Swiss investors can purchase real estate funds in their Pillar 3a.

For instance, Finpension lists “CSIF (CH) III Real Estate World ex CH - Pension Fund ZB”, which tracks the index FTSE EPRA/Nareit Dev (global exposure).

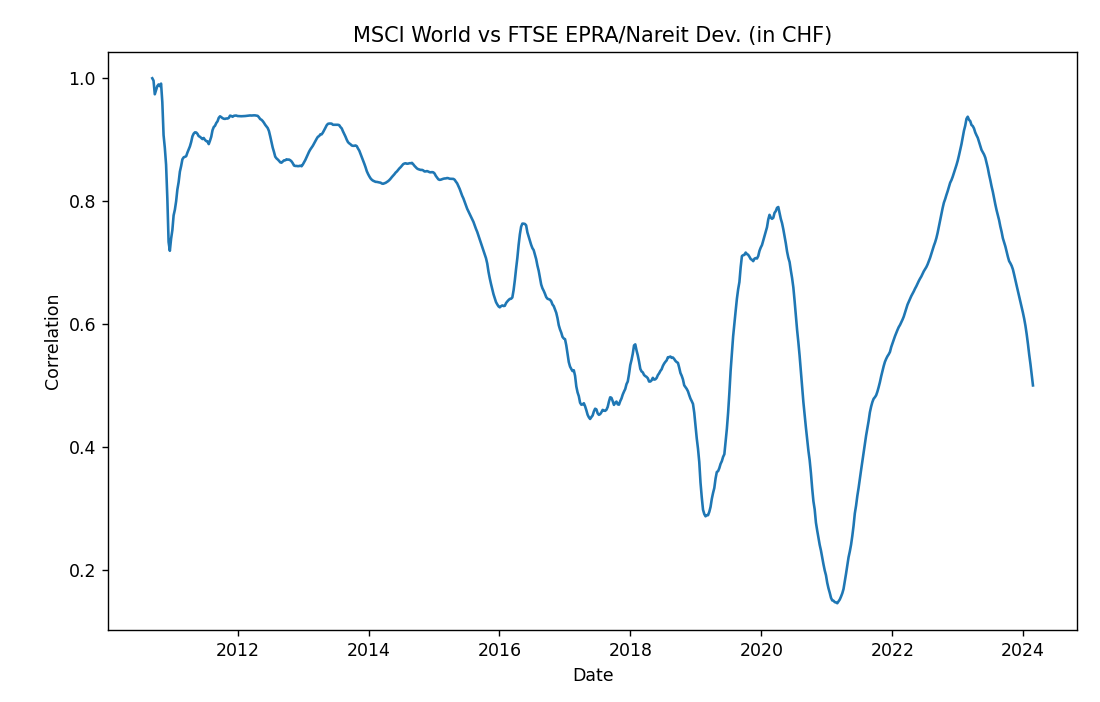

I have made a comparison with the popular MSCI World index (stocks) and we can seen that, with similar volatility and returns, we had the (36-month rolling) correlation below:

Don’t buy this kind of products as it is basically companies that are part of the stock market. Buying it would be like buying a supermarket ETF or energy ETF or any sector basically.

If you really want real estate, you can buy swiss real estate funds outside of your 3a. The law limit their leverage. Some of them are interesting from a tax point of view for swiss investors

And for the tax angle, is the idea to go for non-direct ownership so the income and wealth tax is assessed directly on the investor and benefit from a lower wealth tax base compared to actual market value?

Those funds all don’t hold the RE directly.

For me that’s a tax drag of about 1.7% compared to “direct”, so I decided to go for funds which hold the RE directly.

yes, started smallish positions in BALSP and HOSP recently, outside of 3rd pillar.

For diversification, since I have no other RE, as part of my non-equity bucket, get a little bit more return than Festgeld at some more risk.

I tried to look into Residential real estate funds few months back. What i found quite weird that they trade at a lot premium versus their NAV (which I don’t understand)and have higher TERs too (which I understand due to high cost of managing real estate)

The US is a very special case. There if you have a high earner paired with a spouse qualfying as a real estate professional, you can use bonus depreciation and other rules to dramatically reduce (or even eliminate) your tax burden.

Here things are very much canton specific, but in many there can be huge wealth tax benefits and also income tax benefits (esp. if you buy a doer-upper).

I won’t give specific names, but you should specifically look at the ones with tax advantages

It’s for the safer part of my portfolio and it is literrally unique in term of taxation. It is not as safe as bonds but you make money if you do your homework (normally)

Direct ownership (no wealth/income tax to you, reduced in-fund taxation compared to typical income tax)

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.