Aren’t those the health insurance premium limits? Which at least for me is already lower than my basic health insurance premium (cheapest/highest deductible)

I wouldn’t call then very high ![]()

Aren’t those the health insurance premium limits? Which at least for me is already lower than my basic health insurance premium (cheapest/highest deductible)

I wouldn’t call then very high ![]()

OK, probably we had ran again into differences between cantons, but for me those limits are applied on interest only, separately from the health insurance deduction (maxed out). So it looks like I can earn tax-free interest up to like 200k CHF at least.

which canton? (please be ZH ![]() )

)

also does this apply to bond etfs? or only single bonds?

In ZH it’s definitely the same limit.

Edit: looks like it’s separate only in a few french speaking cantons. (Note Bund is always combined)

It’s not clear to me.

How exactly this works?

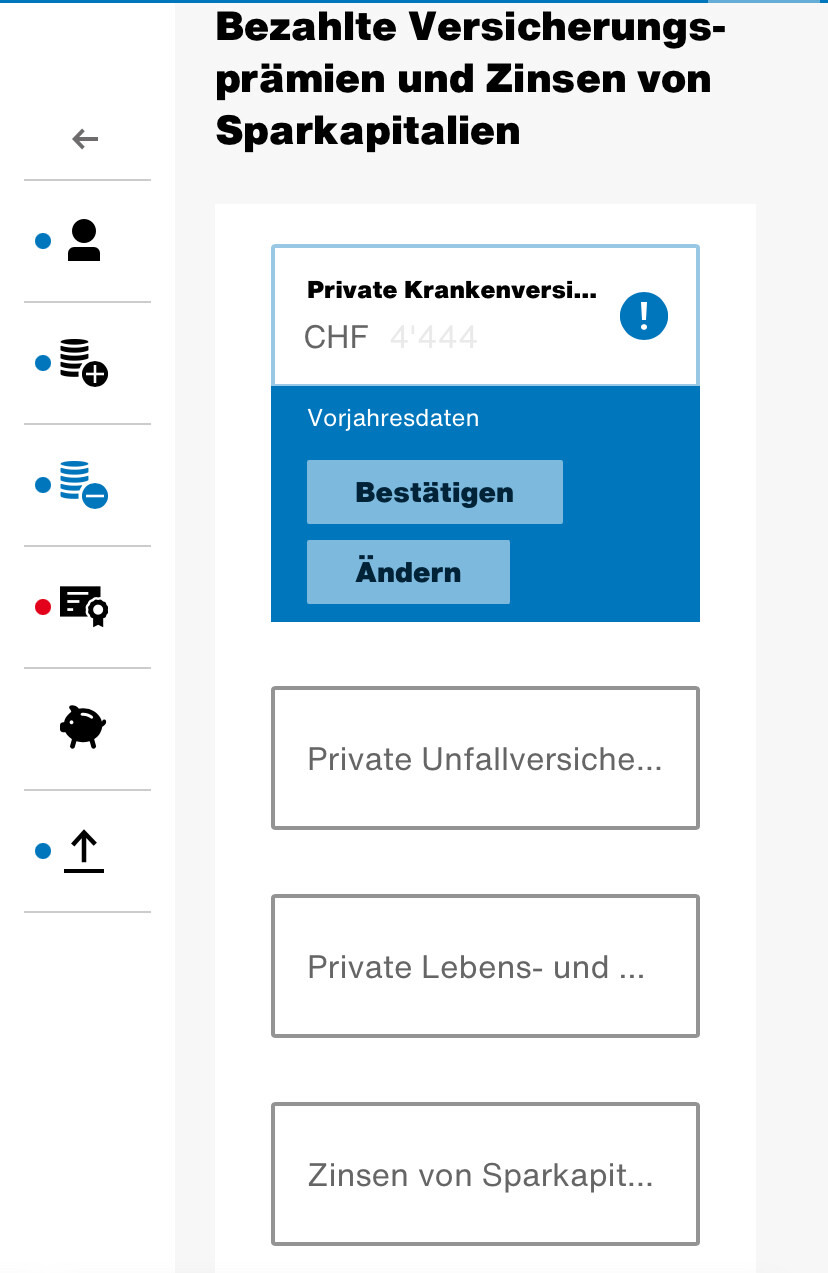

Let’s assume I only have saving accounts and interest is 500 CHF. This number is reported under interest income in Bank account section.

And then there is no tax on it? I didn’t see any tax free interest income on my tax return. But maybe it’s part of the overall calculation and I didn’t realise.

There’s a section interests from savings in the deduction part of the form.

Oh I see.

I understand now

This number is part of same section as Health insurance premiums and others in canton ZH.

