I know that the general wisdom is that not being married is an advantage tax-wise - I’m not married as well.

But I was looking into diversifying my brokers and thought that instead of opening a Postfinance account, I could give money to my girlfriend and invest fro mher postfinance account, so that she can keep the 25k investment more easily, particualrly now that after PF increase of 3a TER, we are looking to move her to VIAC.

and of course, in certain cantons (mine is Fribourg) moving money between peoples gets taxed - a lot if you are not married or live together for 10+ years.

In Fribourg, I can subtract 5000 chf every 5 years from money I give my girlfriend. Anything above and beyond get taxed at 22% (!!) which goes down to 8.25% (still a lot) the day we have had the same domicile for 10+years.

So yeah, not marrying is great for taxes, but only if you really are not exchanging money with one another…then depending on the canton it’s a pain. And I can give her 5k in 5 years to invest in PF without taxes. A bit of a shame.

What about a 0% interest loan to your partner?

Would still be taxed as your wealth, but can be freely invested by her. In case you break up, all things are written down and you can claim back your money.

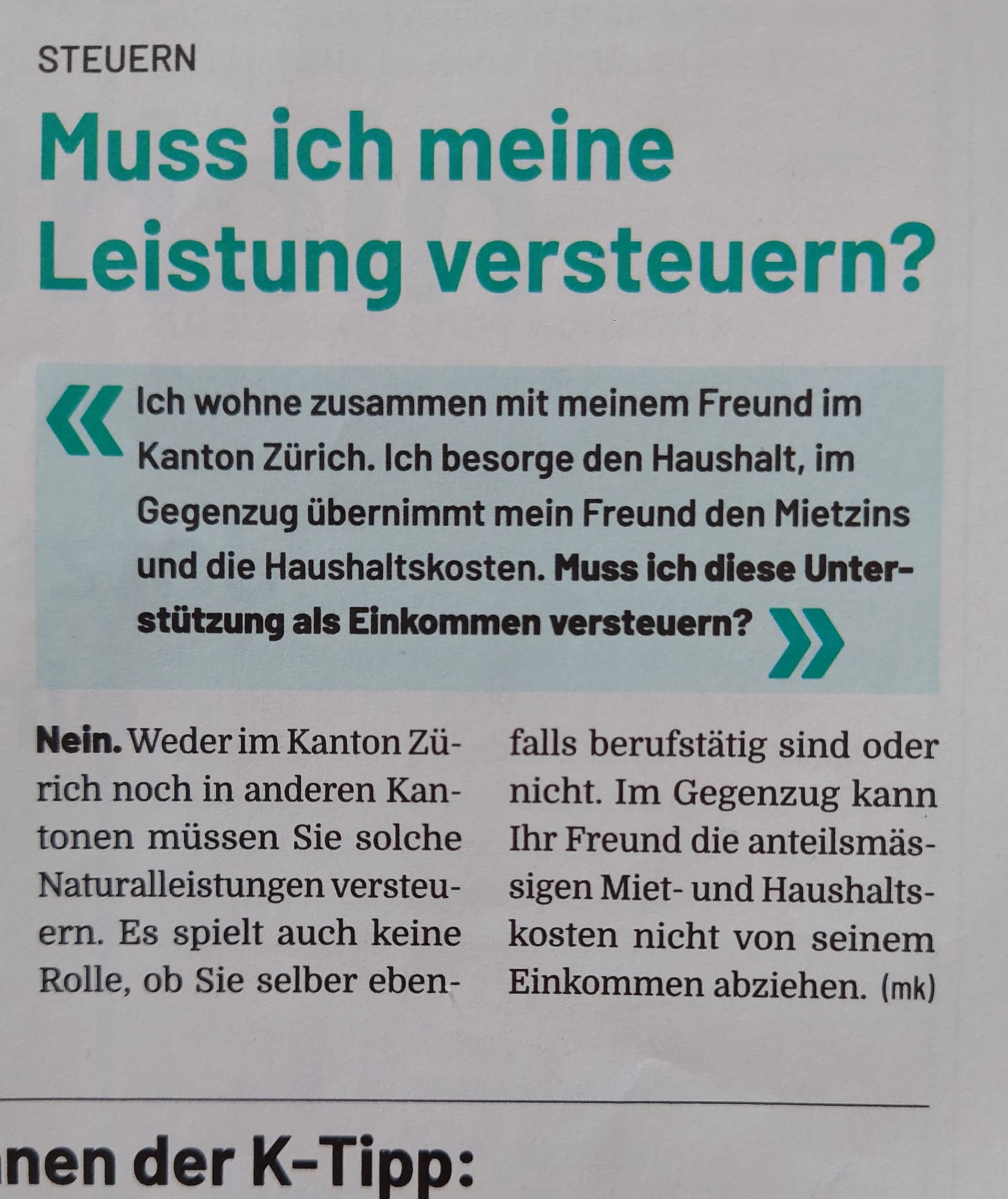

In case you are cohabitating (Konkubinat), it’s possible for one partner to compensate / pay the other partner for household work / child care etc. This compensation is tax free for the receiver.

There are probably other ways of transferring the money, for example by unevenly splitting common expenses (in her favor), resulting in a net flow of money to her.

Some good thoughts here - forgot the 0% interest loan possibility.

The whole thing is really outdated and ridiculous - I mean I can legally transfer, tax-free, to our children. And the children can, tax-free, give it to their parents (the mother).

So in reality it’s already possible - so why there isn’t a direct line between unmarried parents, is burocratic insanity.

Yes, half of kanton have tax free direction from children to parents:

It’s quite funny to see that the cantons who have tax free schenkung to the “lebenspartner”, aka unmarried couple, are the “rural/conservative/catholic” cantons the power of money Schwyz, Uri, Graubünden, Luzern, Nidwalden, Obwalden, Zug like the french says “c’est n’importe quoi”

You misread. It says that if A pays the entire rent, then B doesn’t have to declare that support/payment/… as income, but in return A may not deduct the rent they paid extra.

correct, they cannot deduct it as a support payment

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.