I am looking to allocate a good part of my savings in a “safe” thing (I plan to buy an apartment in the coming years).

I was thinking in $BSV (1.23% yield and very low volatility) but I was wondering if you folks have other suggestions.

I’ve looking into other bond ETFs, but more yield comes with more volatility (which makes sense). I understand I will be exposed to USD-CHF, and I am willing to take the chance, expecting the money-print will slow down and CHF recovers.

If you’re going to buy a flat in Switzerland, then to be truly safe you’ll probably want to limit your currency risk. 1.23% yield means very little when you compare the potential fluctuations of the CHF/USD pair.

Would be good to know when you are planning to do this.

You can still find saving accounts in CHF with positive interest rate.

Another idea would be putting these money to 2a and later withdrawing what you have put there. You are allowed to withdraw the part that you put in 3 years (check) though and your tax office may not like it later and request back tax deductions. And yes, 10% cash rule for mortgage downpayment still applies, I think.

Or you can do a combination of everything suggested.

But looking broadly I wouldn’t separate a dedicated “safe” part of the portfolio at all. You can increase cash and 2nd pillar allocation, make sure you have enough cash for a downpayment, otherwise let your portfolio run as usual. Rebalance half-yearly or yearly I would say. When you need cash, if stocks are up, you sell them, if they are down, you take cash and 2nd pillar and let stocks continue their work. Unfortunately it depends greatly on your current worth, expected savings and the price of the apartment you want to buy.

It is easy to give advices when it’s not my money, though.

I could not see 1.23% on the link you shared, it shows yield to maturity 0.6%

The market expects USD to weaken against CHF in line with the difference in interest rates, otherwise there would be an arbitrage opportunity to borrow in one currency and invest in the other. USD 12m is LIBOR +0.2%, CHF 12m LIBOR -0.6%

A swiss residential real estate fund can (in the short term) loose as much as half what the stocks would loose in a market crash. So, you might have to wait a few month to buy an appartment if you put all the money in it. Probably safer to keep some of the money in a positive interest rate savings account.

If you will be buying the flat within the next 5-10 years, you could consider medium-term notes or fixed deposits. The best rates are still around 0.5% for 5 years and 1% for 10 years. Obviously a balanced investment portfolio would probably yield higher returns over those terms, but if you want fixed interest then medium-term notes are still worth looking at. You can find the best going rates here: Medium-Term Note Comparison - moneyland.ch

Thanks all for your feedback, really appreciate it

Love it, and will seriously consider it, at least for a part!

I computed it myself, based on this year’s dividends so far in 2021 and assuming the same average amount the rest of the year. Not sure why the (big) difference…

Not sure I follow here. US is hitting 5% interest, expectation is already the money print halts and that their interest rates spike which should create more demand for USD, hence increasing its value. CHF keeps being strong and inflation super low, so I don’t see an increase of interest rate for CHF.

