I can agree to mixing CHF bonds into the allocation. I‘d mix in swiss government bonds however.

But here I definitely disagree. The bond part in 60/40 should be majority government bonds that are mostly safe and uncorrelated. As that is the purpose of the bond part.

You don‘t want your bonds to be down a lot as well during a recession, then when you want to rebalance from your bonds into the depressed stocks.

Some small-moderate amount of investment grade corp bonds is ok. Like the classic BND from the bogleheads is about 70% government and 30% corporate.

The recommendation for global aggreate comes from trying to keep it simple for folks like OP‘s parents. Even 3 funds is already a lot.

VT + global aggregate is probably enough and even simpler.

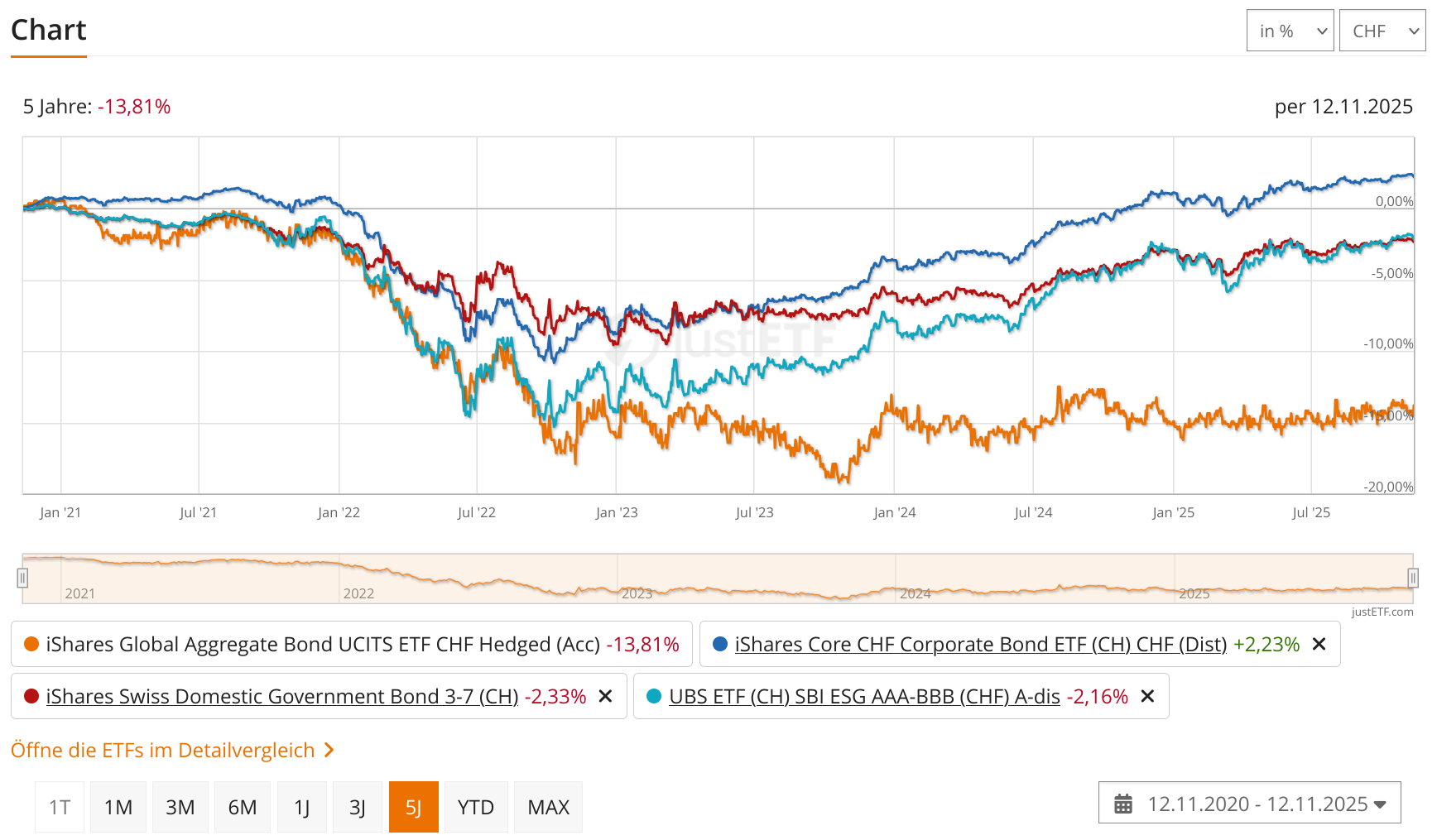

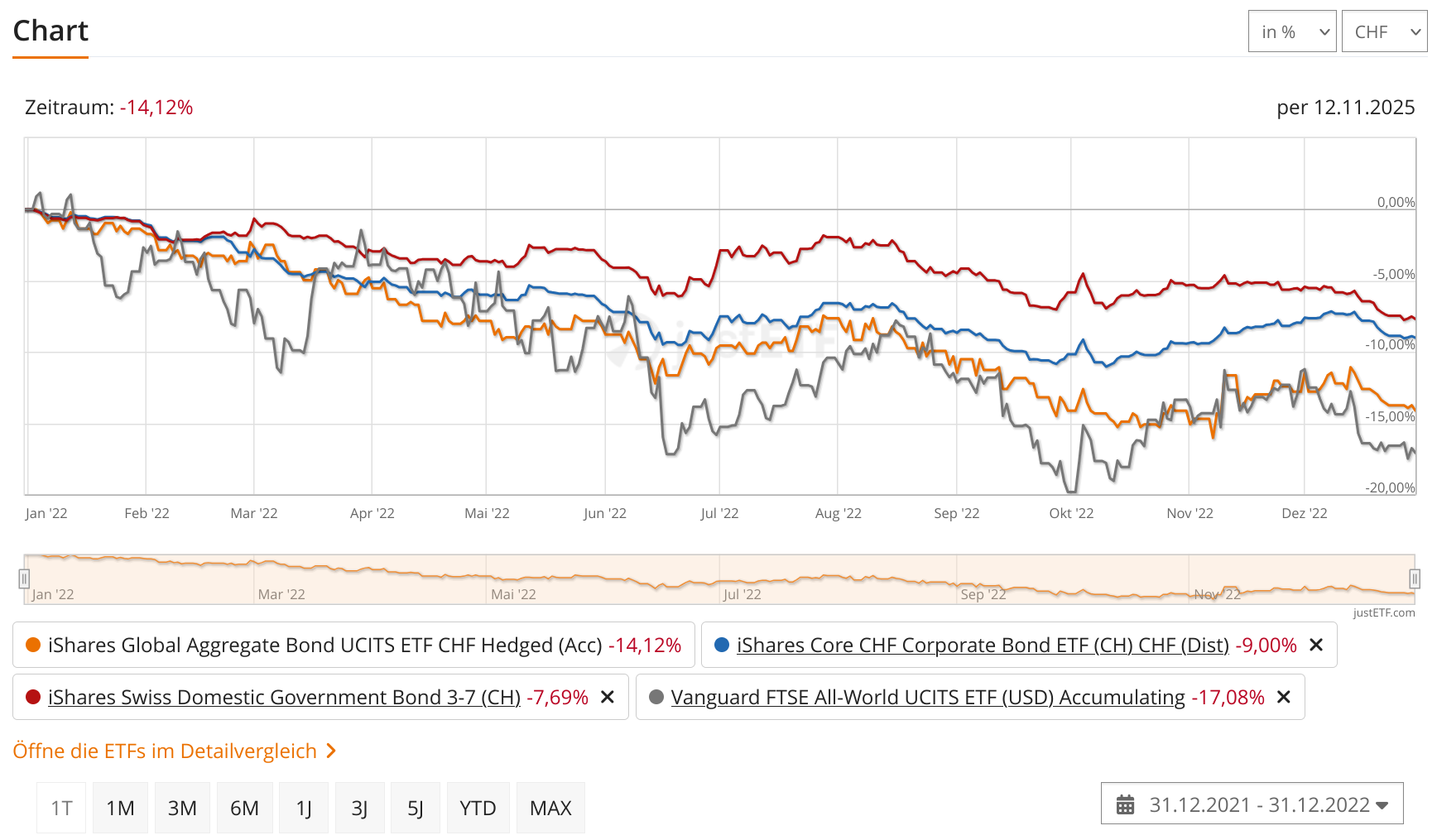

Sure performance hasn‘t been great recently. But that was mainly due to yield curve developments. Swiss cut rates a lot faster than other governments and we are already back to zero rates. That‘s why swiss bonds recovered already, while other governments are still at higher rates (and may stay there). While swiss rates may not have much room to fall anymore.

However that is also short term thinking and shouldn‘t be a determining factor.

But handling a handful of bond funds or more alternatives is really not it in my opinion for someone like OP‘s parents. If they want that, they‘d need a robo advisor or go to VZ etc.

Tops I would add the ishares 3-7 swiss government bond fund at 10-20% maybe.

Keep it as simple as possible and only as complex as necessary.

Ideally Vanguard does a swiss version of their € Lifestrategy funds for us swiss investors. That would make these topics so easy. Just put everything in their 60/40 CHF and forget about it…

Thinking about it, their € version is so good, it wouldn‘t even be a terrible solution for a swiss investor. € is likely to stay quite correlated to CHF I would think. Sometimes simplicity (and prevention of mistakes) beats a more optimal solution.

Closest we have to that are the Avadis solutions like their 60/40 https://avadis.ch/assets/files/private/de/factsheets/strategie_wachstum_ava_sicav_de.pdf

Which is good and the allocations are solid as well. The TER is quite high at 0.54% though.