Hello everyone,

I never realized that I pay that much taxes for a second/holiday house in another country, that I rarely use (couple of time per year).

I wondering if it’s normal to pay the taxes in the country where the house is (because it’s not a primary house), plus it adds a good amount also to the taxable income in Switzerland.

To me it sounds like a double taxation.

In addition I read that if the utilization is really low or you don’t use some rooms, it’s possible to ask for a reduction.

Any experience on this topic?

Thanks

It’s normal to pay taxes in the country where the house is located. Foreign real estate must be declared in Switzerland and affects the tax rate for both income and wealth (satzbestimmend), however, it doesn’t affect taxable income or wealth in Switzerland (steuerbar). With this approach, there is no double taxation.

If it does affect your taxable income, have you checked that there is no mistake in your declaration? Have you looked closely at the ‘Steuerausscheidung’?

Declare any repair costs as the same principle applies, they will lower your CH tax rate. Similarly local property taxes, insurance, co-ownership expenses etc

You will get a deduction in CH for any mortgage on the property. Global debt and interest are allocated between CH and overseas property based on wealth.

It’s pretty clear in the “taxation decision”. In the taxable income there are salary, dividends, primary house and secondary house (deducted the expenses of maintenance and management)

Essentially the second house, that is in other country, is going to increase the taxable income in the same way the primary house in CH does. In the taxes declaration it’s clear that it’s in another country.

Regarding the wealth part it’s not a problem anyway since I have a mortgage in CH

This really shouldn’t happen, as I understand it. Taxable income and wealth can be affected slightly due to the proportional debt allocation as part of the ‘Steuerausscheidung’ that @Barto mentioned. However, net income (whether actual rent income or imputed rental value) of foreign real estate should never simply be added to your taxable in come in Switzerland like domestic real estate.

Does this mean that, according to the taxation decision, your taxable (steuerbares) income is exactly the same as your ‘satzbestimmendes’ income? Or is there a difference but not as much as you think it should be?

Does the taxation decision match the provisional tax calculation of the tax software or did the tax authorities ‘correct’ it? Could you post the relevant excerpt of the taxation decision?

I would talk to the tax person responsible for the decision.

I’m not living in a German speaking canton but it’s really clear. In one one row of the taxable income there is the primary house a the row below there is the second house. Essentially the calculated rental value for each house.

This is a good question, and I was wondering the same. Software and decision are the same value

For your information, the ZH taxation decision I got has 3 parts:

Berechnungsmitteilung: Calculation of global income and assets. Foreign real estate is included the same as everything else

Interkantonale / Internationale Steuerausscheidung: Global income and assets are distributed between ZH and the real estate country. Here the canton column doesn’t include foreign real estate.

Einschätzungsentscheid: Final numbers for “steuerbar” and “satzbestimmend” income and assets. Here the “steuerbar” numbers don’t include foreign real estate but “satzbestimmend” does include it.

Is your taxation decision similarly structured? In particular, did they also include a “Steuerausscheidung” (no idea what it’s called in French or Italian)? That part should be the most interesting one. In ZH also the tax software already generates a provisional “Steuerausscheidung”. Is this also the case in your canton?

If they didn’t include a “Steuerausscheidung”, ask for that.

Edit: “Internationale Steuerausscheidung” might be “Ripartizione fiscale internazionale” in Italian and “Répartition fiscale internationale” in French.

Mine is structured in this way. There is a recap page for Canton taxes.

Income:

-Salary

-Dividends

-Rental value house 1

-Rental value house 2

-Total rental value (1+2)

-Maintenance expenses for houses

-Total rental value minus Maintenance expenses for houses

-Total income value

Deduction:

everything I could deduct and nothing regarding houses

Wealth:

it’s 0 due to the mortgage in CH

Then there are pages similar to what you mentioned and they should be the Steuerausscheidung, because I have a breakdown of two cities in CH (where I work and where my wife works), then the foreign country.

First part is wealth the second is income.

In the income there is house nr 2 as well and it’s under the foreign country and it’s definitely considered in the total.

For federal taxes are exactly the same.

There is another part that I don’t understand. In the recap of the income there is rental value that is adding to all the rest, while in the breakdown actually there are also the passive interests deducted.

Finally in the main page there is the “taxable income” and the “taxable income decisive for the rate” that is 3k higher. So the second value is considered to calculate the percentage of the taxes, then the percentage is used on the first value (I did some reverse engineering since I had no idea).

The second value comes from the recap while the first value comes from the breakdown pages.

I have three columns, “Total Satz” (total to determine the rate), “Kanton Zürich” and the foreign country. In your case I’d expect four columns: total, the two cantons/cities and the foreign country. And I’d expect income from house 2 in the foreign country column and the total column but not in the columns for the Swiss cantons/cities. Is this correct?

Is the difference between the total column and the sum of the Swiss columns 3k here as well?

Do the 3k roughly match the net income of the foreign real estate (imputed rental value - mortgage interest and other real estate deductions)? Due to the proportional application of debt interest, it will likely not be an exact match but you can hopefully follow the calculation on the page with the breakdown between the Swiss cities and the foreign country.

There are 5. Total, Total in canton, city1, city 2, abroad, but essentially it’s what you mentioned

Correct

Yes

After your inputs and checking again the calculations…I finally figured out

The "taxable income decisive for the rate” is including house nr2, then in the breakdown I got confused because the total is considering also house nr2, but then for the "taxable income” is reported only the Swiss part.

The calculations are correct, so no mistakes.

Now I have a question related on why there are two values, and not just one?

Essentially why there is a value to decide the tax rate that includes also house nr2?

It’s to avoid an unfair advantage when income is split across countries.

