I have removed vermoegenszentrum’s savings account comparison. It is less functional than the one from moneyland and clearly biased ![]()

2 Likes

Hi!

Migros bank has some good interest rate both for fixed term deposit and saving accounts. So, still one of the best solution for keeping the money liquid.

But now, the question: what is the risk (above 100k)? If we look at the rating, the bank « only » rates A while other similar bank tends to rate slightly higher. Is Migros bank a bit risky and special care is needed?

Rating as found here: Swiss Bank Ratings from S&P, Moody's and Fitch - moneyland.ch

Thanks!

1 Like

Most banks in Switzerland are not at any real risk, as long as the real estate market doesn’t collapse - and what none of us should forget, the 100k is what ist protected, if sufficient funds are in the insurance (ESI Suisse), as far as i know… so, if a larger bank would come to fail, this 100k would not get very far for a lot of clients :-)… The system is different than the one in other countries, at alest as far as i know ![]()

Important thing regarding liquidity: bear in mind that saving accounts have pretty restrictive rule regarding at what rate you can get your money out of it… ![]()

3 Likes

I don’t think there’s a high probability of a client loosing money in a bank failure in Switzerland. That being said, if I were willing to take on risk that can be mitigated, I would not keep my money in cash. Cash is for money I need available and can’t afford to loose, I wouldn’t give up on the esisuisse insurance for a few tenth of a percentage point of interest.

Savings accounts also usually have withdrawal limits, which is another reason to prefer using several accounts for bigger sums.

1 Like

Just stumbled upon this new offering from Leonteq: https://structuredproducts-ch.leonteq.com/news/all/overnight-return-index

It is an ETP on the SARON rate with 0.3% fee, so a ~1.4% rate currently. Could be an interesting alternative to short-term fixed deposits or savings accounts (with more flexibility, as there are no minimum holding durations). Trading on SIX starts on 15/09/2023.

I am not sure about the risk yet. The term sheet mentions that they do a collateral pledge according to a security agreement that you can order via phone, fax, or e-mail (why not just publish it online?).

2 Likes

Oh nice, that could be very interesting with a 0.1% fee. I have not requested any details because 0.3% was too high to for me, but just wrote them an e-mail regarding the TCM agreement.

The ETP is tradeable on IBKR and spreads are reasonable. They seem to be always 0.02 (so ~4.5 days of yield) based on the SIX historical data, I guess you are almost always trading with Leonteq which is the market-maker.

It is a pity that you have to pay the stamp tax when buying / selling. With the current rates, this is a month of yield for a buy or a sale. So the product is not really suitable for short-term deposits.

2 Likes

Are you sure? Shouldn’t be the case with a foreign broker like IB.

But unfortunately there’s a big question of security: what is going to happen if Leonteq is bankrupt?

Oh yes you are right, was reading the term sheet where they mentioned that stamp tax always applies, but the normal rules should apply for investments via foreign brokers.

If I understand the Triparty Collateral Management correctly, nothing should happen because the ETP is fully collaterized. But this of course depends on the quality / volatility of the collateral.

Received the TCM agreement today. I have not studied it in detail (45 pages of legal clauses), but in general, SIX ensures that there is always enough collateral and you are eligible to the proceeds of the collateral sale if Leonteq defaults. The most important points in my opinion are:

- There is no overcollaterization requirement.

- Leonteq has five business days to fix any undercollaterization.

- When the collateral is liquidated, the agent is paid first and the holder of the product only afterwards.

- Investment-grade bonds, equities of a standard index, and ETFs are accepted as collateral.

So overall it is more or less a margin loan to Leonteq (without overcollaterization). As long as there are no huge market swings, this should work pretty well, even if Leonteq defaults. But I am wondering how it would work in a black swan event where Leonteq defaults and a lot of assets drop in value.

Moreover, almost all of the liquidity comes from Leonteq. If they suddenly decide to no longer be a market maker for the product, you would probably have a problem, because who would then buy this? You cannot just redeem the collateral in such a scenario.

So for me personally, it is too risky for the cash part of my portfolio (which should have a risk as close as possible to 0 for me), but YMMV.

I read the wealth of information you posted to take exposure to CHF. I want to invest with a multi year horizon 100k CHF in a fixed income product with short duration. I noted you started your journey a year ago. Can you recommend some ISIN I can use via Interactive Brokers (probably LU-ISIN) that come as your best pick in terms of return/fee ratio ? Thanks in advance

Here is an important piece of information, which was never discussed AFAIK.

EDIT: applies to Canton Vaud only.

According to the taxation practice in Switzerland, the “interest earned on capital” is added to the taxable income and then deducted from the taxable income up to certain, rather high, limits.

See for example

That means that this type of interest is essentially tax-free. This taxation practice concerns interest on bank accounts, short-term deposits, obligations/bonds (!!!) exchange-traded or not, mid-term notes of banks and similar instruments.

The income from stocks and investment funds is not subjected to this treatment.

For me it means that the interest from money market funds does not receive this preferential tax

treatment.

Another point is that an interest earned on individual bonds is subjected to this preferential tax treatment, while an interest distributed by a bond fund is not!

