Thanks, do you think I still have time to do these? my policy started with them on 1st Nov 2016, so I guess the premium for this year is due 1st Nov, the sales person told me that I have till month end to pay the invoice, and failing so the contract will be ended… so it’s another lie here?

I talked to them both. AXA, and the broker who sold me the insurance. AXA contacted the broker after my claim, and took almost 1,5 month to end up the whole process.

1 Like

If you have that statement officially in writing or as part of the contract (read your contract!) then it’s fine and should prevail in a dispute. Otherwise you should explicitly cancel, most contracts in switzerland would not be that easy to get out and usually need to be cancelled with 1-3 months notice - when you get the bill it’s already too late.

1 Like

@nugget dear nugget, could you please have a look on my situation? I have read your posts. BTW what is "Wert- bzw. Kostenaufstellung” in English or French? I cannot find it online…Thanks a lot

thanks a lot. no I don’t have it in writing…

1.sorry I know it is stupid. but my insurance papers are currently in a friend’s place in a different city…is the “contract” the 9 pages that this OP has uploaded in his first post? I don’t remember having received any other document called “contract”, I have a similar document than that OP’s, and it is weird that there is no clause about cancellation, notice period etc in this document…

- is this the ombudsman service I shall use in my case?

Ombudsman der Privatversicherung und der Suva

I have read Homepage ch.ch - official information from the authorities and seems above one is the one I shall choose.

I guess it’s the same here: take the losses asap, reinvest in your low-cost ETF portfolio and be amazed 20 years from now on how much better it went. beware Schiller PE is high curently, so there might be below-average returns in the coming years. Still, that 6.8k policy sucks hard.

If you con prove it, i.e. have a signed document that says “I, the salasman did not transparently inform”, then you might have a chance suing. otherwise, you will have a hard time gaining anything from suing other than large lawyer costs

you can cancel the AXA policy - but the resulting cash is locked in the 3a system. put it to a 3a savings account (currently ~0.2% yield) or check out security depot solutions from VIAC, VZ, Banks, swisscanto,… around here, ppl will recommend VIAC/ VZ for most mustachian-like investments within 3a

Take it and run. your losses (including opportunity costs) increase every year you are with AXA and not with your low-cost portfolio. Mind, the AXA product probably contains some death- and work-inability insurance and make sure you sign up for according replacements in case you need those.

But make a prcize estimate of your losses: only a fraction of those 6.8k wen to building a stash, some of it went to fund the insurance policies. this money is not a loss but a cost for an insurance cover you enjoy. deduct this from your calculation, and then you will have a better idea on how much loses you have. will be smaller then you think now. see my post

Ombudsmann

i did not use that, and I cannot tell if it is advantageous. I dont know any details

Wert- bzw. Kostenaufstellung

this is a formal listing of what components of your policy cost what money, i.e. what goes to the stash, what tho which insurance. in my case back then, the whole thing included two insurances (death / work.inability). You can request it formally at your broker (or better directly with AXA). The interesting part in there was nut as such written in my contract.

In the end I am sorry for you, but there is no known way around just quitting and taking the losses.

1 Like

I got the same issue not a long time ago and felt scammed when I firstly analysed the situation.

After 2 weeks, I read my contract and remembered myself why I signed it → We bought our dream house and our bank asked us a life insurance because we were just a the limit with the cash (20%). My bank advisor proposed me a life insurance with 3rd pilar included. What I thougt was a good idea and signed without feeling scammed at that time.

Of course, you can invest your money and get more at the end but in the other hand there are some risks. Especially, when you have a family and you cannot earn any salary because of your sickness or even worst…

In my situation, I am thinking of asking the reduction of the amount of money I must pay every year (half of 6800.- chf) and invest the other part to a 3rd pilar Viac (3’400). For that, I need to send a letter (yeah still in 2019) to ask for it. Apparently it is possible according to the support of Generali.

Hope this is short enough, understandable and helpful ![]()

PS : Read your contract carefully before suing Axa. If you have a Legal protection insurance, you could ask them some advice.

2 Likes

thanks a lot, is it possible to cancel the current AXA contract before knowing where I will open my 3rd pillar? I don’t have too much time and energy till mid December, maybe I can open new 3rd pillar mid Dec?