As long as other costs of insurance exceed the limit; then this deduction won’t apply.

Yes (Zinsen auf Sparkapitalien). But as mentioned most people are already maxing out the deduction with just the base insurance, so not worth bothering entering anything.

Yes, I see how these two deductions are combined in the Confederation part, that deduction is maxed out, of course.

OK, in this case I guess everyone should check what applies to them…

If I interpret the same document correctly, the deduction for interest is separated from the health insurance deduction in FR and VD. @anon95353169 ?

In Fribourg, there is indeed a small deduction for that. It’s 150 CHF for a single person and 300 CHF for a married couple. In the tax software, the interest (dividends and interest for instance) is automatically deducted up to this limit.

UBS offers 1.6% interest on a 1 year Fixed Term Deposit for new money.

BUT that requires using them as broker for an equal or larger amount and buy UBS products. e.g a UBS MSCI World ETF - WRDUSY.

For example you can have 100K+ in WRDUSY and 100K with 1.6% fixed for one year.

More here.

Issuing commission and custody fees, though can be negotiated and dropped >50%, are still high compared to IB or a low cost Swiss Broker.

Interesting for UBS employees that are forced to use them as a broker and others that are willing to pay more for “peace of mind” by using a big swiss bank as a broker. (Let’s not start a debate about IB VS UBS please ![]() )

)

Do you happen to have list of 300 funds that are possible to be bought under UBS investment account?

I read that admin fees is between 0.20% to 0.35% depending on which fund. 0.20% includes a small list

So I guess people can try to calculate if 1.6% on cash amount is worth the extra admin fees. Of course one needs to account for other fees (1% transaction fees, safekeeping fees etc)

Btw- WRDUSY is an ETF and not a fund. Is it also part of this scheme?

I think all of them. But I am not sure. I was interested in ETFs only.

Depending on the fund, issuing commission is ~0.8-1% but it can significantly dropped e.g. to 0.3%. Custody fees unfortunately are a % of the investment amount with no upper limit. They start from 0.35% and they are harder to drop.

Correct + as I mentioned, some do not mind the extra admin fees for “peace of mind” or for broker diversification or for UBS employees.

Well ETF is also a fund ![]()

The Duo Savings offer includes all UBS ETFs for sure.

The issue I see is that interest rates are only fixed for 12 months.

So if they fall after 12 month, the admin fee on the funds will become less interesting & then if you sell the funds with 1% transaction fee, you also lose the advantage of higher interest rate

Let’s say -: 25K invested in 1.6% Fixed depot, 25K invested in 0.35% Admin fee fund , transaction fee = 1%

Total fees = 87.5 CHF (custody) + 250 CHF (buy) = 337,5 CHF

Total interest = 400 CHF

Net interest = 62.5 CHF

Selling fee (1%) =250 CHF

Effective interest after 1 yr =(-) 187. CHF

Compared to

25K invested in 0.15% savings account and 25K invested in same fund (UBS fund) held at Swissquote

Buying fees = 9 CHF (prime partners)

Total fees = 80 CHF (custody) + 9 CHF

Total interest = 37.5 CHF

Net interest = (-)51.5 CHF

Sell fees = 9 CHF

Effective interest (after 1 yr) = (-)60.5 CHF

Correct. This is not for all…

Keep also in mind that the issue/sell commission could be far less than 1%

The trend for savings account rates is downward + for larger amounts already 0 in most banks

I was wondering why UBS is offering it because there is no way they can afford such interest… and I think its just a marketing technique.

1.6% interest on Fixed deposit is recovered via Trading fees (1%) & admin fees (0.35%) & safe keeping fees (if any), Fund TER %

This makes sense but a great marketing nevertheless.

It looks intentionally convoluted. I wouldn’t even looked at it. Without doing any calculations, from UBS I expect only offers that profit UBS, not the customers.

Of course it is a marketing thing! They want to to attract new customers. What did you guys expect? ![]()

I do not see it being convoluted though. For every X amount you invest in UBS ETFs (++) you can put max X in a one year Fixed Term Deposit account with 1.6%.

Issuing/Selling/Custody fees are well known to be non-competitive when it compares to IB and the like. Even if you negotiate and bring them down a lot.

There are cases though that could be beneficial for customers. (will not repeat)

Would be nice to have KIID for this total scheme where they show the costs and impact of fees

That would make everything clear

That’s a good start:

https://www.moneyland.ch/en/ubs/online-trading/online-trading-e-banking

The good thing is that you can negotiate far lower fees + it is easy to book a 30 minutes call and get the numbers.

PS I don’t work at UBS nor I hold shares (at least not more than my world index ETF provides) ![]()