Yes of course. But we’re dealing with some kind of a paradox. It’s one of the most desirable places to live with one of the highest salaries, but many people still cannot afford their dream home. I have many friends back in Poland who are earning much less, but they can afford a house.

I guess this predicament can also be seen in Silicon Valley, maybe even more acutely than here.

You get a lot of great things here, but you give up the dream of owning a piece of land. I wonder if there is a way out of this. I like to live here, but I don’t want to put 100% (or more) of my wealth into real estate.

But you won’t. Or better at the beginning perhaps yes but then you will diversify into whatever you want, provided that you have enough savings.

I think we discussed the house topic a thousand times. I agree with many of your points:

RE in CH have low yield

RE in CH does not have large tax advantages

Etc.

However you need to look at your specific needs. RE has a role in the portfolio of each of us. Maybe not in Switzerland but elsewhere.

The emotional element of not owing where you live is a different story. Some people care, others not. But if we strictly speak about investment, RE is a good way to leverage. You would need to pay rent so you offset that cost. Also many people are not discipline enough to timely and exhaustly invest all the spare cash into the market.

Regarding a dream home while working in Zurich: you can clearly forget about it, unless you become a big boss, find a sack full of banknotes while walking in the forest, or accept long commuting trips.

But you could consider a buy-to-let solution, where you could settle in when you retire, or that you consider just as an investment.

In Geneva a relocation agent could charge 3500-8000 chf to access their listing and organise up to 12 visits.

That’s a shame that the housing market is not as transparent as other countries.

For the last two years it kind of felt like this. My wife and I are very fortunate to live in the agglomeration of Zurich for under 1.5k per month. We saved our money like maniacs in the year of 2022: Our assets increased by 98k at the end of 2022, while our 3a and stocks took a battering. But because we always dreamt of buying a house with land, we never thought of investing the money long term, because we wanted to have cash at hand when the time is right to buy.

So now, after a year of excessively saving money, we finally thought: “Yes, well done! We saved a lot of money, we should finally be able to buy something!” While saving we kept checking the market and noticed that we just can’t keep up with the price increases in the region of Zurich. A 20% increase on houses valued 1-1.5mio is a lot of money. We realized that we will have to start looking at houses in Aargau, to still be somewhat decently connected to Zurich.

We now meet the criteria of the banks (Tragbarkeit, Eigenkapital, etc.) to buy a house valued at around 1.25mio. We do not want to pledge or use any money of our second pillar and the little money we have in 3a is not worth considering. But the rates are too damn high now: 3% on a 1mio mortgage is a beast of debt. Adding to that the amortization and additional costs, we would almost be paying 4.8k per month to own our own roof. This is just not a price I am willing to pay, when comparing it with common rental prices (not even considering what we are currently paying).

The whole situation just frustrates me:

Finding the right house and negotiating with banks takes a lot of time, especially as a U.S. dual citizen.

Saving money on something you simultaneously can’t afford, because housing prices increase more than your savings.

Opportunity costs: I could invest the money instead of wasting my time in this rate race.

And our financial situation is about to change too. We are expecting our first baby in about 6 months. After that we both want to reduce our pensum, which means we will no longer meet the criteria (Tragbarkeit) of the banks. So in the back of your mind you constantly think: “We have to do it now, right? Otherwise there is no chance.”

Thanks for for expressing my thoughts in a relatable way! I feel your pain.

If you mostly work from home then that’s ok. But if you need to commute 1h to reach Zurich, even for a silly brunch, this is a recurring nuisance. Also, taxes are a bit higher in Aargau.

And I’m sure raising a child in a house would be much more comfortable. But that’s just a 1st World problem, I guess .

Well then you‘ll never own something which meets your expectations. We are aiming for 10 million people with no room for expansion. Population density keeps increasing. Prices just won‘t get down as it seems.

Demand is still increasing, I see it first hand. It puts my dream of owning a house with land (currently in an apartment) out of the picture.

This is the key. There are buyers that are out priced, but the supply is so limited that it does not matter. It looks like there is always a buyer ready to take over.

I guess this goes a little against the grain in the real estate thread, but I just don’t understand the mindset that owning a house = success in life. There is no universal right to owning a single family home and for sure we should not design our housing around it. It’s also not a sign of a good economy if everyone has their own EFH, it’s just a sign of sprawling development. Switzerland is already destroying a ton of nature and paving it over just so people can fulfill their dream of living in bumf*ck nowhere-Wil and then drive 45 min to work every day. This kind of sprawling development is terrible for quality of live, see North America.

Living in a city is great. I can walk to a forest or a river in 15 minutes. I can bike to the lake in 10. And yet I’m at HB in 15 minutes by tram. I have a lot of greenery around my place and there is a school nearby if I ever want to have kids. How would my life improve by moving somewhere in Aargau just so I can own a house? “You can’t raise a family in the city” is some weird boomer mindset that hasn’t been true in half a century.

