I have an account in one very small private bank (100+ in the list of private banks according to the total wealth under management), this bank has lower fees than some bigger players. I wonder what could be the risk associated with using small private bank vs some big player like UBS. My understanding is that by Swiss law all my stocks are in Central Securities Depository so in case of insolvency they will be returned to me without problem. At the same time, I clearly save on the fees. Another risk which I might underestimate is fraud, in this case not sure what might be consequences for my account. I think one way to mitigate this risk could be to request some documents to verify that all my securities are really stored somewhere safely (but what if they fake this document, unclear).

I have worked in a small bank and these are some of the observations I have made. Small banks have less staff and with multiple roles and therefore less specific know-how. Having a bank license costs at least CHF 10 Mio per year which requires at least 1 billion of assets under management to be economically sustainable. Many services are outsourced and small banks have less leverage to get issues resolved.

The risks you might encounter as a customer with a small bank are:

- more prone to make mistakes due to lack of scale and lack of know-how

- longer time for issues to resolve due to more third parties being involved

- smaller product offering due to cost of running processes for each product

- higher prices due to outsourced services and lack of scale (strangely not the case with your bank)

- more prone to go bankrupt due to more impact of single events (credit loss, fraud, trading error, single large client leaving, etc. Credit Suisse hopefully was the exception to the rule

)

) - less digital tools due to high cost of developing them and lack of scale

- less maturity in the implementation of processes and regulatory requirements

After making sure your bank is FINMA-regulated, you could ask them about risk management measures to address your specific fears.

In case of insolvency you have to understand that it might take a while to get your securities back. It might also take a while to get your cash even if it is insured. I know of a case where a small bank went into voluntary liquidation, hoping they could serve all clients by revoking the loans. Turned out that after a year, these hopes were squashed and only then a bancrupty was declared, allowing for the deposit insurance to become active.

it is FINMA regulated, category 5 from the FINMA report dated today actually (https://www.finma.ch/en/~/media/finma/dokumente/bewilligungstraeger/pdf/beh.pdf?sc_lang=en&hash=4ADA6BB475CA6AD29F1A491FF66DEFAE)

Generally, there are some many small banks there and it is unclear what is the difference between their services. If all of them use custody account for stocks, the risk of all of them is approximately the same. The only measurable difference to me are fee for FX, fee for buying/selling stocks, custody fee, service fee.

I understand your suspicion. After all, it is your hard-earned wealth. Also understand that banking is one of the cornerstones of Swiss economy. While banks might charge high fees and engage in some unethical behaviors, they need to build trust and confidence. Thus they do not falsify documents or do illegal things. And they would want to weed out peers who do.

In a scenario where SHTF (as happened in the subprime crisis), banks stop trusting each other and restrict transactions and may even close shop for a couple of days (banking holidays). As long as you do not engage in trades that require you to sell fast in time of crisis and as long as you do not need a lot of cash fast, there is not much to fear.

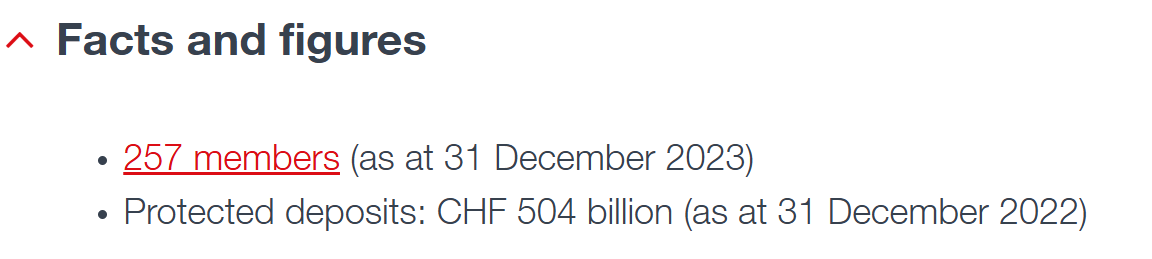

Be aware that the Swiss deposit insurance is covering only 7.9 billions out of 504 billions protected deposits. That’s 1.5% of cash if all insured banks fail at the same time.

Do you think there is any value in having two private bank accounts to reduce the risks? What could be the criterion for choosing the private bank (category from FINAM classification maybe, beside of fees)?

Yes, don’t put all eggs in the same basket if you have more than 100k. Being very cost-sensitive, I mostly bank with low-cost institutes and do it across jurisdictions. Also try to have a category 1 or 2 bank on standby, should I ever want to get another mortgage or do other business.

I’m currently using

- IBKR (UK), Swissquote (CH), Consorsbank (EU) for brokerage

- Revolut (LT), Neon (CH) for payments

- ZKB (CH) for more sophisticated matters

- Frankly (ZKB CH) for pillar 3a and vested benefits

- VIAC (WIR CH) for vested benefits

I have used in the past

- Degiro (D), Migrosbank (CH) for brokerage

- Postfinance (CH) for brokerage and payments

- Spuerkees (LU) for payments

- Credit Suisse (CH), UBS (CH) for mortgage, brokerage and payments

- Schwyzer KB (CH) for vested benefit

Why did I change? Some banks were unfit for purpose. Others were no longer necessary when I moved countries or got a divorce.