I am starting to think about my personal FIRE strategy and I am considering to set up a company to separate buy&hold investments from some more active investment strategies which could otherwise count as “professional” investment.

The advantages I see are:

No risk of being classified as a professional investor and therefore no tax on the capital gains for the private buy&hold investments

Freedom to use any investment/trading strategy with the assets of the company

Some tax optimization by deciding how much salary I get from the company (can be adjusted quickly)

Possibility to deduct some expenses as the operating cost of the company

Remaining in the 1. pillar (AHV) or maybe even 2. pillar (if the salary is above the threshold) until the retirement age

Disadvantages would be obviously the cost of setting up and running the company.

I tried to compare it with the case when I simple FIRE and stop working with a 1’000’000 CHF in investments. My very conservative assumption would be that I receive 1.5% of dividends on my investment portfolio and additionally achieve 6% capital gains with my buy&hold strategy.

On the other hand when setting up a company I would put 50% of my investments into the company and achieve 1% dividends and 9% capital gains with that part. Again this is a very conservative assumption but I’d like to be on the safe side. The company would pay me a salary of let’s say 20000 CHF per year but this is adjustable.

With those assumptions (and with some help of AI ) I get:

Position

Case 1: Private (100%)

Case 2: Hybrid (50/50 Split)

Asset Allocation

CHF 1,000,000 Private

CHF 500k Private / CHF 500k GmbH

I. Gross Income

Dividends (Private 1.5% / GmbH 1%)

+ CHF 15,000

+ CHF 7,500 (Priv) / + CHF 5,000 (GmbH)

Capital Gains (Private 6% / GmbH 9%)

+ CHF 60,000

+ CHF 30,000 (Priv) / + CHF 45,000 (GmbH)

Total Gross Income

+ CHF 75,000

+ CHF 87,500

II. Operating Costs & Taxes

Salary (Gross)

CHF 0

CHF 20,000

AHV Contributions

- CHF 2,600 (Non-empl.)

- CHF 2,120 (ER+EE on salary)

Private Income Tax (St. Gallen)

- CHF 260 (on 15k)

- CHF 1,750 (on 27.5k)

Corporate Profit Tax (GmbH)

CHF 0

- CHF 3,458 (after salary/costs)

Fiduciary & Trading Tools

CHF 0

- CHF 4,000 (Net expenses)

Total Expenses

- CHF 2,860

- CHF 11,328

III. Final Net Growth

+ CHF 72,140

+ CHF 76,172

The wealth tax is not considered since it will be almost the same in both cases.

What do you think, are the calculations realistic? Am I missing something? Of course the most important point would be that I achieve higher returns on the capital in the company, this is my assumption. But with my 10+ years of experience in the stock market and a lot of time after FIRE I am very confident that it will work, I would actually expect much better results than just the current 10% per year total return assumption.

The strategy is not conservative, there will be for sure risks which I am well aware of. Conservative is my assumption that with this strategy I will be able to achieve 9% or 10% per year, I would actually expect more.

Ok cool, then I’ll buy into this risky strategy that “conservatively spoken” you expect 9+% per year.

What is the special sauce that you can get like 50% more return than average market?

Kidding of course; you hear it from my comment, I would not count with such a high number and this affects the balance from “being worth of doing a company” or not.

That’s a valid point of course but I have to assume something and those numbers are currently my best guess without being too optimistic and being well aware of the risks.

My point is not to discuss my trading strategy and if 9% or 10% or some other percentage would be realistic with it. My point is to discuss if the comparison table is roughly correct under those assumptions or if something significant is missing.

Maybe someone has already experiences with such a setup and knows about some additional expenses which I haven’t considered so far.

Many people overestimate being counted as professional investor. But I assume you have done an analysis and concluded a medium to high risk that your trading style will be considered professional.

yes, theres no issue to set up a company as you described, the salary you pay yourself has to be a reasonable one not just ridiculously low. However your case 2 returns doesnt read like it would be considered active trading/investing anyway

After RE I would basically have no taxable income except of the dividends. I would therefore always violate the criteria that capital gains do not exceed 50% of net income. This, together with holding (some) assets for less than 6 months and occasional usage of derivates would give at least a medium risk of being considered as professional investor. And in a good year with outstanding returns (let’s say 30% or more) the risk would be even higher.

And even if I wouldn’t be counted as professional I would still feel uncomfortable that one day the tax office could simply change their mind and there is absolutely nothing I could do against it. So paying a small premium for running a company but having peace of mind in return sounds like it is still worth it for me.

While it may create certain tax implications, your portfolio split and trading strategy are (very likely, especially at a meagre CHF 500k) not tied to or dependent on your legal structuring (whether your operate a GmbH or not).

If you have a superior trading strategy, that’ll net 9%, you can also pursue that as part of your private wealth. Which is why it should be part of the comparison.

Also: Is incorporation the only way you can segregate your “professional trading activity” through - or could you do it otherwise (as in: keeping two separate securities accounts)?