The problem is that there’s 1) not enough housing buying built in places where people want to live (a.k.a. please build in Zurich and not Rüschlikon) and 2) People often can’t buy a flat, most are just to rent where you can be evicted.

For the record I’m not saying owning a house is bad, but we should not glorify it, and it’s also not really what improves people’s quality of life. I don’t want CH to turn into another USA or CA.

All good points. I’ve been to Florida recently and yeah, not looking forward to have this kind of urban planning around here. I don’t think everybody has to live in a house with a lawn. But if you’re one of the higher earners, you should be able to afford it. However, many are not. You either inherited it, or you bought early enough, or you live far away and have a nightmare commute.

I think what my parents have is quite nice, though. They live in a village which is 8 km away from the center of a city with 200k inhabitants. The plot of land is 1400 m2 and it takes them 10 mins to reach the center with a car, there are rarely ever any traffic jams. I think this kind of setup with smaller cities, with high density centers and some single family houses sprinkled around the edge, for the upper middle class, is quite ok.

That’s true, I enjoy spending time in Zurich. However, where I live is just loud, I can’t open the window, I can’t use my balcony as it’s just dirty from the street and super loud. I am surrounded by some ugly-ass architecture with no sense of cohesion, every building looks different (even though most of them are modern). I only have identified a single path/loop where I can go for jogging/walks without having to go near cars or cross roads. And even then I hear the noise from the Autobahn. I could live in a flat, but then this flat would have to be in a calmer place, with a view to some park and not into the neighbors window. With these criteria, a flat in Zurich will cost upwards of 2 million CHF.

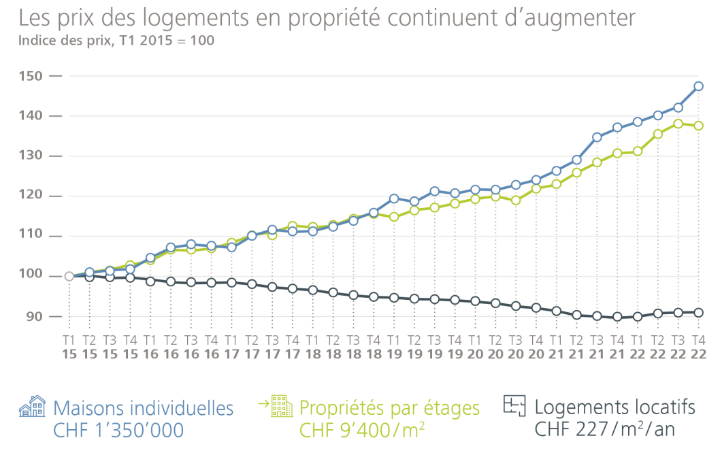

Personally I expect a period where rents will increase faster than house prices. Rents as a % of price will stabilize at a higher level than today

Demand for accommodation is increasing faster than supply however that does not necessarily mean that sale price will keep increasing. Prices are impacted by other factors - e.g. interest rates. There is an alternative option: renting

The cost of owning just increased due to interest rates. This will tend to push more people towards the rental market as explained perfectly by the example of @happy_bear:

So demand for rental is likely to increase. We also have salary inflation (CPI is running at 3.4%) which will feed through to rents and in addition the reference interest rate used to cap rents is also increasing.

I am not sure if what I’m going to say is actually true, but intuition tells me that rental prices are even more stiff than real estate prices. Maybe it’s partially due to rent controls, which are apparently in place. So if annual_yield = rent_price / real_estate_price, then if annual_yield should go up, it would be more likely due to falling real estate prices, than rising rents.

So let’s say a person with a taxable income of 100’000 CHF wants to buy the reference flat (not even a house!) for 2’000’000 CHF. How much money can they save per year with that kind of income? Pay your tax, cover your living costs, what are you left with? perhaps 40’000 CHF if you’re frugal. So you should be able to pay off that flat in just 50 years. Does it make actual sense?

Or to put it differently, if the value of your work is 100’000 CHF per year, that flat is worth 20 years of your work. It would take you 20 years of your work, not to own it, but just to produce an equal amount of value. This just sounds a bit off to me. You work and earn in one of the best paying places in the World, but most of that money goes into paying for that dream home? Probably better to take the money and go, in many cases.

Apparently rents were falling for the past ~10 years. Low interest rates created an incentive for institutional investors to construct rental buildings and increase supply:

Raiffeisen are now talking about a “time bomb” whereby rents are going to increase. Reference rate for rent controls is going up. UBS talk about a 20% increase in rents by 2025

The first increase should come with the next publication in June as we are close to the threshold, however 20% seems a lot given that the reference rate takes into account the past 10 years of mortgage rates and you still have a huge pile of mortgages below 2% in that timeframe. Also we cannot know how rates will evolve till 2025 unless you have a cristal ball ^^, rates might go down again…

Yes UBS forecast that rates would go up not down. The reference interest rate in 2025 calculated by them and on which they based their forecast was 2.5%.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.