Hello,

in the blog post MP to taxes L1TW/L2TW, we learned USA-based ETF is tax free for US, and 15% could be free for Swiss after declaration the tax forms to get it back. And Ireland-based ETF with US stocks (L1TW) will cost 15% taxes. So, to invest in USA-based ETF, like the VOO is more attractive.

But if I compared CHF/USD over 20-30 years, USD losses. So the question is; “just” to save taxes to dividends, loose a lot of invested value of hundrets of thousands by change to CHF, because USD losses value?

Isn’t it better to stay in the ‘safe’ (or more valuable) CHF? The problem is, I couldn’t find a S&P500 USA-located ETF in CHF. Just Europeans (or Swiss) emit USA-focused ETFs in CHF.

By investing in S&P 500: Choose VOO (USA / USD) or VUSO (Ireland / CHF)?

First of all, as @Burningstone pointed, the trading currency of ETF is irrelevant. It only matters at time of purchase because you might incur forex fee. What matters is the underlying assets and the fact if ETF is hedged for currency or not.

You will not find American domicile ETF in CHF because they are traded in USD in general. You can buy VUSA (traded in CHF) at Swiss Stock Exchange (SIX). It is basically a copycat of VOO but is UCITS ETF (*remember though that UCITs is less tax efficient for Swiss investors in most circumstances vs US ETfs for US exposure but also has some advantages *) . However, it does not solve your concern.

If I understand correctly your concern is that CHF might appreciate against USD.

So lets take an example

Lets say at time of purchase of VOO, CHF/USD is 1.1 and at time of sale of VOO in one year CHF/USD is 1.30

You invested 1000 CHF when CHF/USD was 1.1 in VOO. So basically you invested 1100 USD in VOO

Now at time of sale in 2 years from now, VOO gain 10% and is now worth 1100 x 10% + 1100 = 1210 USD

But then CHF/USD is 1.3 and hence in CHF terms, the asset is worth only 930 CHF. And in other words you started with 1000 CHF and ended with 930 CHF. Not good of course

But you cannot solve this problem by buying S&P 500 ETF in CHF (for example VUSA). And for argument sake, lets say VOO was available in CHF by magic and is called CHOO. Even CHOO will not solve your issue. You need to buy currency hedged ETF for example IUSC to reduce currency risk.

When you invest in international stocks, you expect two types of return/loss

Return of underlying asset (in your example S&P 500)

Return of currency (can be positive or negative). Hedged ETFs try to minimize this exposure.

The problem is that this hedged ETF will not guarantee success because lot of variables are at play like hedging costs, interest rates, actual currency devaluation vs estimated. There is a lot of research around this and results are non-conclusive. I will give two examples

