Got it. As I said I used LLM earlier in this thread to summarize Dom Development. I took discussion from portalanaliz.pl forum between me and other investors about the company. I asked LLM to translate it to English and summarize the information. I checked the data for accuracy and added my own opinion about current situation. It accelerated the process 4-5 times comparing if I did it manually.

2 Likes

Indeed. The tax advisor stated that no tax should be levied on capital gains if I am a tax resident in Switzerland. I should reject the tax return automatically prepared by the Polish Tax Office.

On dividends, according to the double taxation avoidance agreement, the broker should withhold 15% tax.

3 Likes

I wanted to start discussion about Synektik (Ticker SNT.WSE).

It is a Polish medical technology company with business model spanning radiopharmaceutical production, medical equipment distribution, and healthcare IT solutions. The Synektik Group is exclusive distributor of Intuitive Surgical’s da Vinci robotic surgery systems** and is the largest manufacturer and supplier of radiopharmaceuticals in Poland, a developer of specialized medical software (e.g. PACS imaging systems, the Zbadani.pl platform), and a leading distributor of advanced medical technologies with associated maintenance services. Geographically, Synektik’s core operations are in Poland, but the company is expanding regionally for example, its exclusive distribution agreement for Intuitive Surgical’s da Vinci robotic surgery systems now covers the Baltic states through 2029. Synektik’s equipment portfolio includes cutting-edge diagnostic imaging and surgical systems (e.g. da Vinci surgical robots, Hologic mammography devices), which it supplies to hospitals and clinics, alongside long-term service contracts and consumable instrument sales.

Synektik operates two main segments:

1. Medical Equipment & IT Solutions, which integrates the sale of Intuitive Surgical medical hardware, maintenance and training in Poland, Czech Republic, Slovakia, Lithuania, Latvia and Estonia.

2. Radiopharmaceuticals, involving production and delivery of radioisotope tracers for diagnostic imaging (notably PET tracers).

Synektik’s outlook and investement thesis is influenced by multiple growth drivers across its business lines:

- Surging Medical Capital Expenditure & Funding Tailwinds: Poland is increasing hospitals investments thanks to EU-funded programs like the National Recovery Plan (KPO). Hundreds of millions of EUR are allocated to upgrade oncology and cardiology infrastructure by 2026, which directly benefits Synektik as a key supplier.

- Recurring Revenue & Service Model: Synektik is shifted its mix toward recurring revenue streams, providing a foundation for sustainable growth. Maintenance contracts, software licenses, and consumables increase its revenue contribution by 60-70% yearly. The installed base of da Vinci surgical robots is driving a flywheel of recurring income. Each new robot sale yields long-term revenues from disposable surgical instruments and service fees. In Q1 FY2024 alone, 9 new da Vinci systems were installed (8 in Poland, 1 in Slovakia). Synektik’s da Vinci installed system is reached 96 (65 in Poland, 31 in Czech/Slovakia) by end of 2024.

- Innovative Product Development – Cardiomarker : A key mid-term growth catalyst is Synektik’s proprietary cardiological PET tracer (often dubbed the “cardiomarker” or Cardiotracer). This novel radiopharmaceutical for myocardial perfusion imaging addresses the large cardiac diagnostics market. The cardiotracer is entering Phase III clinical trials – multicenter studies are ongoing in Europe, and Synektik has completed preparations (including an FDA pre-IND consultation) to launch a Phase III trial in the United States. Technology transfer is in progress, with production modules delivered and installed to supply the trials. The cardiotracer’s competitive advantages include higher image resolution and contrast, lower radiation dose, absolute quantification of blood flow, and the ability to image “difficult” patients (e.g. obese) with shorter radiation retention.

- Expanded Portfolio and Geographic Reach: Synektik continues to broaden its product and regional footprint, opening new growth avenues. In late 2023, it became the exclusive distributor in Poland for Hologic’s state-of-the-art mammography and biopsy devices