You can imaging yourself implications on “fixed income options” for private investors in Switzerland…

1 Like

Aren’t those the health insurance premium limits? Which at least for me is already lower than my basic health insurance premium (cheapest/highest deductible)

I wouldn’t call then very high ![]()

OK, probably we had ran again into differences between cantons, but for me those limits are applied on interest only, separately from the health insurance deduction (maxed out). So it looks like I can earn tax-free interest up to like 200k CHF at least.

which canton? (please be ZH ![]() )

)

also does this apply to bond etfs? or only single bonds?

In ZH it’s definitely the same limit.

Edit: looks like it’s separate only in a few french speaking cantons. (Note Bund is always combined)

It’s not clear to me.

How exactly this works?

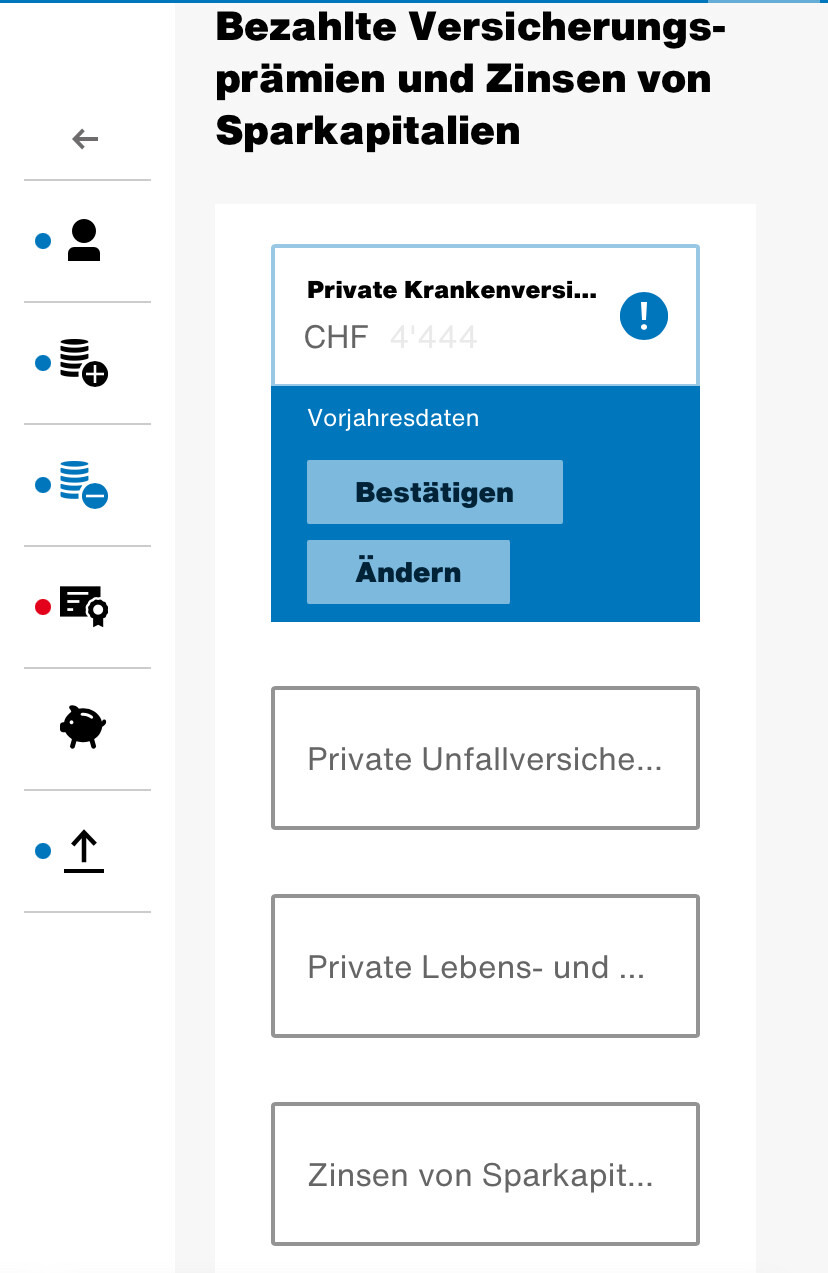

Let’s assume I only have saving accounts and interest is 500 CHF. This number is reported under interest income in Bank account section.

And then there is no tax on it? I didn’t see any tax free interest income on my tax return. But maybe it’s part of the overall calculation and I didn’t realise.

There’s a section interests from savings in the deduction part of the form.

Oh I see.

I understand now

This number is part of same section as Health insurance premiums and others in canton ZH.

As long as other costs of insurance exceed the limit; then this deduction won’t apply.

1 Like

Yes (Zinsen auf Sparkapitalien). But as mentioned most people are already maxing out the deduction with just the base insurance, so not worth bothering entering anything.

3 Likes

Yes, I see how these two deductions are combined in the Confederation part, that deduction is maxed out, of course.

OK, in this case I guess everyone should check what applies to them…

If I interpret the same document correctly, the deduction for interest is separated from the health insurance deduction in FR and VD. @thepoorswiss ?