I don’t remember having a copy of the contract other than the policy and a doc called “Protect Plan Dynamic - Application for your policy”, but inside I fail to find any clause about cancellation…

I have the same structure as you, death and work inability.

Does “stash” mean the savings part?

thanks a lot. you guys on the Internet are the only ones who are helping me on this issue. Nobody in my circle is well informed in this topic…

Opening a viac account takes 10 minutes.

3 Likes

In case, you can contact AXA to ask to send you the full contract.

1 Like

Hi @neutralname my case is still ongoing. I tried to cancel my 3A AXA policy but was told that the loss would be approx. 9000 CHF. I reduced the premium to CHF 100 per month and am now trying to reduce it even further to CHF 60.

The next consultation takes place in early Dec. I’ll update this forum when I learn the next steps. All I can say is that try to get out of your policy without losing money. I know that is hard, but its better to minimise your losses while exiting.

Thanks Sirob, I thought everybody in the forum told you to close your account with AXA ASAP, and I am surprised to see that you haven’t done so. I am as lost as you haha

Mustachians I need you help, here is some replies from the AXA agent this week in Italics. what shall I do especially for point number 1? would be grateful for your helps

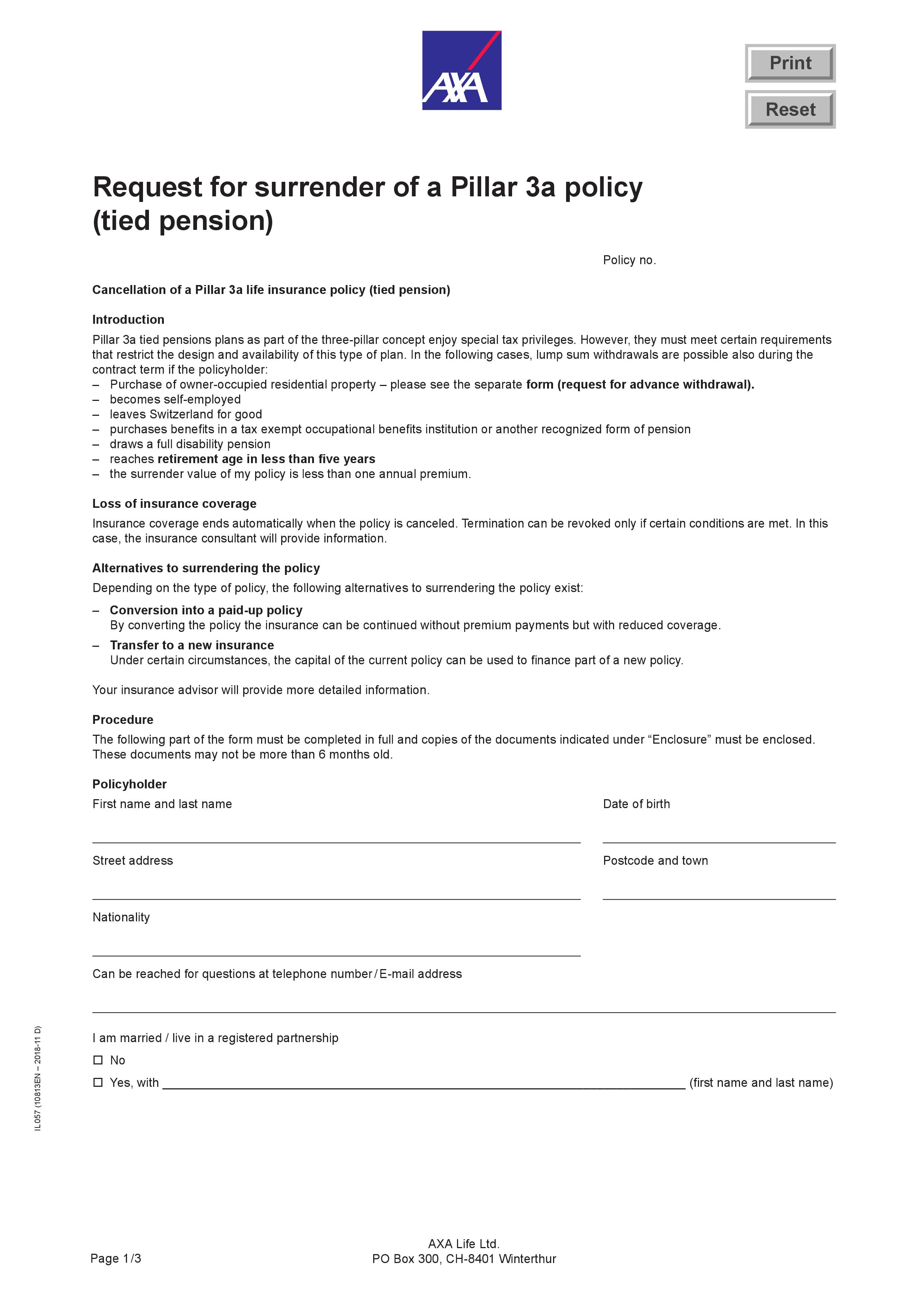

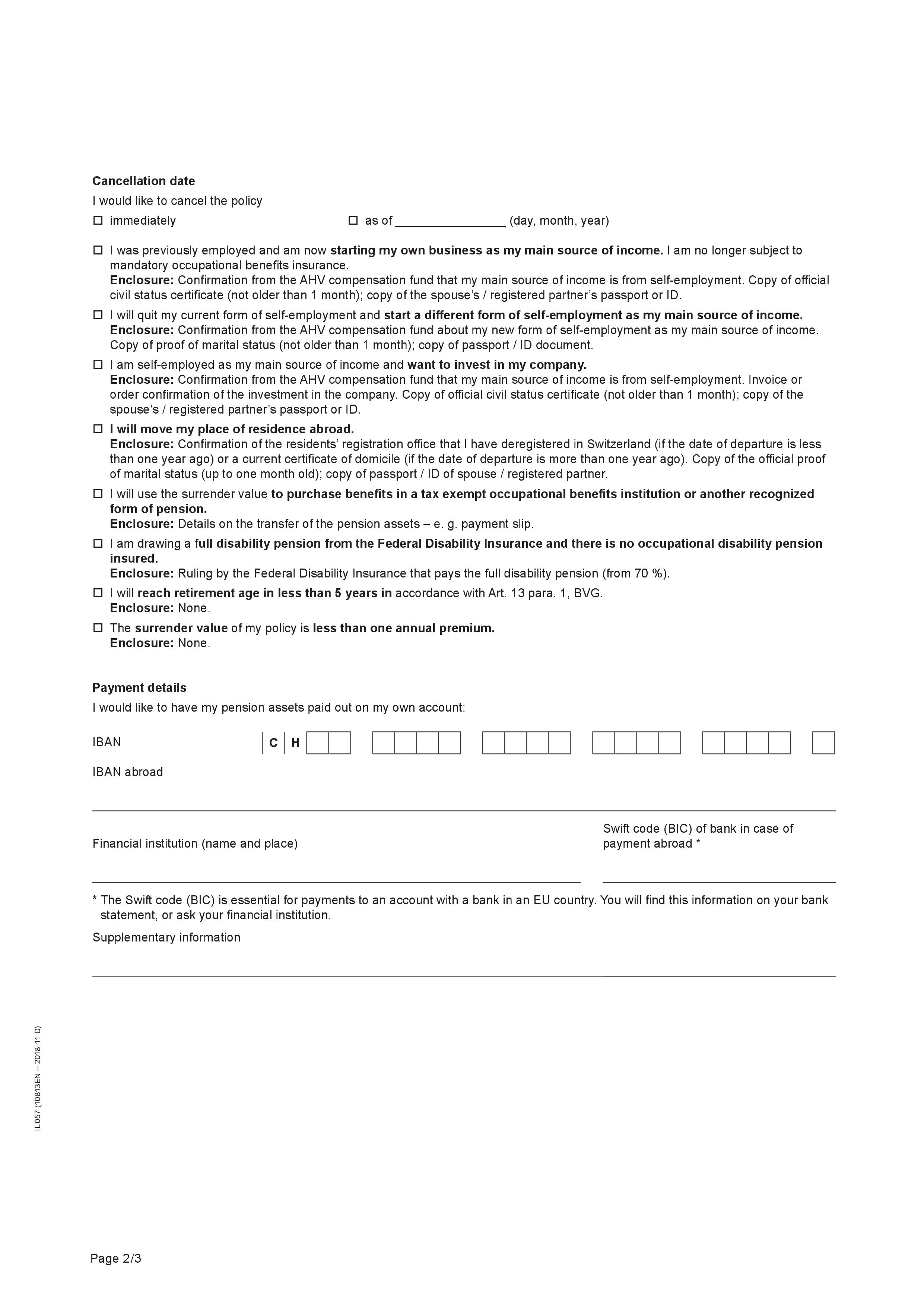

- The AXA agent sent me the attached form to fill to close my account, here is his comment, shall I sign it? Hope it doesn’t mean that I accept to only get the current surrender value. I still want to fight for the amount if it is possible to get back more:

