This is all good, still it may not apply to all circumstances, especially here in Switzerland and for FIREd people who do not qualify for a mortgage renewal… then, what are the options left ? A margin loan may be the lesser evil.

For example: my mortgage is due for renewal in 2029. If all goes according to plan, I will have no income by then. My wife may still be working but only at 50%, with a relatively low salary (by Swiss and this community’s standards), so we will not satisfy the 33% rule—in fact, we may reach only about half of the required income.

My wife does not want to sell the house for the foreseeable future…

So, I see the following options:

Fully pay back the mortgage by selling corresponding assets (I don’t want to do this, as it would eliminate the cash flow needed to bridge the gap to retirement age—we cannot eat bricks and mortar ).

Pay back enough of the mortgage to satisfy the 33% rule, by selling assets (again, I don’t like this for the same reason as option 1).

Pay back enough of the mortgage to satisfy the 33% rule, by taking a margin loan.

Fully pay back the mortgage by taking a margin loan.

Pledge Rely on liquid assets as “pseudo-income”, likely by moving them to the mortgage provider—possibly with worse conditions and uncertainty about how much they will be valued at; this probably would not take us very far, as the safety cash flow calculated by the lender would likely be very low.

At the moment, I think I will have to lean toward option 4, but I’m open to hearing any other suggestions I may not have considered.

Suggesting to see the recent mustachian blog article, including the comments. For simplicity I’ll repeat here my comment to the article : Banks can calculate an “income equivalent” from your capital, using a conversion rate. This was confirmed by MP himself. Other options are also discussed.

Sure, this is option n° 5 I have listed. Still, considering a 5% “pseudo-income” I would need at least 2M CHF to be eligible, if the wife will also stop working before the mortgage renewal time.

Maybe a combination of this + some partial amortisation… for sure before the time comes it may be worth to check with some specialised consultant whether there are banks / insurances willing to consider a higher % of “pseudo-income”.

I wonder if the lenders after having granted the mortgage do regular checks that this % criterium is still fulfilled (may not be the case in the withdrawal phase).

Maybe someone who has already followed this path could provide insights… @Financial_Imagineer ?

That was indeed your option 5, sorry I missed that.

FWIW, my “too big to fail” bank did not require us to move the assets. Only ~30% of our portfolio is with them, but all of it (based on tax declaration) was taken Into account to calculate an income. Of course they would have preferred to receive additional funds, but I also made it clear that other mortgage providers exist…

I just stumbled on this option 6 (Reverse mortgage). Did you consider it ? Any thoughts ? It appears that it is mainly restricted to people close to retirement age (60+) but it may be an option worth further exploring…

Not quite, since no pledging or moving of assets is involved. Have you done the affordability calculation if you add 3% or 4% of your invested assets as income?

Option 7a: Renew your mortgage early, should be possible up to 2 years in advance.

Option 7b: Check with your bank the cost of ending it early

If you stick with your bank, will they even re-do the affordability check?

Right, my use of the term ‘pledge’ was not entirely accurate, I amended my comment accordingly.

(At least partial) moving of assets on the other hand is not so unlikely, from what I’ve read so far

Sure, as I mentioned in my response to jmp, even considering 5% I would land quite far away from the required (pseudo)-income

Right. These are also options I didn’t list. I may explore them in due time

no idea (in my particular case it’s not even a bank but an insurance company) and there’s no guarantee whether they would - or wouldn’t - do it. That’s a big uncertainty I’d rather avoid in my advance planning, given the potential consequences…

Actually, I’m wondering about these questions now (1. subletting income in general, might be house mates or airbnb type renting out and 2. contract starting in the future)… does anyone know? @Cortana maybe?

Ah I mis-read that. Don’t get me wrong please, but if you’ll be far away even with 5% assumed return on assets, do you have enough or maybe too big a house to stop working by then?

I guess you do, since you already could pay-off the mortgage, just wondered about the numbers (I know it’s not part of the original question).

Since you mention the 33% equity in option 2 and 3, is there a chance the lender might re-evaluate your house by then (higher, of course)? That might get you there without additional amortization and has an impact on the affordability calculation.

My bank indicated they can or would do that after 3 or 5 years, without me asking.

The question is pertinent; however, my intention with this discussion was not to delve too deeply into my specific circumstances, but rather to generalise the issue, so that any suggestions arising from this thread could be applicable to others as well.

The real issue lies in the rules applied by banks for mortgage granting or renewal. While these are restrictive for good reasons (the country does not want to face a ‘subprime mortgage crisis 2.0’), in my opinion they are too generic, and more freedom should be left to lenders to assess the specific situation of individuals.

Leaving aside, for simplicity, the 1% fictive maintenance cost: why should a fixed-rate mortgage be assessed using a 5% fictive interest rate? In such cases, the borrower’s obligation is clearly defined upfront (e.g., 1.5% yearly interest for 10 years), so the lender should reasonably ensure that the borrower can meet that specific obligation. If, after 10 years, rates skyrocket and the borrower no longer meets the conditions, then so be it — but I don’t see why they should be denied the initial loan (or its renewal) based purely on a hypothetical scenario that may or may not materialise years down the road. Of course, SARON or variable-rate mortgages are different and should be evaluated accordingly.

