Well, people paying those high fees are paying my museum tickets, so I can’t really complain.

What do you mean exactly?

You have one eBill “account” for all banks.

Bad news:

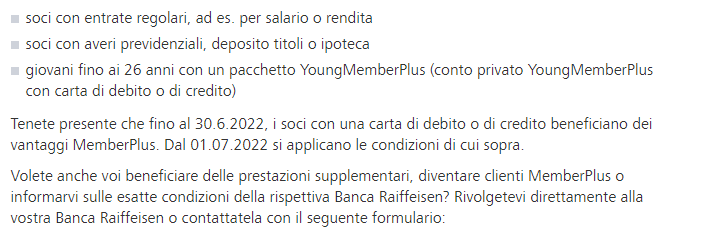

From 1.7 to be a MemberPlus rules change:

Either you have regularly money flowing in OR you need to have 3a, ETF ,mortgage etc. or be young ![]()

I suppose they will remove the rule that you need a Maestro/VPay whatever card, otherwise it’s just a big hassle.

This is a generaly information, vaild for ALL Raiffeisen

I might need to call them to understand. Maybe having more than 20k on 3a will save me from having the Mastercard card and money flowing in.

Edit:

Confusing: You can identify with the IBAN… I wonder how it works in a museum if I show them my IBAN

2 Likes

You have to cancel standing e-bill payment orders in one bank and recreate in another one.

2 Likes

I guess they just want to avoid people parking cash (I assume they’re fairly generous when it comes to applying negative interest rates?)

It depends on the branch of Raiffeisen. In mine, I can park 2 Mio without negative interest (quite an exception).

I didn’t find anything about parking money tbh.

They have storage boxes though. They might use that ![]()

In mine negative rates are applied from 350k!

I am sure that they will drop this 2 Mio limit anytime soon ![]()

1 Like

Negative rates from 350k or 2 Million. Man, we have too many millionaires in this forum ![]()

1 Like

On which page? I’m curious if we just skipped that. 350k is high btw.

Page ?

They told me this by phone.

1 Like

in case anyone else with a Raiffeisen account wants to check: My branch just snuck a 10chf annual fee for a customer card into the terms and conditions without any other communication - effective Jan 2023.

I cancelled my customer card as I already have a maestro

1 Like

I actually even cancelled my maestro card. Im sick of all these fees. ![]()

1 Like

We are in the process of moving our Raiffeisen accounts from Raiffeisen X to Y and open a security deposit for the rent to Y.

This is a nightmare since they need to move one of us first, then the second one after, then cancelled our joint account in X to open a new one in Y, because they can’t transfer it from X to Y.

Everything. Is. Fine.

PS: They will charge 10 more CHF for the Debit MasterCard (50 CHF instead of 40 CHF for the Maestro).

yes, Raiffeisen is getting really expensive lately…

I don’t really like the fact that Raiffeisen is centralized. Nowadays, people move often and their local entities don’t have so much power.

1 Like

Raiffeisen’s digital processes are really not up to scratch…

Some time ago we opened a joint account with the cantonal bank where we live. Previously, we used a joint account with Raiffeisen with eBill for the automatic payment of certain bills. During the process of transferring from Raiffeisen to our cantonal bank, we encountered problems because it was not possible to set up eBill with the new cantonal bank account.

Of course I called the customer service of the bank. They redirected me to eBill, which redirected me to Raiffeisen. For Raiffeisen, everything was in order. I contacted the cantonal bank again, and was met by a very competent lady who told me that “when creating an eBill account, Raiffeisen indicates a fictitious date of birth which can cause problems later on, especially when transferring to another bank”. A phone call to Raiffeisen, who maintained that there were no problems (?!) before I was transferred to the technical team who, indeed, found that the date of birth was wrong…

I’m very curious to see how the bank will develop with their famous 2025 strategy and the 500 million investment in digital… By dint of considering themselves as a “smart follower” while increasing fees left and right, I really wonder what the value of their service will be in the future…

What bothers me more and more is the emphasis on their “local roots” and the “privileged link with their members”, while reducing the benefits and remuneration of the accounts. The lack of consistency from one Raiffeisen bank to another (by which I mean the conditions granted from one bank to another) also leaves me perplexed…

2 Likes

To add something more about their catastrophic non digital process:

My girlfriend have to move on Raiffeisen Y to order the transfert of their account (checking and savings) from Raiffeisen X in order to open a Savings Security Rent Deposit with the same contract, otherwise it would have been a new one (why, I don’t know). During the process, they encountered a lot of problem to transfert their account because, they just use our IBAN Joint Account instead of their private ones…

What is strange for me is that, their E-Banking et mobile app are really great and their customer services too, when you have someone competent and patient.

But their onboarding and transfered process is a mess !

I hope that everything will be set up next week ![]()

Non standard stuff is always difficult for all banks. Maybe UBS and CS are OK for those stuff. I know someone who had a very bad and expensive problem with Cler, just because they have rules and some staff is sub-par.

For Raiffeisen, I think they have a very cool app for scanning invoices. You can install it on any phone without any connection to your account, once you have to scan invoices, you first pair it with your account via a web QR and then scan your invoices. At the end you check and pay through the web application on your pc. I’m a pc person so I prefer working on a computer rather than a phone.

Another annoying thing is that they are the only bank showing interests rates in fractions. Annoying.

Third and worse, it’s not clear yet if you are still MemberPlus if you don’t have a Debit card. They don’t know and I am not even sure of what I’ve read on the web myself.

Rising costs are kind of weird now, but I think they decided some time ago and might backtrack soon.

You are a MemberPlus but can’t use the benefits anymore since the card serves as proof when you go to a museum or other activity with benefits from MemberPlus.

For what it’s worth, I have an excellent experience with my local branch for everything regarding standard products, mainly because I personally know my advisor. They seem to have a very hard (if not impossible) time getting anything outside of the standard products with the standard fares, though, everything requiring discretional input seems to be centralized.

I did get a student loan through them, even though they stated they normally didn’t offer the product. The interest rate was 3.75% from 2013 to 2017 so, good for an unsecured loan. This was apparently possible because my father, with good credit, put his name on the loan too. They’ve been flexible on the repayment conditions so I have nothing to complain about.

All in all, I have a rather good experience, even though they’re not the cheapest (anymore).

1 Like