First, thank you so much for all the great information in this forum, I have be devouring so many great threads and discussion - thank you!

I opened an IB account and put together a portfolio, I have it below. I have two question I would really appreciate some help on:

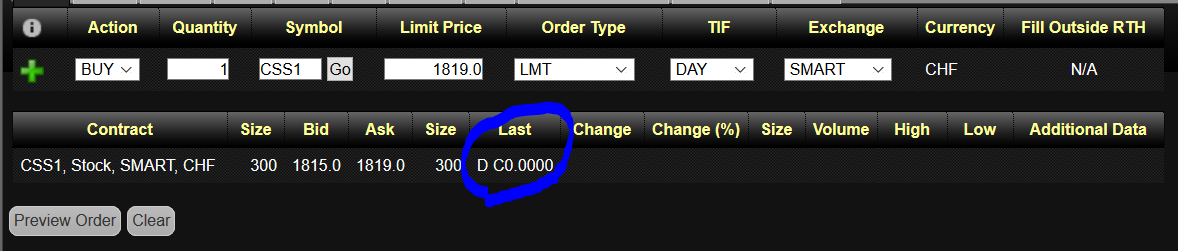

The CSIF (CH) Equity Switzerland Small & Mid Cap FA looks like it has very low trading volume and when I try to buy it on IB - it says it’s price is zero. Does anyone know why this is? I found the stock in one of the Mustachian ETFs forum threads and I want to invest a little into Switzerland but stay away from large cap as I get plenty of stock from the corporate I work at.

CSS1 (ISIN: CH0222624659) has a zero closing price?!

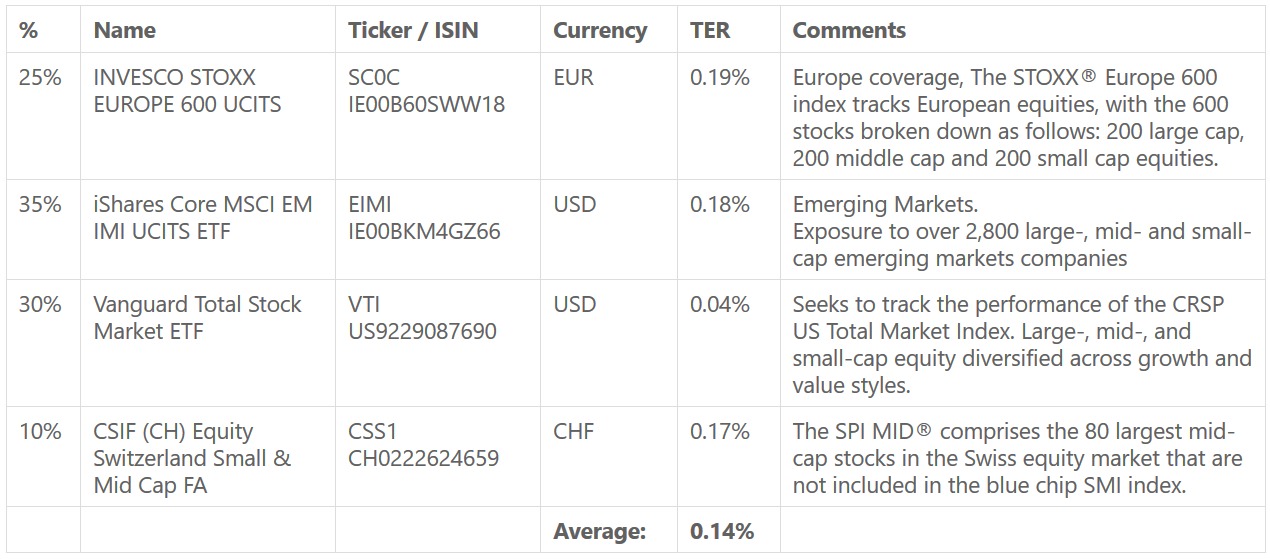

Does this portfolio make sense? I go with a lot of stocks as I am still very young, and I already get stock in the big swiss corporate I work for - so I tried to get a well diversified portfolio with more weighting in EM as I have a high risk tolerance (and plan to invest for ~40 years minimum).

And you say next yourself you’re already a little invested in Switzerland. More than a little if you’d consider your CHF paying corporate job and benefits

EM does not unquestionably mean more risk more gain. Did you even look at the shit you’re going to buy? Banks, banks, lots of f’ing chinese banks, and just a few giant asian IT tech companies that turn top 10 into top 25%. Is that your idea of something that’d emerge you more wealth than S&P500? Pass

Thank a lot hedgehog! Really appreciate your feedback.

That makes sense, I was unsure if I was doing something wrong in IB or so, but probably just a not so popular ETF. Thanks!

Good point, also my pension savings are all in Switzerland so better to diversify.

This is really helpful, I had looked at the top 25 but as I have limited experience on what is a “good ETF” then I thought it looked fine (i.e. geographical spread and EM companies).