That said, there is nothing you or I can do to change these rules… (which is why I am exploring other options)

Regarding my specific case (in response to your question): if by 2029 fixed mortgage rates rise to a level I am not comfortable paying, I would indeed consider selling the house and moving to something smaller (or renting, or another arrangement), as I would not want to lock too much of my net worth into the property. However, this is not a scenario I am currently anticipating, as I do not expect interest rates in Switzerland to skyrocket in the next four years — and if they did, my investment returns might also rise accordingly.

With the 33% I was referring not to equity, but to the affordability threshold whereby mortgage costs should not exceed one-third of one’s income.

As a side note, in light of this criterion, a property revaluation could actually work against you, since the 1% fictive maintenance cost would also rise accordingly (5% mortgage + 1% maintenance < 1/3 income).

why should a fixed-rate mortgage be assessed using a 5% fictive interest rate?

[…]

If, after 10 years, rates skyrocket and the borrower no longer meets the conditions, then so be it — but I don’t see why they should be denied the initial loan (or its renewal) based purely on a hypothetical scenario that may or may not materialise years down the road.

[…]

if by 2029 fixed mortgage rates rise to a level I am not comfortable paying, I would indeed consider selling the house

Because you wouldn’t be the only one looking at selling in that case, cratering the prices and making a lot of people underwater.

I don’t know if 5% right or an overcautiousness from the 90s crisis, or simply not updated for current times. But you do not want people to have zero error margins. Can you imagine if essentially all the people that had to renew mortgages during 2022/2023 were no longer eligible? You can’t just say “so be it”.

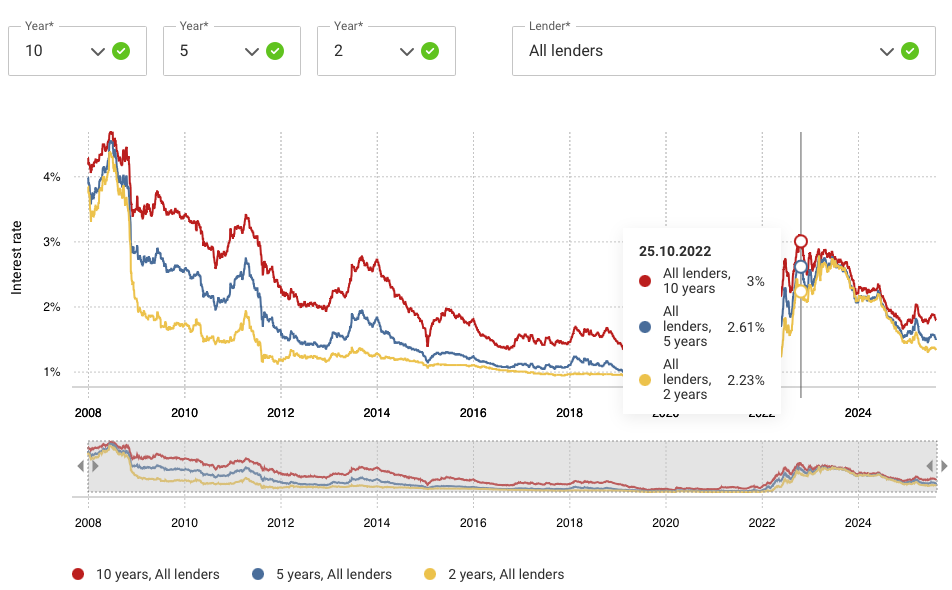

First, how likely is it that all people who have to renew at the local peak in 2022 (where - according to comparis - 10Y fix was at 3% - and one could also choose a shorter duration, e.g. 2Y at 2.23%) will fail to meet the affordability criteria?

Second, in a real crisis, people could lose their jobs — in which case they would fail to meet any % (be it 2%, 3% or 5%)

Third, how is it preferable to force people who are already home owners to sell their property today, because they do not meet ‘fictive’ affordability criteria, supposedly to prevent a situation where they ‘might’ have to sell tomorrow, if they could not actually afford the mortgage?

If you are the bank it is preferable (econmically, maybe you need to consider reputation too) to sell if the owner cannot pay. This way, you hopefully recover enough from the downpayment that you don’t incur a loss.

Second, in a real crisis, people could lose their jobs — in which case they would fail to meet any % (be it 2%, 3% or 5%)

OK, but if they keep their jobs and floating rate increases to 5%, at least they don’t lose their home.

The owner may have amortized, for example, 50% of the property value, in which case the likelihood of a loss for the bank is relatively limited. This is why I believe the situation should be evaluated on a case-by-case basis rather than through a generic rule.

Anyway, as I mentioned earlier, I don’t think debating the rule will take us far, since we have no means to change it. It’s better to focus on identifying the best available solutions to achieve the goal (for me, that means avoiding being forced either to pay the full property value in or to sell it ).

If the owner has amortized to 50%, then the original 5% interest that they could afford would be equivalent to 8% interest on the reduced principal. 5% of the reduced principal would be 3.125% of the original principal (assuming 80% borrowing initially).

I don’t want to be the party pooper, but given the circumstances of having to refinance house you might be better served working a few extra years to pay down the mortgage.

Or do a large voluntary 2nd pillar contribution this year that you can withdraw in the 4th year to pay down the mortgage.

And go talk to your bank. If they are negative, you might already start looking for an alternative loan provider.

I heard from a friend of mine which was in a similar situation and checked with ZKB, without income from a Job they requested assets of around 6m for a mortgage of 1m… so they are not very risk tolerant in such cases to say at least…

My friend decided to sell the house and buy a cheaper one without mortgage to have peace of mind.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

).

).