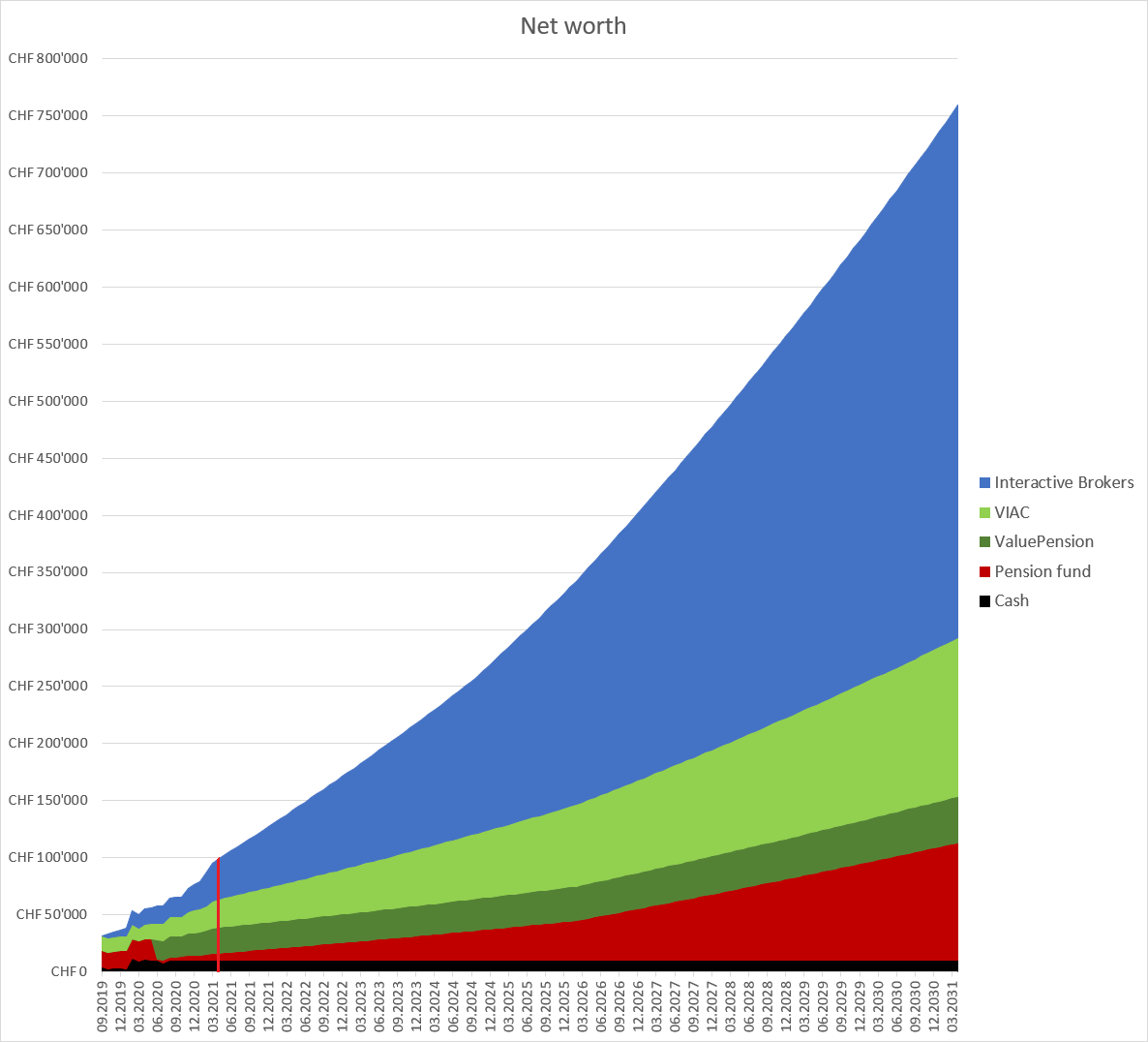

I made a projection and made rather pessimistic assumptions for the future. 6% return, no increase in current savingsrate (apart from the increase by 800.-/month as soon as I finish my studying in 2024), only 1%/year salary increase. You see the actual numbers till the red line and afterwards the projection till 2031 (when I’m ~40 years old).

It’s very motivating! Especially when thinking about the fact that my salary will increase way faster than that and that my savingsrate won’t stay the same the next 10 years. So in reality I might get close to 1 million by then.

Pessimistic and 6% return expectation in same sentence? Though increase in your salary and savings amount and/or savings rate will likely pick the slack if the returns over next decade are lower (than 6%).

True. But if the model is supposed to be conservative 6% seems a bit high, right?