I was thinking that with the Vanguard Total Stock Market and STOXX 600 I am rather well covered for the S&P500 (correct me if I am wrong here though, I just thought that the companies in S&P500 are included in those two ETFs).

Do you have any advice how I can invest into EM in my portfolio? I felt it is important to have that aspect in my portfolio as I am living in a developed market and more than 50% of my portfolio is invested in the developed markets, that it could be good to have some EM exposure.

Really appreciate your helping out a beginner, thank you!!

Well then what would you recommend to invest the money I hold in CT into? Currently I have VUSA, but since I have IB, it doesn’t make sense to keep it. I also don’t want to close my CT account.

I thought about buying VFEM. If you look at the factsheet of FTSE Emerging, banks make up 18% of it, technology 16%, the rest is spread over many sectors. Emerging markets still have young societies, still profit from the “demographic dividend” (more people in production age than in school/retirement). Europe is full in debt, they try to cope with low fertility by importing people from Africa, not sure how is this gonna work.

Of course, the condition of the economies is not directly linked to how their stock market will perform, because the companies operate worldwide. But still, there will be correlation.

So, back to the question, what would you replace the VUSA with, considering I have VT at IB?

I mentioned small caps already. that’s a more stereotypical example of higher risk higher potential returns

Do top holdings look to you like they have much to do with this demographic dividend? India is only 8%! South Korea and Taiwan are emerging? Not in my book. Chinese banks have a debt problem bigger than Europe’s

Well, isn’t that a good thing that India is small? It can grow in the next years. South Korea is not part of EM in FTSE indexes. Didn’t know about Chinese banks. But I would say that Chinese companies should have a huge opportunity ahead of them. They have a potentially even larger home market than USA, which can act as an incubator. They are not so much concerned about ecology, human rights, patent law. And what if China’s military gets big enough, so that Americans can’t dictate the terms? Putting 50% of the portfolio in USA and only 3.5% in China seems like a considerable imbalance to me.

Why not overweight BRICs then? I started a separate topic on this, but not much interest.

Russia may be the questionable component here, but … well, it’s Russia. Business will go on even if the people are starving.

Yeah, that’s what I call “incubator”. They can develop in perfect conditions, and when their products are good enough, the World will buy them. Wasn’t it the same with Japan and South Korea? First you start with mercantile/protectionist policy and let your own companies satisfy the home market demand. At first, their products have shit quality, but with time they get better. And when you’re ready, you lift the barriers and join “free market”. What Poland did in 1990 was opening the market too soon, which killed many local companies, which weren’t ready for it.

The people governing China are technocrats, they are no dummies, and they can focus on the important stuff, not worry about reelection etc. They invest heavily in things like solar power. They tackle problems with unimaginable momentum: like they had a problem with desert taking more and more land, so they decided to plant millions of trees along thousands of kilometers. Also, historically, a few hundred years China was already responsible for 30% of the World’s GDP. I have a fear that the Chinese might leave many other developed countries in the dust.

Of course, history is so unpredictable, so many things can go wrong, that I’m not gonna bet a lot based on that prediction. It’s just what I’ve been able to read and watch recently.

Really interesting discussion, it is clear there is no silver bullet here!

There is definitely some risk with wherever you place your money, otherwise the market would most likely have corrected for it.

I had a look at VFEM that @Bojack suggested, this looks interesting, I couldn’t find the TER in the fact sheet though. I found the Vanguard one, VWO and that has only a TER of 0.14%, that could be a great FTSE Emerging market ETF to invest in, what do you think?

Does @hedgehog have any suggestions for ETFs that cover the small caps of EM? I had a look around but this seems like a hard area to cover through an ETF…

How did you look? Type in “vanguard vfem factsheet” in google and it’s the first result. The OCF (TER) is 0.25%.

Of course VWO has a lower TER, but as I’ve said, I have some CHF on Corner Trader, and so I’d like to buy an ETF that trades in CHF. I’m looking for an ETF that would compliment VT. So the question is what should I overweigh. Ideally, I would invest in something like VXUS for Europe, but Vanguard does not offer it in Europe (weird, btw).

Interesting. I was comparing some SPI Extra funds out of curiosity when I stumbled on this CS fund. I was comparing it to the Swisscanto SPI EXTRA fund (CH0315622966). What I don’t understand is that even tough both are non-exchange traded index funds, they are not traded in the same way. When I search them in my eBanking i find the following:

CH0315622966

Anteile -FA CHF- Swisscanto (CH) Index Fund V - Swisscanto (CH) Index Equity Fund Small & Mid Caps Switzerland Stock Exchange: PRIMAERMARKTT2

CH0222624659

Anteile -FB- Credit Suisse Index Fund (CH) Umbrella - CSIF (CH) Equity Switzerland Small & Mid Cap Stock Exchange: SWX

What is the conceptual difference between those funds? So why is the CS fund traded on SWX and available on IB even though it’s a non-exchange traded fund (and not an ETF)?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.