Hello fellow mustachians.

I’m currently helping my parents set up their withdrawal strategy for their retirement, and would really appreciate your feedback. They have already received a “pension planning” of a (in my view) highly questionable “Financial Advisor” – and frankly, it is complete garbage, which is why I think we are better off thinking this through ourselves.

Their situation:

Assets:

Cash & equivalents: 184k

Bonds & equivalents: 1.1 m Pillar Lump sum from Mr. Retired Frog to be paid out soon

Investments: 3.1 m (currently invested in 85% stocks, 7% bonds and some mixed stuff)

Other: 66k

Real estate: 3.2m (primary residence + 1 commercial property which is currently rented out, but long-term tenancy is uncertain)

-> Financial assets excl. RE: ~4.5 m

Income & spending:

Combined pension (AHV): ~34k/year

Rental income: 13k/year

Expected spending: ~120k / year (generously estimated, but they would like to enjoy themselves and travel etc., later on they might be facing higher medical expenses etc. )

Taxes during retirement: estimated at ~30-40k /year

-> Total expenses during retirement ~150-160k/year

-> Total draw down from portfolio needed: ~ 110k/year

Drawdown will likely start in ~3 years (for the next three years, they will receive additional insurance payouts which will cover their expenditures).

Special considerations:

- They are currently 65 (my dad) and 69 (my mom) years old, and luckily both are in good health

- The set-up needs to be simple for them to use (easy withdrawal / rebalancing process), they value simplicity more than a set-up which is perfectly optimized for lowest possible fees

- My dad has some experience investing in ETFs and with Roboadvisors. They prefer Swiss-based broker solutions, and would probably be overwhelmed with the IBKR interface

- They are not comfortable going all-in on equities overall

Current thinking (2-pot approach):

Their current thinking is to set up a 2-pot strategy.

Pot 1: “Pension pot” on TrueWealth (they like the interface and are both familiar with it), where they would manage the outflows and re-invest any surpluses. Starting balance could be the 1.1 million to be invested from the 2 pillar pay-out.

