I will not raise the topic again about rental guarantee insurance vs deposit, I refuse to pay 4%+ for interest for my rental guarantee, but on the other side, having it blocked at 0.1% (the best I can find, CLER bank) is kind of stupid. Our next move will more than double the guarantee required (the rent didn’t double, just where we are they asked for less than 2 months warranty) and it will block even more cash (not even counting the transition until the previous guarantee is free up).

I cannot understand why they require so much money, the flat is old and only expensive because of the location, not the value of the equipment/building. And in any case, if we damage for more than guarantee, we will still have to pay for it anyway, so I don’t get how it’s still a thing.

Isn’t there a solution to put equities (ETF) or bitcoin as guarantee, so it continues to gain values in the meantime? I would be ok to put 50% more in this case, as I want to invest some money anyway. If there isn’t such solution, why not? Swissquote or any other bank could offer that and get more customer investing and paying the usual fees for investing, they just have to ask for the landlord approval to close an account like a normal banking rental guarantee account.

Would be interested to know if anything like that was already discussed and what do you think about it.

EDIT: it turns our it exists already, thanks @Guillaume_GVA

The guarantee is also there to cover scenarii where you fail to pay rent for some time.

A 3 months guarantee is standard. If that’s what they’re asking for, I wouldn’t fight it too extensively or try to mitigate it and I’d just consider it the cost of renting that specific place. I may reconsider depending on other factors (mainly availability of competing items) if they are asking for more than that.

I have no knowledge of an investing product for rental guarantees. As nabalzbhf puts it, it sounds counter productive to the purpose of the deposit. In order for it to work, like it does for mortgages, you’d either need the bank to be the counterparty or for it to issue a fixed guarantee to the landlord, while allowing you to invest the difference. That guarantee would be costly so I don’t know that it would fit your criteria as to how much you are willing to pay to still have your money invested.

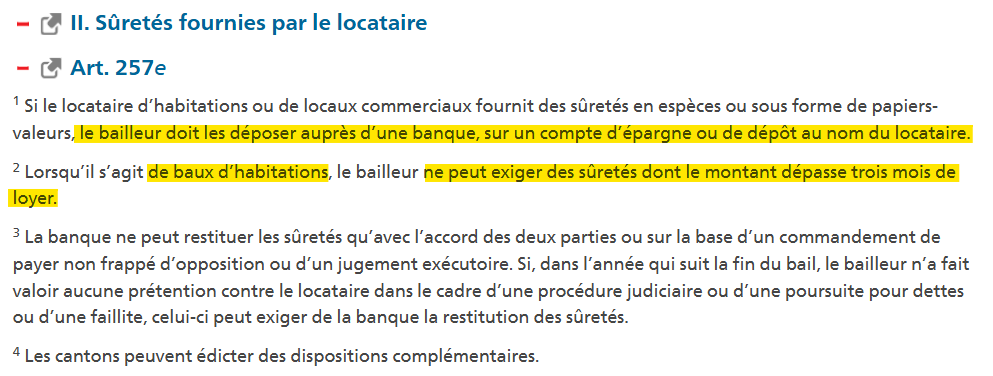

Extract of the law on rental deposit (art. 257e) - Fedlex

Up to 3 months of rent as deposit. I’ve never seen a landowner asks for less. However, the 3 months are a maximum. Perhaps you have the option of negotiating a lower deposit (unlikely to happen).

The full paid-in deposit of up to 3 months rent is guaranteed by Evorest, even in a market downturn. If the markets are performing well, the deposit coverage is even higher than what was paid in

As usual, the marketing speech is prominent and it’s not that easy to find the actual legal conditions that apply (I haven’t but haven’t searched for long). I’d be interested to read them.

Great! Thanks for finding it, I knew it would be a good idea, proof, someone did it before me I search for half an hour, on Moneyland and Comparis and even direct internet search but didn’t found it (price to pay for not using Google maybe).

0.6% fee for 75% invested, not so bad, better than sitting at 0.1% or paying 4% a year for nothing.

I have anyway ETF on a free Investart account that I was looking to close as I have already a regular IB account (and Investart just manage a separate IB account for you). So If I sell these ETF and buy more or less the same with Evorest, it will not be a huge risk on my side. Even when I change flat or if I don’t need a deposit anymore (like buying a house in the future) I can always buy in or out of IB with same or very similar position, so long term I don’t have much risk of bad market timing.