On the other hand a 1% yearly salary increase seems somewhat too pessimistic…

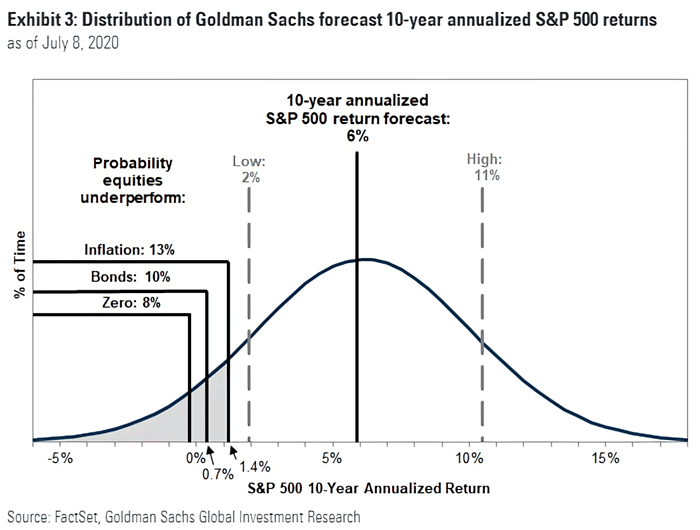

Yeah I guess. So what would be a conservative CAGR for 10 years? If you look at ARK, they treat bear case as expected value -1 standard deviation (and bull case +1).

Don’t forget most international returns and all US returns will be in USD. The USD depreciated 0.7% p.a. to the CHF last hundred years. And in the last 20 years that depreciation has even accelerated (>2%p.a.), with no end in sight.

And I saw @Cortana 's unit on the y axis is CHF.

So I’d subtract 1% from an “average return of 6%” if measuring the returns in CHF.

And what is the probability that the next decade brings further advancements in computing power and artificial intelligence, causing a feedback loop in the rate of technological improvement, the so-called singularity?

It makes sense to be a bit pessimistic about return assumptions of financial assets.

Being wrong about a pessimistic expectation doesn’t negatively affect your plan. Being wrong about an optimistic expectation has negative implications.

That‘s why it‘s called assumptions and not facts. To RE or be FI you just have to wait until you hit your FU number. If it takes a year or two longer so be it. Main influx is still cash and returns make a small portition out of the eventual net worth (especially if you do it in a short space of time)

4% instead of 6% returns wouldn’t change that much regarding my FIRE goal. I might end up working till 54 instead of 52 if that happens. Time is still the biggest factor in all this.

You will have possibly saved 1’000’000 CHF by the age of 40. By 52 this could be over 3 million. What is your FIRE goal?

These are my reference points:

Poor FIRE: 1’000’000 CHF with 3.6% SWR (3’000 CHF expenses per month)

Safe FIRE: 2’000’000 CHF with 3.0% SWR (5’000 CHF expenses per month)

Fat FIRE: 4’000’000 CHF with 3.0% SWR (10’000 CHF expenses per month)

I practically achieved the first milestone, but I don’t really feel “independent” yet. So I’m pushing towards Safe FIRE. I currently don’t aspire to ever reach Fat FIRE.

If you’re expectation is (too) pessimistic, you might take an inefficiently low amount of risks into your plans.

For example, you might put a higher amount of your assets into bonds, if you expect the stock market to outperform bonds to a lesser degree.

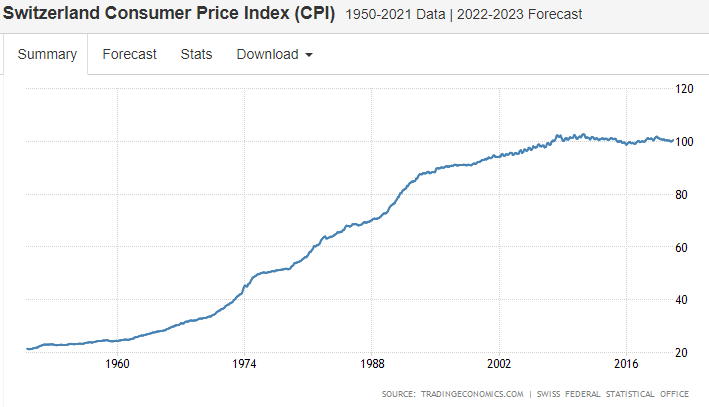

You should, but if you don’t invest in fixed income assets, your investment should grow on top of inflation. Additionally, we have seen that in the last 30 years inflation in Switzerland practically stopped:

But you’re doing it you just said we have to factor in inflation. Why not deflation? Any crystal balls you have lying around? Or it is reasonable to assume inflation (based on what if not history)?

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

you just said we have to factor in inflation. Why not deflation? Any crystal balls you have lying around? Or it is reasonable to assume inflation (based on what if not history)?

you just said we have to factor in inflation. Why not deflation? Any crystal balls you have lying around? Or it is reasonable to assume inflation (based on what if not history)?