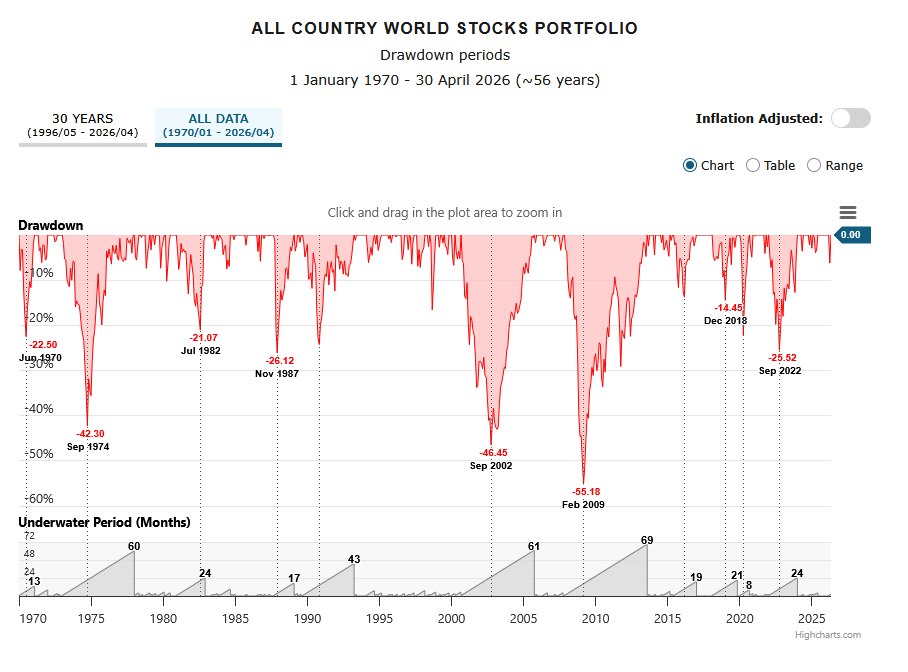

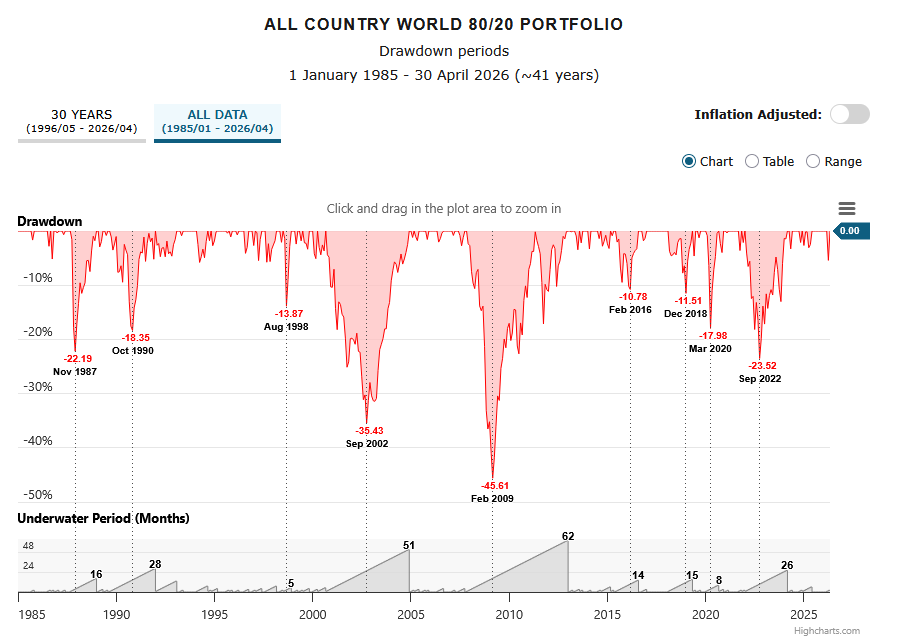

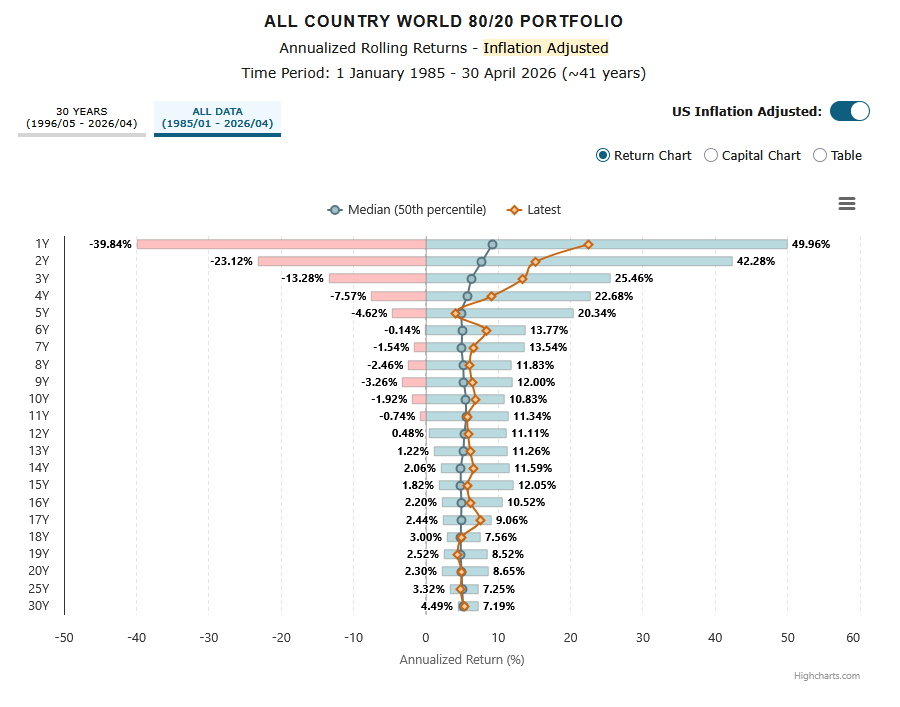

The thinking there is to go with a 80% stocks, 20% bonds allocation. This pot would have less volatility and more downside protection thanks to the bonds allocation to avoid that they panic if markets are down).