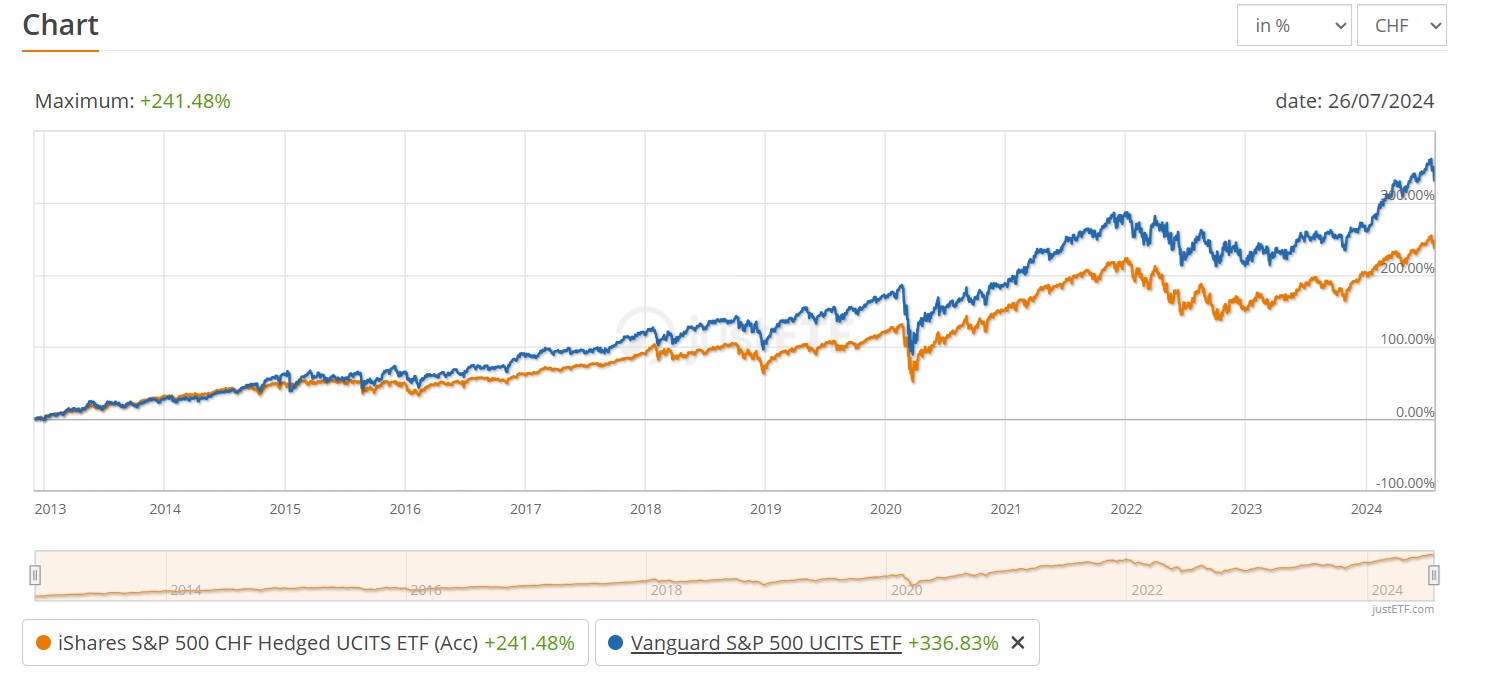

First chart. see chart below, for last 12 years, IUSC (currency hedged ETF) underperformed VUSA (unhedged ETF). It does not mean, it would always underperform.