I’m not sure what you mean, but usually I try to avoid complex investment scheme, I stuck to global ETF or Bitcoin, no leverage. I did try some collateral with crypto to get cash and it didn’t turn well, was liquidate during a flash crash of less than 1h, could never buy back at the liquidation price or below, so I’m not willing to try again unless I find a product with non-liquidation guarantee or something (like you have x hours/days to see if it recovers or to reinject the difference if needed).

If the rental deposit is invested in ETF, it is not anymore insured by the “Einlagesicherung” but it now belongs to the “Sondervermögen”. Or am I wrong?

The “Einlagesicherung” would only come into play if you don’t invest the money (which is the whole point of Evorest).

I think in theory this system could work well with a “margin account”-like system. So, for example, the landlord demands 10k of deposit, you can open a special brokerage account where the value may not go below 10k or it will be margin called. You can, for example, fund it with 20k initially and then just invest in stocks and even withdraw some of the returns when the portfolio is doing well.

Not sure if this is allowed by law and if yes whether it’s implemented by someone though

You are right, their statement is a bit stretched. Only the cash component is insured. The invested component is booked in the name of the client, so safe from a HBL bankruptcy anyway.

Also they could remove the threshold of 100k from the statement and move it to the notes, who has that much on a rental deposit account anyway?

Actually it kinda does. From their FAQ, if the value of the portfolio drops below 80% of the initial deposit they will require the customer to top up the difference. I would assume that if the customer does not comply they will liquidate the positions to cut their risk.

I wonder how they are planning to approach a large market downturn where a large chunk of their customers may have to be contacted to top up their accounts…

I would give my tenants the option for something like Evorest. But they are pretty thight lipped with their “guarantees” on their website. I don’t understand how they guarantee the deposit, so it is a no.

The same is from the tenant side. The fees are declared nowhere, the ETFs are declared nowhere. The only reason can be that those are bad.

0% on CHF everywhere else is interest above market rate and a good deal. Combined with competitive leverage that could probably beat 0.5% fees.

I assumed this is eventually described in some kind of terms and conditions which are not linked on the website but should be made available at product opening.

They do described high-level how the claim process works in their FAQ. However, they do not detail how they rule if property manager and tenant do not agree. Imho, the ease of dealing with them in case of dispute is what makes the quality of the product from a property manager point of view (beside the guarantee itself).

The fees are declared nowhere, the ETFs are declared nowhere.

What do you mean? The bank is never involved in the disputes between property manager and tenant. They will pay out if there is a mutual agreement between property manager and tenant or if there is a court order.

Die voll eingezahlte Kaution von bis zu 3 Monatsmieten wird von Evorest garantiert, selbst bei einem Marktrückgang. Wenn sich die Märkte gut entwickeln, ist die Kautionsabdeckung sogar höher als der eingezahlte Betrag

I don’t unterstand the last sentence. Would they pay out more to the landlord if the performance is good? I thought all the performance wins (and losses) will go to the tenant.

I would assume that the profits belong entirely to the tenant (minus fees). However, if you have damage that must be paid for from the rental deposit, then the landlord can also use the profits, as they are legally speaking still part of your rental gurantee deposit. But that’s just my guess.

I saw that, but I assumed that can’t be everything. A startup guarantees me the difference between what is in their client’s account and what those clients owe after a 20% drop? Where would they have that much money?

What happens if there is a market downturn when I move out and I have caused a damage?

(..) In the unlikely case that you have caused a damage that is higher than the value of your deposit, you will need to liquidate your investment and compensate the difference between the damage and the liquidated value of your deposit.

This raises the question of whether you would then have to collect this directly from the tenant (meaning Evorest would be off the hook) or whether Evorest would advance the difference and then claim it from the tenant. IMHO, both pose an increased risk for the landlord

EDIT 1: according to FAQ:

What are the downsides of using Evorest? Is there any risk for me and the property owners?

There are only upsides and no risks attached to using Evorest. Even if an invested deposit falls below the paid-in amount, the property manager has no risk, since the tenant and in second priority Evorest guarantees the full paid-in deposit to the property owner.

EDIT 2: I find a company that says “There are only upsides and no risks" not entirely honest. Because there are always risks. And they should be named transparently.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.