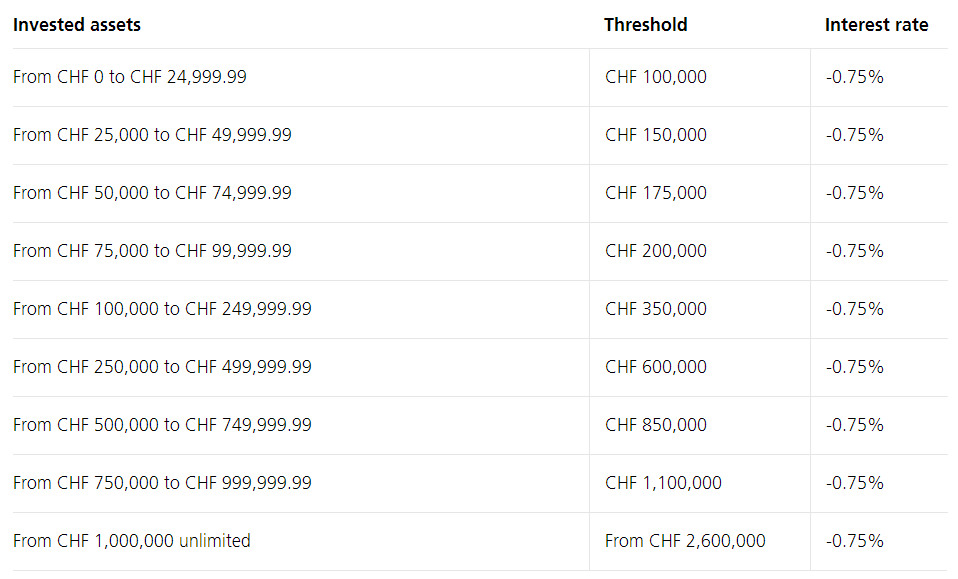

So, a bit confusing, but my understanding is: if the cash balance of your private+savings accounts ever exceeds 100’000 CHF, you will pay 0.75% interest rate on the amount above this threshold. “Invested assets” and “pension assets” are safe. If you have a mortgage, you can keep an extra 250’000 in cash. Once your invested assets are over 1’000’000 CHF, you will get some individual deal from PF.

I don’t get it, why does it have to be so complicated? Why can’t they just say that they only count private and savings accounts?

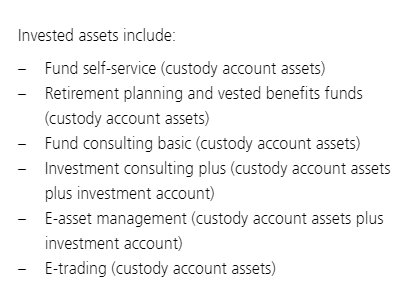

Looks like if you have signficant amount of cash and you want to store it at PF, you better transfer your shares there.

e-trading only costs 90 CHF per year (+fx cost?) while you’ll pay 90CHF of negative interests just by being 12k over the limit?

If other banks start tightening, might consider moving 100k worth of ETFs to PF for my next bank account. I guess the annoying thing will be dealing with dividends in USD (how much are wire fees if e.g. I’d like to send the USD to IB).

InteractiveBrokers lets you keep up to 100k CHF without negative interest rate. In case you are not ready to invest all your excess cash in one go and would rather average it out over a time period.

I would not be surprised if PF changes their conditions for trading in the near future. I would not tie my investments with them given their precarious condition. For instance, for a while they were including life insurance for higher threshold. But now it will no longer count towards that calculation. As long as PF cannot do mortgages (and interest rates remain low), you can expect worsening conditions. You have been warned.

I honestly don’t understand what the problem is. There are still saving accounts with a positive interest rate and not so strict withdrawal limits. In many banks you still get perks by keeping money in a savings account.

PostFinance is not allowed to directly give out mortgages like other banks as it is a state bank. In the current negative interest environment, it is facing strong headwinds because while other banks have been able to benefit from the real estate boom (via mortgages), PF has its hand tied. As such, it is in a difficult position.

As long as interest rates remain low and PF is not allowed to give out mortgages (directly), they have no choice but to keep cutting corners (and raising fees).

Not really. I mean, technically yes, but it only applies to certain amounts. Example: you have 250’000 in stocks, your threshold is 600’000, so you can theoretically hold up to 350’000 in cash. But if your stocks drop in value to 249’999, then your threshold drops to 350’000, so you suddenly can only hold 100’000 interest-free. The pricing is built so that you’re always sure that at least 100’000 is interest free. So it doesn’t really matter if you move all your stocks to PF.

I don’t get why they have to work with these ranges and thresholds… it’s the same with courtage for stock exchange transactions.

Die Valiant Bank ist seit 2011 Hypotheken -Partner der Postfinance

Yes, but the margins are not the same if they were allowed to directly compete against other banks. There has been some movement in allowing PF to enter the mortgage market, but obviously rest of the banks are against this.

It’s an interesting theory that PF has to increase fees, because it cannot make money on mortgages and it is losing money on sight deposits.

This might prove problematic in short term, but might also prepare the bank in case of inflation and rising interest rates. I know, you’ll tell me this won’t happen. Let’s see.

But I don’t think PF is an isolated case. It’s just in the forefront. Other banks will follow.

Why do you think cash is actively fought? Due to “crime”?

If there was only digital money, they could introduce 2% negative interest already from 0 CHF.

Can someone explain to me why do the banks have charge this negative interest? I bring my money to the bank, they book it to my account. What costs does it incur that they HAVE to charge me?

The idea of this calculator is nice. Work with numbers when then words are confusing. However, the calculator is too much simplified.

Our example:

Trading account is on my name (as not possible otherwise)

Current and saving accounts are joint accounts (legal reasons)

Result: We will have to pay the fee (with > CHF 100’000 in the joint accounts) although “we” have significant amounts of ETF in “my” trading account → To solve it, I will have to open a new saving account on my name and transfer a certain amount to it

PF makes it even hard for the customers they want to keep …

Surely a central bank specialist will give a detailed answer, but IIRC the rate on accounts has to match the central bank’s overnight rate. In this case it is exactly -0.75%:

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

.

.