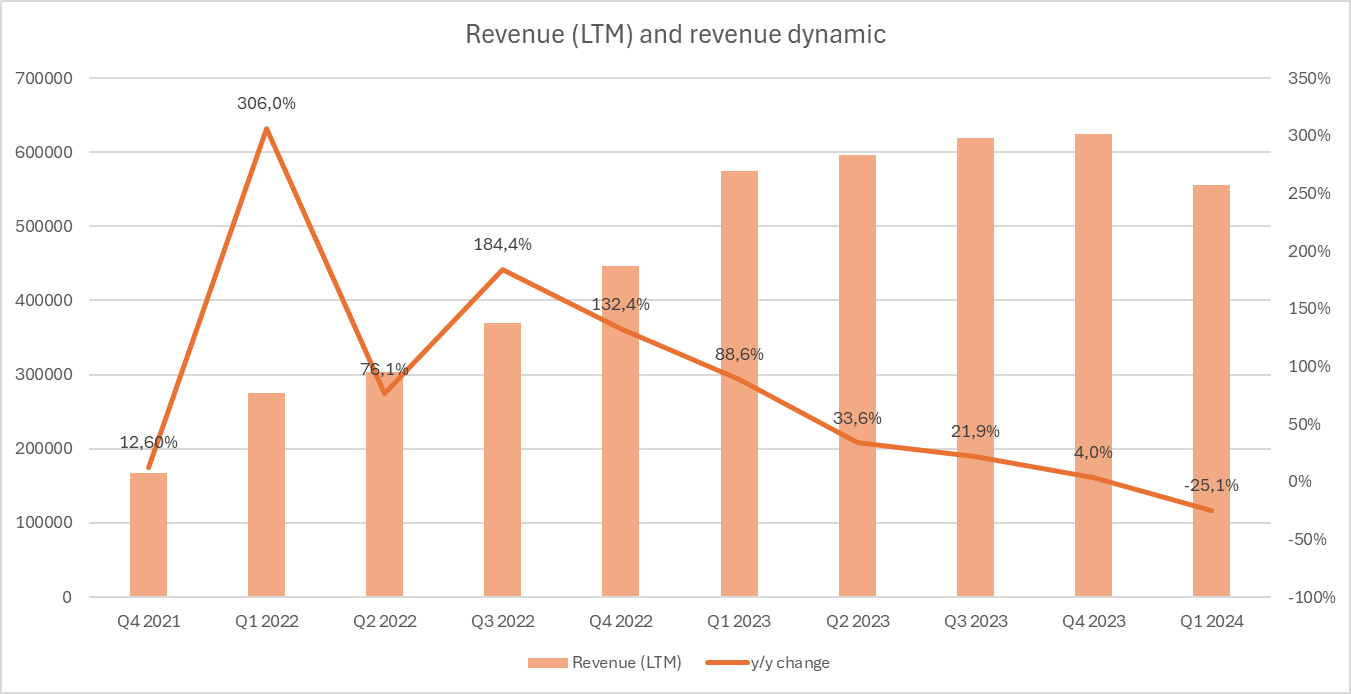

(Of note: Synektik’s financial year is moved by 9 months in relation to calendar year. For example: Q1 FY2024 is Q4 CY2024). Recent financial results (Q1 FY2024, quarter ended Dec 31, 2024) highlight a decline in total Revenue, due to lower than last year deliveries of da Vinci systems. However, it is worth mentioning that Q1 2023 was exceptional for the equipment business.