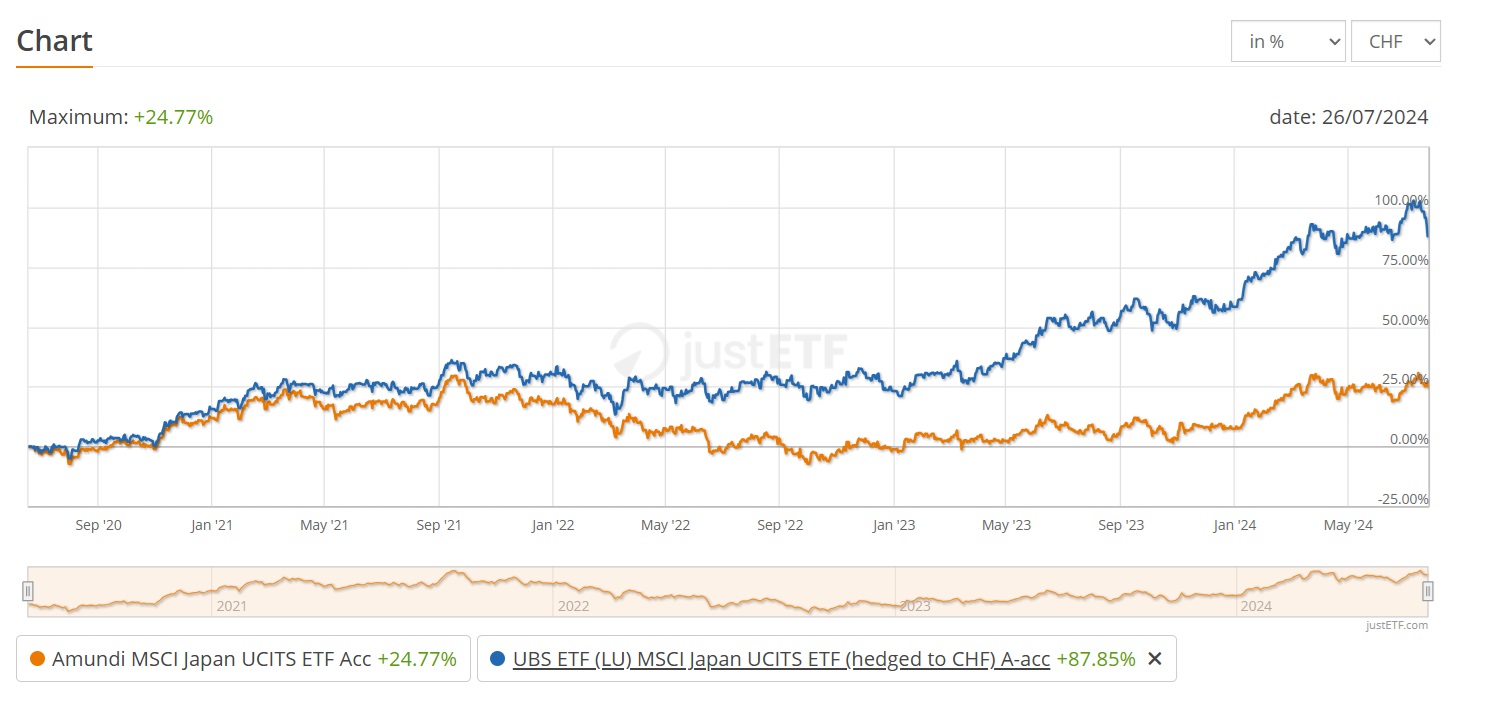

Second chart compares performance of Hedged vs Unhedged MSCI Japan ETF. And in this case, hedged version outperformed because Japanese yen collapsed

I tried to read very complicated articles about hedging and could not come to conclusion. So i decided that if i plan to invest long term in Equities, i will leave them unhedged.

Thank you very much guys for your helpful answers! And sorry for opening a new post for this. I’m not very familiar with these kind of blogs/templates, but now I think I got it more - there are some similar posts. If this one is to delete, please let me know.

However: I think I got it now (a bit self-pain). The value of the ETF/stock is import, not the currency. It doesn’t matter if I hold it in CHF VUSA or USD VOO. If the S&P500 increase 10%, both should increase 10% (without looking to fees, and exactness of copying the index). And if the CHF/USD gets low, it doesn’t matter when I want to sell it, because after selling, I could quickly change the currency back to the start/main currency - that doesn’t change the 10% inscreasement.

I think the mistake in thinking is that the FX does impact you: CHF getting stronger vs USD does not impact say S&P 500 performance, but it means your USD denominated VOO will be worth less in CHF.

However, a CHF denominated S&P 500 ETF will be impacted by CHF:USD FX and that’s the part people forget. And it’s a part that isn’t brought up in arguments, where solely “just the currency of the earnings matters” is brought up. And that’s just wrong. It’s not really that at all.

It’s that the value of your US ETF denominated in CHF is impacted by the FX while the value of a US ETF denominated in USD is not impacted by the FX. I.e. the FX impact comes in in different places. But has nothing to do with “currency of earnings”. That is a separate matter from currency denomination.

I disagree with this. If VOO increases 10%, as USD denominated VOO increases 10%. If the FX changes, VOO in USD is unaffected, so you sell get your 10% higher USD value, but lose on the FX conversion to CHF. If you had an unhedged CHOO in CHF, the value of that ETF would not increase by 10%. The 10% increase would be offset by the increase in CHF value but when you sell then you don’t have to convert back from USD to CHF, so no losses there → in short, the FX loss of an appreciating CHF comes into play at different steps for a USD denominated ETF vs a CHF denominated one. But it doesn’t mean it’s not there.

However, considering that US based ETFs have lower fees and commissions, and FX is cheap on IBKR, it makes more sense to hold USD denominated ETFs than CHF ones.

Thank you very much. Very helpful this point: in a CHF ETF with USA stocks currency effects during holding the ETF (are priced in) vs. by USD ETF with USA stocks currency change effects by selling / changing currency.

So by dividends the same: By first option I get it in CHF, currency effects are priced in. By second I’m free to change USD into CHF or not.

For lower taxes and fees it also makes sense to choose the VOO.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.