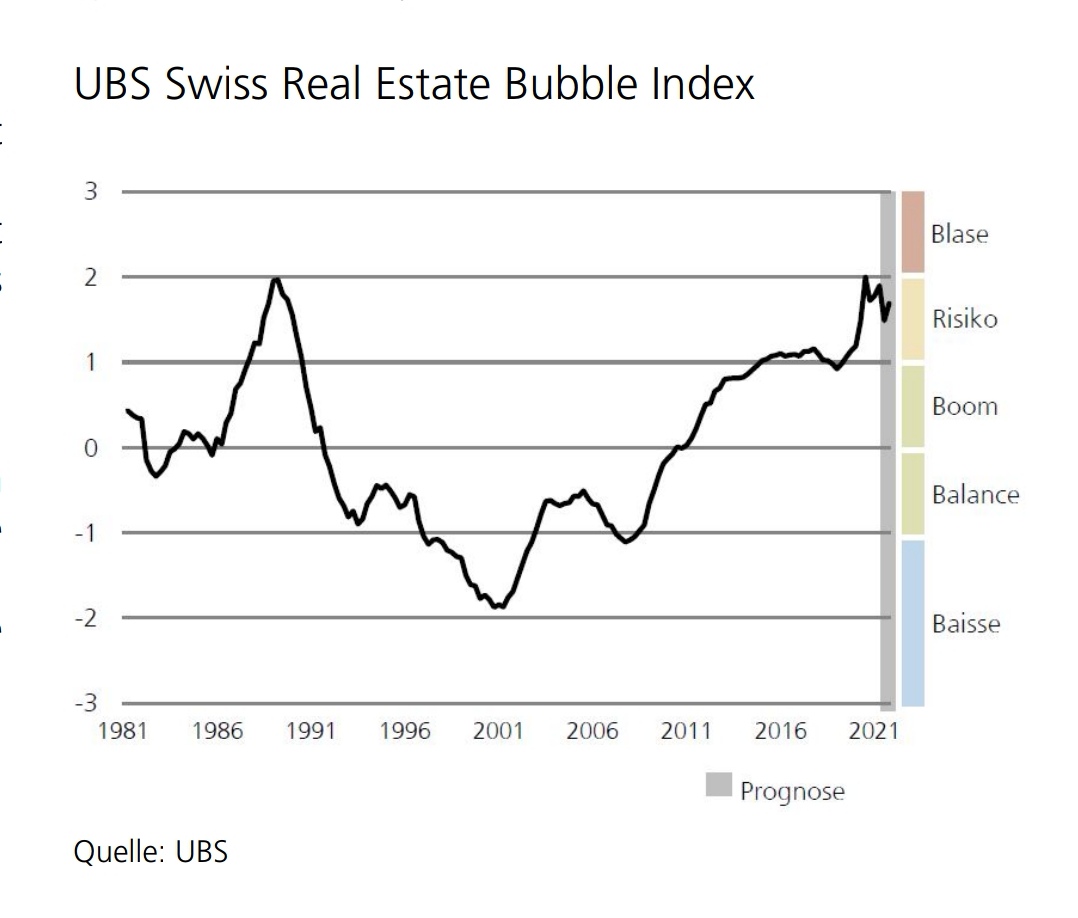

Surprised by this, and will need to do some research before stepping in. Do you have hard data about this? The idea I have is that typically RE is more stable (at least residential). How much did RE in Switzerland suffer in 2009 crisis?

You can see what happend in 2020. The real estate funds index has commercial funds in it, so if you look at the residential funds only, it would be less volatile ofc.

I was referring to interest rate parity theory. In summary investing in USD bonds should give the same net return as investing in CHF bonds, taking into account forward FX rates. Otherwise there would be an arbitrage opportunity that an efficient market would quickly close.

YTM captures not only the interest payments but also the fact that when a bond matures the princpal repaid may be different to the current trading price = capital gain or loss. Note that if the before tax interest paid is 1.23% then this would be subject to tax. If you have a 40% marginal tax rate that would be -0.5%, and after tax yield to maturity would be something like 0.1% (0.6%-0.5%)

The Swiss Real Estate funds are typically leveraged. In simple terms, if the RE companies in the fund are leveraged 5 times they would drop 50% in a 10% RE price drop - So you would only have 50% of your funds to buy real estate that has become 10% cheaper. So not exactly a “safe” placement of funds.

Swiss Real Estate funds need at least 2/3 equity by law. This means that the leverage is lower than your typical family home with a mortgage.

A potential concern is that for Real Estate ETFs the stock exchange price may differ significantly from the valuation by real estate experts. E.g. as per end of July there is a price premium of 44.5%, according to UBS for the SXI Real Estate Funds ETF. Maybe the official valuation is outdated or on the conservative side but still, it’s likely you pay a premium compared to buying actual real estate. On the other hand you get liquidity and diversification. This also means that there is no 1:1 relationship between ETF price and the actual real estate market.

My knowledge of forex/economy theory is limited, and after reading Interest Rate Parity (IRP) Definition, Formula, and Example (your link doesn’t work) I still don’t grasp it, mainly the forward rate. This seems to go against what SNB has been doing for the past years (lower interest rate on CHF to devaluate it against EUR). If the fed increases interest rate on USD, this creates higher demand for it, appreciating its value against other currencies.

I am no expert but the mile high summary is that if the 1 year interest rate on USD govt bonds is higher than for CH govt bonds, the market expects USD to decline. Google “USD CHF forward rates” and you will see it is the case.

Otherwise it would be possible to make unlimited profits by borrowing in CH and buying USD bonds. FX traders and efficient markets remove this possibility for the average investor.

If USD interest rate goes up, keep in mind:

-price of existing USD bonds will decrease

-SNB is intervening heavily in FX selling CHF to buy other currencies, it is possible the FX rate may not change at all

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.