Yup, but I need at least two years to add you to the chart (I can update it). I have 50.1k for end of 2020, but do you know the NW at the end of 2019? If yes, I add you. And congrats for the 50k!

True. But it’s hard to standardize the process for everyone. Except if everyone follows MP’s way of doing!

is that capital gains & dividend (before/after taxes)? It‘d be interesting in general to see what came out of capital gain / interest and what from adding capital.

Annual expenses is maybe too subjective but the number of dependents might be an interesting parameter. I fear there would be too many to take into account, though…

True @Zerte2 . If everyone is willing to give this piece of information, I’ll take care of the visualization!

Another metric that I find quite interesting is the one explained in the Millionaire Next Door book where the expected net worth being : age * income / 10. This number represent an “average accumulator of wealth” (AAW). If the net worth is half of that, you’re an “under accumulator of wealth” (UAW) and if it’s twice that, you’re a “prodigious accumulator of wealth” (PAW).

In my current case, I’m reaching the AAW this year, if everything goes well.

In summary this metric compares the net worth with the age and the income, and in your case it compares with the expenses.

Income can vary a lot along one’s career. Do you take current income or is this aspect somehow already considered in the formula ?

Another topic: what would you do with mortgage? Theoretically it has to be deducted from NW but in my case I already know we’ll get rid of the house when we retire…

You’re right, the income varies. It may be good to smooth the income over some years to be more accurate. I don’t know.

Regarding the mortgage, yes, you deduce it from your NW. Or you just count the part of the house you really own (house value minus remaining mortgage).

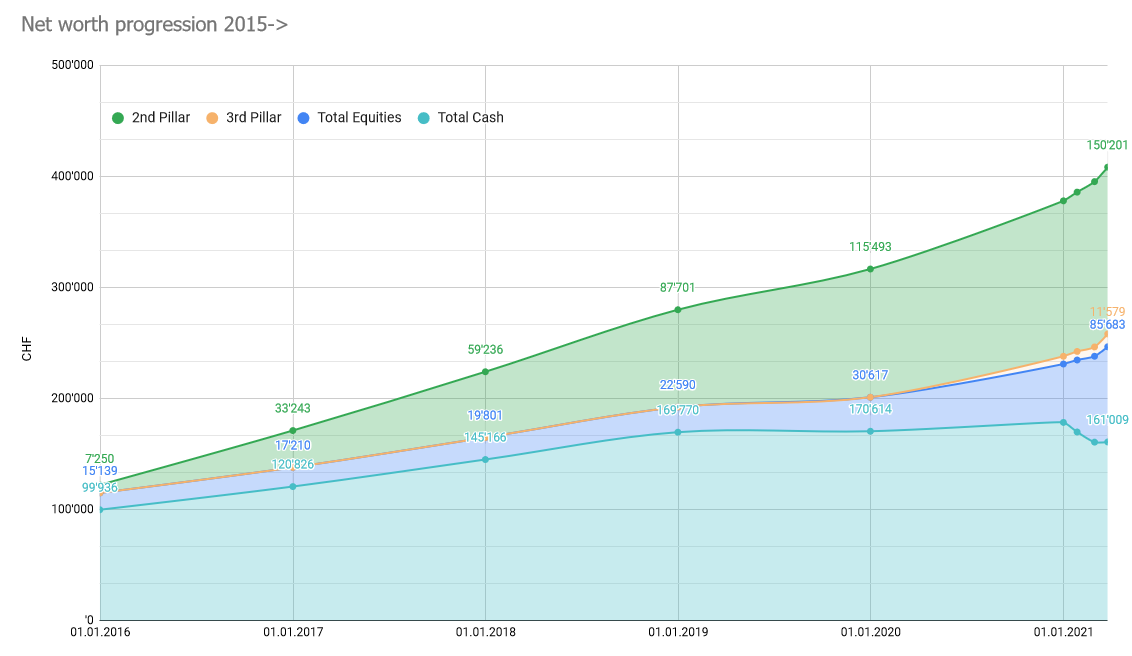

Quarterly update. I finally crossed the 400k mark. The chart is stacked somewhat differently than before, it’s all for readability. I started monthly tracking but am only showing the annual values and the value for latest month. I also removed the total NW line for readability. It’s about 410k now.

As discussed before, some context is always useful:

41 years old

5+ years in Switzerland (tracking starts there)

married, family of 4

single income

I am in the process of adding a small crypto position but it doesn’t register on the chart yet. More importantly, I have started to reduce my cash position and it really shows. Other things worth mentioning: Jan-Mar 2021 got a boost from my Gamestop trades and the annual bonus payout. I expect the rate of growth to even out for the rest of the year.