I dont think merely investing your own money will make you a GmBH. Most likely you will need more clients to call it a business. otherwise its just investing your money whatever the route. Better check this with a lawyer because this sounds like a scheme to maximize AHV payments

I think this kind of scheme is especially worth it if you engage in some higher risk activities (financial or contractual). The limited liability nature of a GmbH or a AG protects you as an individual.

Also something else regarding wealth tax. Shares of an entity are sometimes valued at less than the actual net assets of the entity. I don’t know what are the rules but in my case they keep valuing it at the initial share capital.

Do you have a source? If this were a hard criteria (and not cumulative with other criteria) many FIREs would probably be considered professional investors.

I don’t think that violating only this one would be a problem. But together with not holding some assets for at least 6 months and usage of derivates it might be enough to be considered a professional investor.

Or do you know FIREs with no additional income (that’s important!) who regularly violate those 3 criteria and don’t count as a professional?

The rules are for excluding the possibility to be considered a professional trader. But I don’t think the taxman starts even looking before you make regularly 7 digits per year in non-taxable and realized capital gains.

The main reason could be the risk for the taxman, because as a professional trader you can deduct realized losses and don’t pay tax for unrealized gains.

What rich professionals do: realize losses and realize gains only until they offset the losses including dividends. Than they live off debt, as all the rich do… taxman loses, he may even lose the tax on dividends.

Now I wouldn’t start a company for that. Holding a trading company may qualify you as professional trader anyhow and you have some kind of double taxation for half of your money. In addition there are money laundering rules that can hurt your company. And it is a lot of administrative work for nothing.

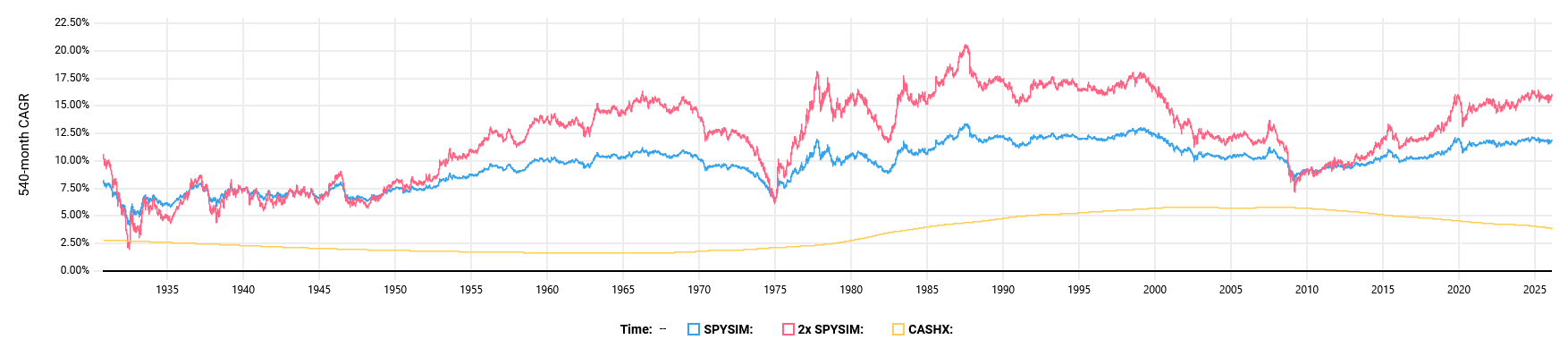

Although there is a multitude of ways to cut yourself when trying to add special sauce to get 50% more real returns than the stock market, those 3%-points additional expected return are very much possible. With a dumb leverage strategy and enough time you nearly get there.

45 year rolling CAGR was chosen to keep the great depression visible

It can take decades to only pull even with the market return. Probably a whole lifetime is required to take “advantage” of that return profile reliably. This is different from stocks vs. cash, where it takes maybe 20 years to outperform in all cases.

Numbers-go-up is a fun game, but not a reliable investment strategy to use those numbers for something.

A bit more diversification will improve that in return and drawdowns, though. I’m certain the market can be beaten reliably with moderate knowledge and a very long horizon. Very high knowledge, an edge even, can probably do better still.

But returns are diminishing for the time invested. Using such on your 100k portfolio would probably be better spent selling that knowledge, working more, and spending less.

The point of those criteria is safe haven. Only if you check all of them, they say they won’t try to tax your trading as a business.

If a regulation is not clearly against laws (or the constitution), it binds the administration as far as the judge is concerned.

But if you break any of those safe haven criteria, then there is not much binding language in that circular. So it will be a judge “in consideration of all circumstances of the individual case” handing down a judgement. If the administration wants to try, (and you take them to court,) that is.

Looking specifically at point 3 of the safe haven criteria of “Kreisschreiben Nr. 36”:

Original:

Deepl translation:

The second sentence is a safe haven upon the first sentence. So if you have any income that is provably enough for living expenses, the second sentence has no importance. Distributions could be that income, fully or in part.

I think @cubanpete_the_swiss employs a rather active strategy including meaningful leverage and many small allocations, deliberately engineered to still check all the safe haven criteria. The capital employed is around 2 million (USD?) as per this post. If I remember correctly they are retired. If they get some pension money that could be enough in and on its own to check criteria number 3.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.