I’m new to the forum - but I’ve been reading along quite a while now

I just opened my IB Account (and made a first buy for VT ) - I’m currently thinking about my Portfolio Strategy - and I’m looking for some Feedback.

Background:

33 Years old

stable Income + Savings

No plans to retire early

→ Ambitious Plan: starting ~50 don’t work fulltime + jobs that I enjoy and pay the bills

Assets:

Emergency Fund (~20k)

2nd Pillar

3rd Pillar (VIAC 97 / Frankly 95) (~22k)

3rd Pillar Live Insurance (~18k might get closed and moved to VIAC / Frankly)

German “Bausparvertrag” (~30k) - will get closed and invested

(Euro ETF - 1 time buy and hold) → Ideas?

Investments:

BuyIn: 10k

Yearly: 12k (1k per Month)

Current Portfolio Idea:

55% VT

30% SmallCaps - 50% AVUV / 50% AVDV (thx @xorfish )

15% Gold (?) / Silver (WPM) - Main Reason: to lower volatility

The Plan is to hold the stocks LONG and spend the least amount possible on investing.

Is AVUV / AVDV a good idea for this? And is the allocation of 50/50 reasonable?

Also thought about EM - but VT already has 11.4% EM included …

Might would buy some hand picked stocks (Swiss based) - but no plans for that currently, I would also buy them with additional money beside the regular investments.

Bond/cash would lower volatility, I don’t think gold/silver significantly does. If you want to hold it maybe find another reason (it’s still a fairly large allocation for non productive assets).

The small cap tilt is pretty big, that’s a large bet on FAMA being correct Maybe check some analyzers with monte carlo over 20 years and see how much difference it actually makes (and decide if it’s worth adding complexity for that).

In one of the Financial Podcasts that I’m listing to - I think it was the one from “FinanzFabio” (Swiss-based Financial Advisor) there was a Fund Manager which was explaining that holding 15-20% Gold (and maybe Silver) in your Portfolio would lower the volatility, because when stocks fall - Gold rises …

It sounded quite logical to me - but maybe I’m completely wrong … IMO Bonds currently don’t make sense, because they have negative returns for quite a while now.

–

What would you say would be a better allocation? 15% / 20%?

Does it even make sense to buy AVUV and AVDV? Or should I decide for only one or change the allocation between them?

I can live with a higher allocation into VT easily (makes it more easy) - but thought that adding 1-2 other investments would make sense.

Yes, there’s a theory that it should be inversely correlated. But no idea if it will hold true long term (central banks have sold a lot of gold, that might continue), also there’s period where both equity and gold move in the same direction.

Can i please ask something and try not to make too much fun of me i dont get this lowering the volatility by being simultaneously long term invested in 2 items that go opposite.

So lets say you have 1000 CHF in VT and goes down 10 percent during the year

The same time you have 1000CHF in gold and it goes up 10 during that year

if you are not realising your profits lets say you sell gold when its 10% up and just hold it and gold goes down the next year how does that make any difference in the long term i dont get it.

yes sorry i did explain myself correctly as in what is the point of that? how does the volatility affect the normal private investor here

Unless you can time the market and sell the VT just before dip and by the gold before it goes up and then sell the gold before it goes down buy back the VT i dont see how is this is usefull.

or if it is i would really like to know why so i can potentially use it too.

There’s two things, volatility and uncorrelated asset class.

In general lower volatility is preferable (steady increase is always better), and we’d seek to be rewarded for the higher risk implied by the higher vol.

For the uncorrelated asset classes, the key point is that you define an allocation and then you stick to it. If it’s truly uncorrelated, you’d rebalance when one over/under performs (so sell high, buy low). It increases returns, I don’t think it changes volatility.

oh ok wait so you are saying your portfolio lets say is 70% in VT and 30% in gold and when the VT goes down and gold goes up then you keep selling from the 30% of gold and buy the dip of VT and then when VT is up and gold down you keep buying gold till your allocation goes back to 30% of your portfolio?

It‘s big, yes. On the other hand, in the grand scheme of things it will likely still be highly correlated to blue chips or VT.

The overperformance of MSCI World Small Cap over „vanilla“ MSCI World must have been less than 1% (annualised) over the last 10 years. Does this have a significant impact on your portfolio, and how big is it.

To put it in layman’s terms: What if you had 10% Small Cap (or any other „tilt“) in your portfolio and that 10% share grows one percent more each year than the rest of your portfolio?

Well, it would amount to 10% * 1%= 0.1% difference for your overall portfolio - or roughly 1% over 10 years. So would it make a great difference towards your overall investment goals? I don’t think so.

If you want to deviate from low-cost VT by investing in other relatively strongly correlated assets (other diversified stock index funds) wouldn’t you want to do it with a share of portfolio that’s big enough to - hopefully - make a significant difference?

@San_Francisco

Thanks for the time you took to write all this!

I think you are right - I’m overcomplicating things … with the small Portfolio I’m starting it doesn’t make a big difference.

I think I will start with VT as my main ETF - this should bring a certain base performance at a really low cost. I can still add some tilts later …

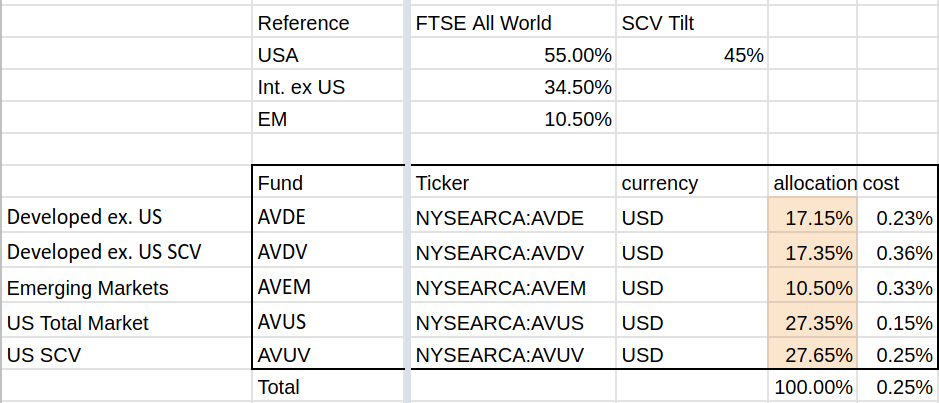

Here is my allocation for taxable. I have a higher factor tilt in taxable because I can’t have a factor tilt in 3a, overall tilt is 35% in small cap value.

I don’t think there is enough evidence to support that gold is negatively correlated with stocks. It is also far too volatile if you want to reduce overall volatility. I would just stick to cash for that part until bond yield raise.

VT + AVUV + AVDV is fine, but be aware that you underweight emerging markets if you go that way.

Thank you for sharing your allocations. I’m in the process of implementing a similarly aggressive factor tilt in my portfolio.

Isn’t your factor tilt higher than 45% because AVDE and AVUS are also factor tilted? Is it negligible, or do you have any info about the overlap?

Did you consider the withholding tax implications when constructing your portfolio?

Yes, that is true, althoug the tilt in the core funds is quite small. There is probably some overlap as companies in the scv funds will likely also be in the core funds, but with a much smaller allocation.

Yes, as long as my marginal tax rate is above 15% and I don’t pay interest, then this should also be very tax efficient.

If yes, why more risk? Because more exposure to Value stocks and Mid cap. Or maybe the factors like volatility? Uff, I still need to understand the factors…

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

,

,

) - I’m currently thinking about my Portfolio Strategy - and I’m looking for some Feedback.

) - I’m currently thinking about my Portfolio Strategy - and I’m looking for some Feedback.