Edit: about currencies

The cash amount I report here is a composite of EUR and CHF from various accounts which I track in more detail using YNAB. I use the forex rate on the monthly reporting date to convert everything to CHF. Any USD is reported in the Equities category, even if it’s cash on my IB account. I always have some available cash for my option trades and sudden market movements.

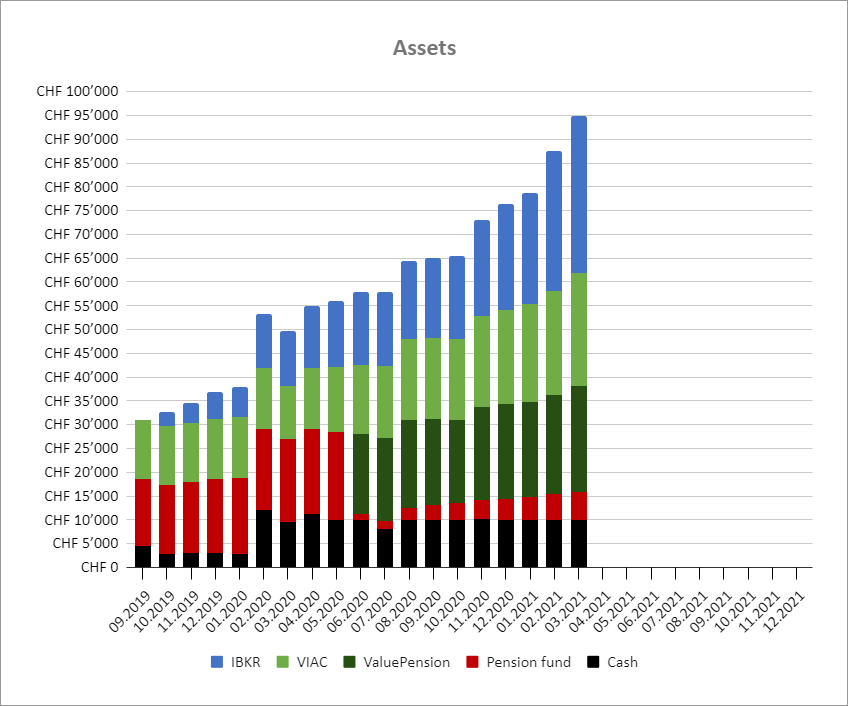

Thanks, I think it’s the right level of granularity for me. Tracking monthly was always my intention but it was not practical for the historical data. I like seeing the impact of my decisions on this level. I’m using Google Sheets.

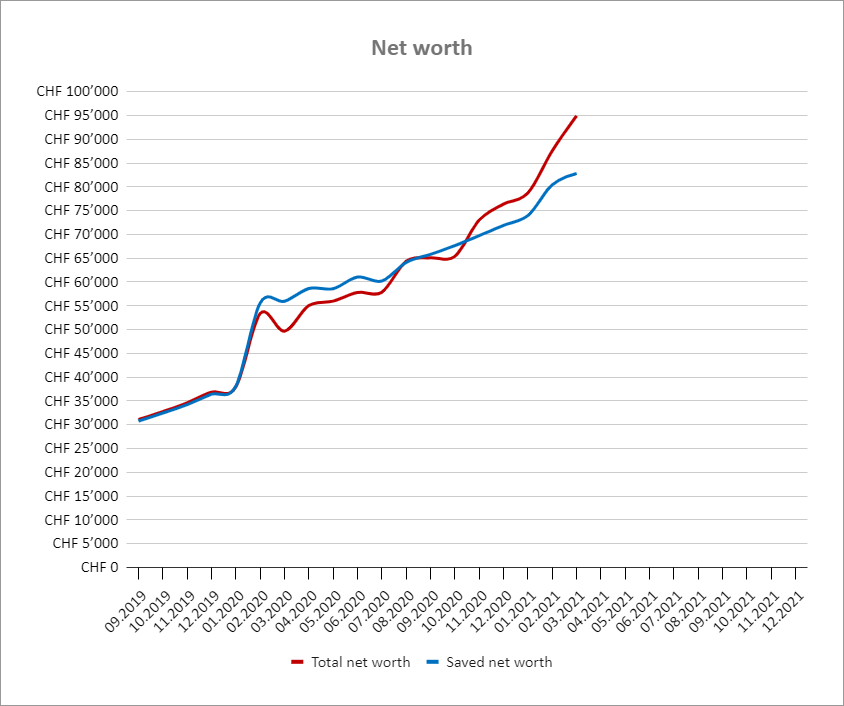

Market has been crazy in the last couple of months. 5 months ago I was at 65k networth and now at 95k networth. +15k from savings and +15k from market returns. I’m approaching the 100k mark way faster than expected.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.