Hello everybody! I am going to repeat after many newcomers here: it was great to find this forum, I wished I found it 10 years ago. I am pleased to see people thinking rationally about their finances, and in particular people living in Switzerland and exposed to the particularities of this country. Looking forward for interesting conversations and hope to contribute myself.

About myself: I am not so young, have a wife and children, we bought an apartment (not too big, not too expensive) we are living in with a mortgage (more or less equal to our second and third pillars combined, not too high interest). Professionally I stayed all my life in an academic environment, my wife’s job is also not related to profit-generating. With our background we are very good at not wasting money, but not so good in investing it. It does not look an earlier retirement is in the cards for us, but I would like to increase our financial potential.

My financial knowledge is mostly coming from many years of reading cash.ch, which is Swiss- and active trading-biased. But I did learn a lot. Googling for explanations of financial concepts, I often ended up at investopedia.com. I am become somewhat more familiar with index fund investments reading this blog: https://www.etf.com/contributors/allan-roth , which did help me to understand few things better. The last two resources are very US-biased, so I could not find answers on my questions concerning investments specifically in Switzerland. Reading this forum and related blogs helped me to find answers to many questions and to grasp few things I did not even think before.

Here I would summarize these things that I figured out for myself reading this forum:

-

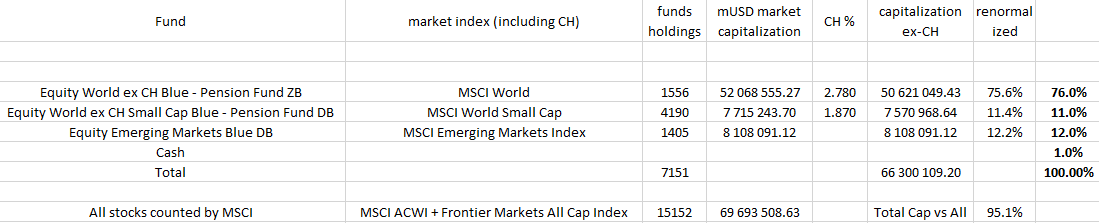

For a person living in Switzerland, 2nd pillar and (not invested) 3rd pillar money may be counted in some way as secure assets, so, bonds. Before figuring it out, I kept scratching my head thinking about what kind of bond allocation I need and if I should buy bond funds with negative YTM. Now it is clear to me that comparing how much money I can invest in stocks and how much money I (we) have in 2nd pillar and 3a cash, I can go 100% stocks for long time before reaching any reasonable stocks/bonds ratio. So now I have to sell all bonds that I accumulated and use these money to buy stocks.

-

No currency hedging. Currency hedging does not prevent long-term changes of rates between currency pairs, it just smoothens out short-term fluctuations and incurs additional costs. In fact I compared performance of few index fund classes, which have exactly the same composition but with and without currency hedging to CHF. After few years unhedged classes performed better than hedged classes, even shortly after Frankenschock of 2015!

-

The trading currency of a fund is not relevant. The “true value” of fund’s share did not change if you recalculate it into other currency. But what important are currency exchange fees if you are buying not in your base currency.

-

More dividends or less dividends is not important. If a company generates a profit, they can distribute it as dividends, use it to buy back shares or do something else. It does not matter as long as its value grows. Dividends are even disadvantageous because they are taxed more expensively as income as compared to the capital growth.

-

(A conclusion drawn also from pandemic news) Human brain cannot handle exponential increase