Pot 2: Growth pot, sitting separate, in a different broker (for diversification reasons – we were thinking about Saxo). The idea is that they would not touch this until the pension pot is drawn down. Starting balance would be 3 million.

Real Estate for now is left out of the picture for now, as this adds another layer of complexity.

Questions:

-

What do you think of the 2-pot strategy with 2 separate brokers?

-

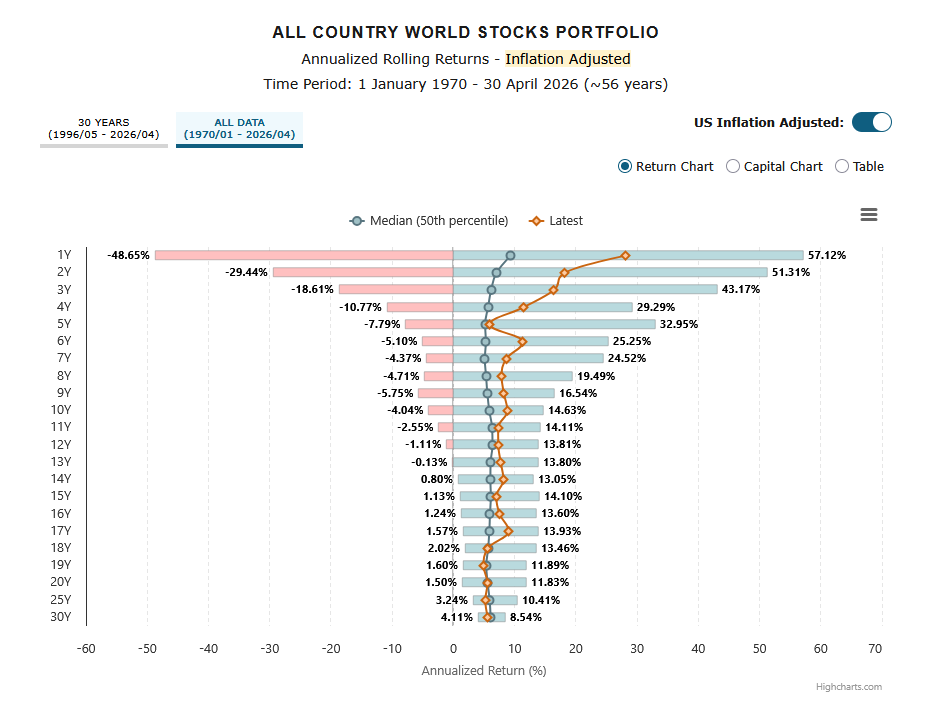

What do you think of the asset allocation for the first pot (Pension pot, 80% stocks, 20% bonds: and the second pot (100% stocks)?

-

In terms of the instruments, if they go for True Wealth for the Pension pot, Instrument choice would be limited. For the bond part, True Wealth offers the iShares $ Treasury Bond 20+yr UCITS ETF (CHF hedged), as well as a USD High Yield Corproate Bond ETF. How would you rate these instruments? What would you recommend if there was unlimited choice?

-

Do you have a recommendation for a tool that let me model the cash outflows granularly, stress test outcomes under different assumptions (to model the impact of Sequence of Return risk)? I am aware of this one, but it is heavily geared towards the US: https://saferetirementspending.com/

Thanks so much in advance!

Frog