have those accounts and they did talk with people there in person.

Having seen a bit of the prices, I wonder if yuh can be added. It’s basically PF and very easy to use. Pity that they don’t have a website, but that’s only me.

Postfinance is easy to understand:

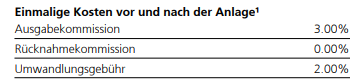

0.15% custody fees (Raiffeisen: 0.25% )

1% to buy (Raiffeisen: 3% on that example. it might vary)

PF fonds 1 (Bonds): TER 0.79 [side note: 1 star rating, probably a bad idea as a fund alone?]

PF Global A : TER 0.8%

etc.etc. The site is very easy to read.

I think I can see the strategy of Raiffeisen: They want you to meet them at any cost. Their website is full of links to organize a meeting with them. Postfinance instead is less interested in that.

This exercise has badly defined boundary conditions, so I suggest to keep away from it. Like it was discussed in the thread about investing for parents, if there are market losses, it is your fault, if the strategy is too conservative and there are not enough gains, it is also your fault.

Yes good point. But I could at least suggest which platform to use between the two.

At the moment it seems that PF is cheaper. Purchasing costs for 6-8 year make a difference. The only positive for raiffeisen is their TER, but it depends on which funds so it’s hard to compare.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.