Let’s imagine there is another country that has the exact same income tax brackets as your Swiss town, and a part of your income is taxable in that other country.

If each country taxed you individually on the local income without adjusting the rate for global income, you’d likely pay less tax than if you had exactly the same total income but all your income was taxable in Switzerland (because you’d benefit from lower tax brackets). Such a discount would be unfair to people whose total income is taxed in Switzerland.

With Switzerland’s tax rate approach, you’d pay in total exactly the same amount of taxes to the two countries in this hypothetical example, no matter how your income is split across the countries. I think it’s a reasonable and fair approach overall. The proportional allocation of global assets/debt may be a bit odd in some cases, though.

Hi @jay I am trying to understand this topic and I am failing, you seem to understand well how the Steuerausscheidung so I’d appreciate your input on the following situation.

In 2022 I have negative income from my property abroad, due to renovations. This negative number is deducted from the Swiss income at point 6.4, as it was in 2019 when I last did similar expensive work that more than offset the eigenmietwert of the property.

Then this number (in the low 5 digits) changes a bit thanks to the Steuerausscheidung and the resulting, slightly higher number ends up in section 26.2 and it is ADDED to the “Steuerbares Einkommen im Kanton Zürich bzw. in der Schweiz”, i.e., more than offsetting the deduction at point 6.4.

In previous years I always had a smaller, positive value in 26.2, which ended up reducing my taxable income so all good. In 2019, when I had again a negative number, nothing was added in 26.2, so I wonder if there’s an issue with the software? Indeed I tried several times to correct a typo in a field and it never got registered. Or perhaps something haas changed since then?

What I ended up doing is not running the Steuerausscheidung and submitting the tax return without it, ignoring the warning. I am sure they’ll correct whatever needs correction.

I don’t have experience with negative taxable income from a property abroad, however, to me it doesn’t sound that unreasonable what the tax software is doing.

If we ignore the difference in the amount between 6.4 and 26.2, it makes sense that your taxable income in Switzerland is not affected by negative income of a property abroad, as it’s also not affected by positive income of a property abroad. I.e., you don’t pay taxes on profits of that property in Switzerland, so why should you be able to offset losses?

With regards to the tax rate it should still provide an advantage as the amount in 25 should be lower than the amount in 27. I.e., you will still pay slightly less taxes in Switzerland due to that renovation (assuming the difference between 6.4 and 26.2 is small enough).

If your main concern is the difference in the amounts between 6.4 and 26.2, it gets quite a bit more complex. I would have to see the Steuerausscheidung but I’m also not familiar with all the details there, so not sure whether I could explain it. The system also has its limits which may result in unfair results.

I don’t know of anything that changed compared to 2019. Maybe the tax software actually did it wrong back then and it’s been fixed in the meantime? I assume in 2020/2021 the amounts in 6.4 and 26.2 were relatively close, so that the net effect of the taxable income in Switzerland was very small?

Does this make sense or am I misunderstanding something?

That’s the “problem”. 27 is higher than 25 because it’s a negative number being subtracted. For that you wrote earlier it might still makes sense as they are basically offsetting again what they deducted at 6.4 (well, not exactly, as 26.2 is 6.4+2K), but in 2019 this was not the case and 26.2 was left blank, which obviously I liked and took for granted. I hope the mistake is now and not in 2019

The differences between 6.4 and 26.2 are small, so I don’t care much, but it’d still be nice if the tax office would provide a detailed explanation of what goes on. E.g., I have no mortgage on the property abroad, but still I get assigned some mortgage amount for some reason.

Interest and debt get allocated between countries and cantons based on the value of assets.

It avoids people taking a mortgage on their property in Switzerland to provide the cash to buy a villa in the South of France, and ending up with zero taxable wealth in Switzerland.

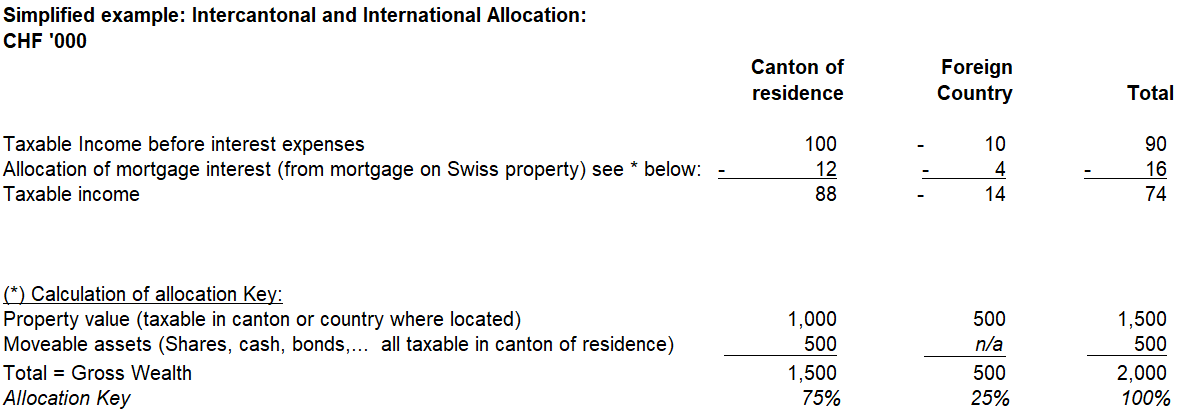

I tried to make a simplified example, not sure if it helps:

In the example taxable income is 88k. Global income is used to determine the tax rate. So the 88k income is taxed at the rate applicable to income of 74k. Thus there is relief on the loss from the property overseas.

Example shows income - similar applies to calculate taxable wealth

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.