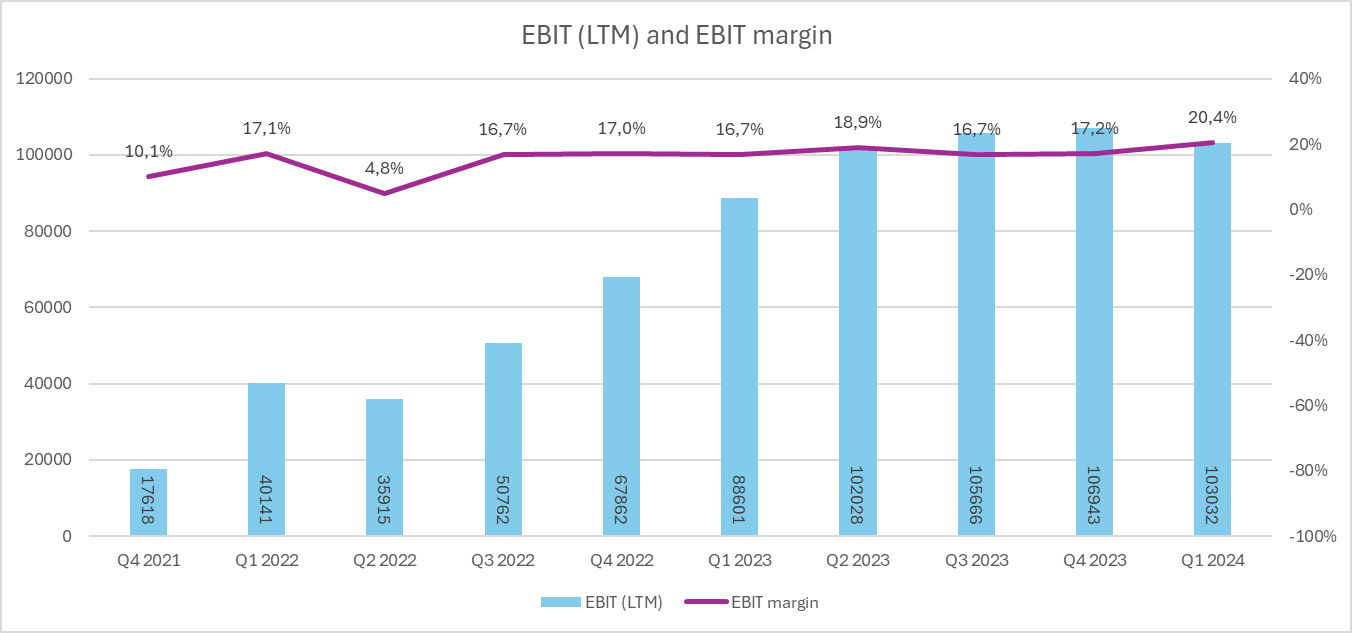

All numbers in thousands PLN.

Recent quarter might look like disappointment but it is mainly due to exceptional Q1 2023.

The company is not chip, but has outstanding ROE and ROIC. Current multipliers are:

EV/EBITDA: 14.7

P/E: 24

ROE: 36.3%

ROIC: 36.3%

Company has PLN -166M of net debt.

Let me know what you think.

For those who had a view on Polish stocks before the election- has your view changed now due to the outcome of that election?

For me the fundamentals have not changed. I am using current drop as opportunity to buy business which I believe are undervalued and have growth potential.

Some notes from the Synektik’s call with investors which I joined last week:

https://x.com/PolePosInvest/status/1932870333201072311

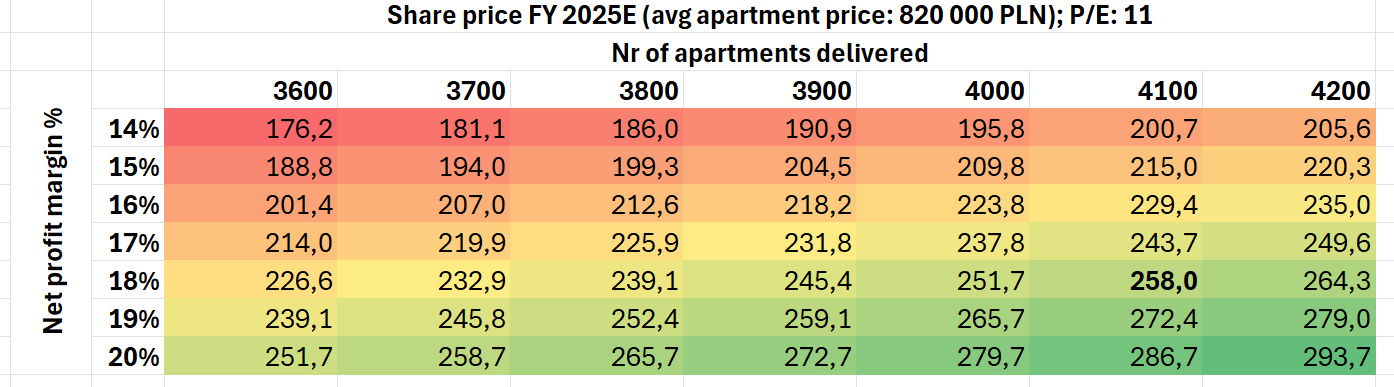

I checked if DOM Development is worthy my money. At current price (236PLN), not really

Below sensitivity table.

My estimate is they will deliver ~4100 apartments in 2025 (they did 984 in Q1) with net margin of 18% and overage apartment price 820’000PLN. It implies 234.6PLN share price at P/E: 10 or 258 at P/E: 11

In both cases there is very little upside.

For more information on polish stock follow me on “X - PolePosInvest”

Free Analysis of Text S.A. (aka Livechat are available here: Polish Investment Guide - Expert Analysis for Foreign Investors

New blog posts available on my website covering Sygnity (owned by Constellation Software), Comp (IT Security for defense and gov sectors), and Passus (IT Security and AWS migrations). polepositioninvesting.com

If you want to stay up to date with curated news and sentiment analysis on these companies (and several others), check out the /news section on the site.