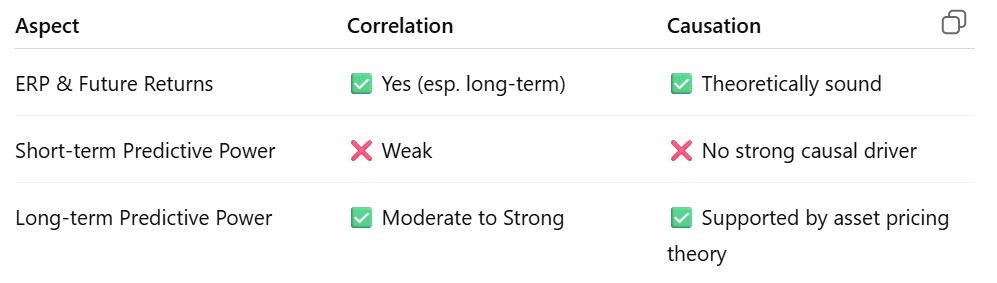

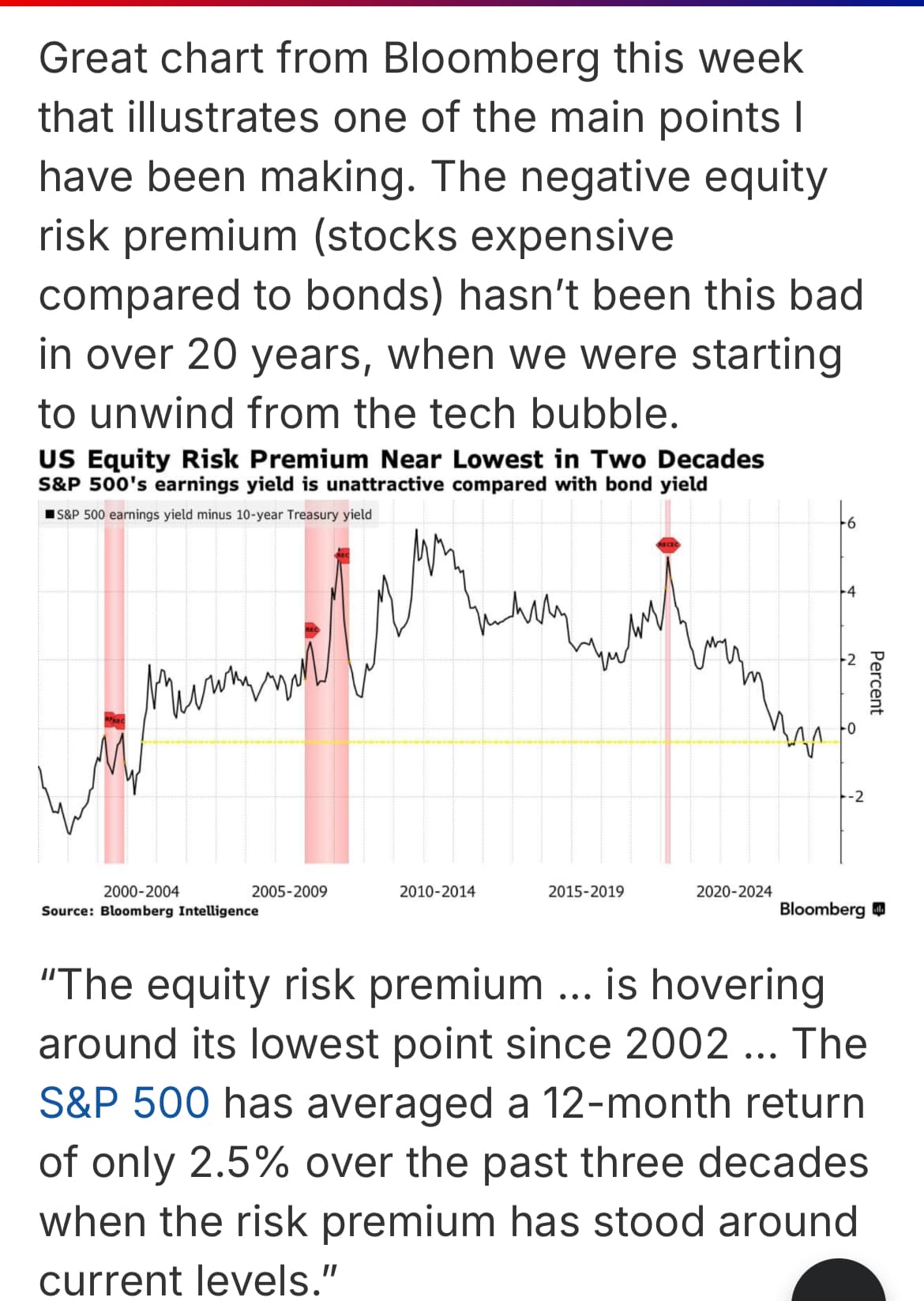

As far as I know for S&P 500 , equity risk premium is calculated as follows

YE = earnings yield from S&P 500

YB = 10 year bond yield

Equity risk premium (ERP) = YE - YB

At this moment it’s negative or close to zero. This number used to be between 4-6%.

You can only say “risk” is still there if people ask premium to take on the risk. If people are buying stocks for same yields as 10Y Bonds, this actually means people are not really concerned or uncertain.

I am talking about people who invest in stocks (active investors or active funds). People who buy index funds are not really setting any price. They are merely providing liquidity to buy stocks based on what other active investors have decided to be the price. So we cannot really look at index fund flows as metric.

——-

I think this is result of long term strong performance by S&P 500. Investors are okay to get low ERP to buy these stocks. But I think then the same investors shouldn’t be surprised if their returns are similar to 10YR US bonds. That’s all

It can also happen that S&P end up delivering better than bond performance due to excellent earnings growth in future . But that’s the unexpected part of discussion.