The majority of the population is renting.

3 Likes

And myself, as a owner who is currently renting, find that the non-deductibility of interests and works is not worthwhile the immediate possible small tax gain.

1 Like

And/or has debt.

Indeed the debt part is a good way to drive your tax down to whatever amount you like. Just a simple currency carry trade will lower your tax bracket and your tax to almost zero if you want that. On the currency carry trade the debt interest difference is deductible, the capital gain is free of tax.

1 Like

What about the majority of the voting population (that actually vote too)?

1 Like

I remember reading it was still slightly more renting than owning, but not that far from 50/50. At least for those eligible to vote. (As a aside “people that actually vote” is hard to define because most people vote, just not all the time.)

The more striking figure I remember is that the median voter is over 60.

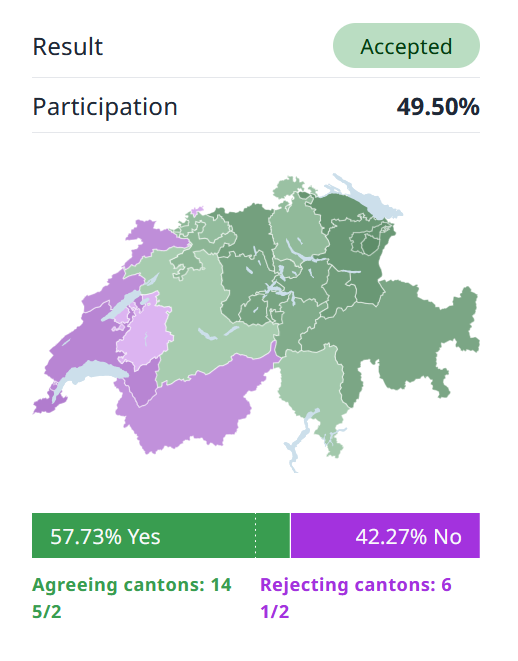

Looks like it’s decided 58% so far (as expected, but not that clearly) for the removal. Abstimmungen live - Hochrechnung: Hochspannung bei E-ID, Eigenmietwert abgeschafft - News - SRF

3 Likes

Futures just got a lot more attractive.

2 Likes

I think it’s a mistake, but so be it.

It will be interesting to see the consequences going forward, although things like housing stock maintenance will take decades to see the actual outcome.

I guess it will actually become law sometimes around 2027? I wonder if there will be a frenzy of renovation until then.

So I didn’t really follow this topic much.

But TLDR -: imputed rental income is going away & so is the deduction on debt interests from taxable income. Is this right?

There is absolutely no doubt about this

1 Like

This only applies to owner-occupied properties. Costs, maintenance and interest for rental properties can still be deducted. In essence, those who have paid off their mortgages and whose properties have increased in value will benefit, while those who have bought recently at high prices will lose out.

The state estimates a loss of tax revenue of between 1 and 2 billion, but does not specify how this will be compensated for. It’s another vote like the AHV one, where something is voted on (and won by the boomers for their own benefit) without any consideration given to how it will be funded.

9 Likes

Sometime back there was a news about revision of wealth tax value for properties in Switzerland. Maybe that would help compensate partially the offset.

Thanks for the highlights.

btw - is it really common for people to pay off their mortgages in Switzerland? I was under impression the norm is to max out at 35% of equity because home prices are so high.

What do you mean?

Or rather, margin loans and mortgages became very bad.

Maybe if you can structure it so the loans are wrapped in a company or fund, and then put that against interest intensive, high capital loss securities like: cat bonds, P2P lending, high yield government/corporate bonds, high yield crypto. But diversification is questionable, so you need to think about implementations to inject cash quickly if there are problems (in both directions, into and out-of the wrapper).

Mortgages are subpar, because their asset is real estate, which has a significant capital gains part.

Futures are downright simple to implement correctly in comparison.

It used to be when interests rate were like 7%. It wasn’t that long ago.

There will be a premium for newly built properties while old ones will only be valued at land prices. I guess we won’t see an end to the trend of tearing down everything and building new lol. One alternative might be to transfer the property to a company and pay a rent. Don’t know what such a transfer implies in terms of taxes when it happens.

Adding to what others said: that also applies to any and all debt. So no more car loa or margin loan deductions etc

2 Likes

A wild guess: Households continue to take care of their property and decide whether to amortize or stay leveraged? Or whether to buy or lease a car? Banks will continue to offer mortgages as it’s a relatively stable business. House prices continue to be set by supply and demand. Renovation-related trades offer competitive services and innovate to stay attractive without tax advantages?

In short: Nothing at all.

Now SRF labels it as a conservative vs. left-winged vote and just neglects those poor individuals that lose the tax-advantaged carry-trade or margin trading. Might be just a small faction, after all. ![]()

My 2c on the consequences:

1- renovate all you can until the law comes into effect

2- no renovations for multiple years (10-20 ?) while people amortize their debt instead

3- many small companies active in the field will suffer/close

4- old housing prices go down

5- but today’s new housing will be old in 20 years too, so all housing prices will go down

Of course, all of these in slow motion, this is real estate after all