You do not have to tick a box on page 2 for the moment, because you do not have the bank details of your 3rd pillar in the bank. You can open it later, whenever you want, it’s not a problem. Then, when you have the account details of your 3rd banking pillar, you can send them to me so that I can transfer the money on it.

On the first page, you must choose: “Conversion into a paid-up policy” and that’s all.

Just complete it and sign it, I’ll do the necessary.

- when I requested him “Wert- bzw. Kostenaufstellung”, which is a formal listing of what components of my policy cost what money, i.e. how much went to the saving’s part and how much for the death and disability parts respectively.” His reply is below, I insisted to have it and asked what is the 311 CHF as I never saw this number but no reply since 2 days…

However, I do not have a list of your premium details. To do this, simply do the following calculation:

- you have paid 6768 x 3 years (20’304 chf total)

- the payment of premiums cost 311 chf per year (933 total chf )

- the current value of your contract is 12’125 chf

So the cost of the life insurance and the contract costs are 7’246 chf.

- When trying to ask him a confirmation of the amount I can get if I close, I get below reply:

I confirm that if you close the policy with the form, you don’t need to pay the premium of this year.

The amount of your savings will then be 12’125 CHF (11’641.00 +484 bonus).

But…you can only remove it for the following reasons:

- leave Switzerland

-buy a property as a principal residence

-carry out renovations in his or her principal residence

start a self-employed activity

- Below is some general info he gave to me:

In your third pillar, you don’t have full life insurance.

Currently, in the event of death, we pay back the premiums you have saved to your beneficiaries…but not the final capital when you are 65 year’s old.

two insurances included in the contract:

- we pay the premiums after 2 years on your behalf in the event of disability due to illness or accident.

- after 5 premiums payment (so from next year), you can pause the contract and therefore not pay the year. You can do this 4 times maximum (in a row or not).

If the goal is to reduce the premium for this year, we can lower it if necessary, but if you don’t pay at all, then effectively, the contract ends.

if you leave Switzerland, you can touch your 3rd pillar, The value to date is 11,809 CHF.

You can also withdraw this amount for the purchase of a principal residence. But normally this is not done. The 3rd pillar is used for mortgage amortization. Because in this case, the tax savings are kept for the duration of the mortgage.

This is the same amount as if you cash out the money. There is no difference between transfer it to a 3a bank account or cash it out.

looks like we cannot upload PDF file on mustachianpost? had to convert them into jpg…

Hello,

From what I know, as I was about to subscribe to the very same AXA 3rd pillar life insurance (but finally not, thanks to you guys!), you could try to keep that policy but ask them to reduce the premium value to a minimum, i.e. not close the contract. I don’t know for sure how much of this is true and helpful, but still worth a try. Give them a call.

2 Likes

@Sirob

Hi Sirob, could you please reply my last question? I thought everybody in the forum told you to close your account with AXA ASAP, why do you still want to keep it? I may be in similar situation.

@Cortana @xorfish @nugget @pandas @Mr.Paprika @ilvalesco

My policy started 1st Nov 2016, do you think there is a deadline for me to stop and quit my current policy or I can do it at any time? the agent has not given me a precise date as deadline.

Would be grateful if you could help

Hello, I doublechecked MY contract and it is written it is possible to cancel whenever I want. You should check the general terms to be sure.

Options

- Keep that contract as a health and 3rd pilar (deductible for the swiss tax). In the future, you can use as a deposit to buy house/flat and you have a life insurance for your family in case of death. An option is to ask to reduce the amount of money you save on that insurance 3rd pilar every year and open a bank 3rd pilar (without life insurance)

- Cancel the contract and loose some money because you will get only the surrender value (by contract)

The final decision will depend on some parameters :

https://en.comparis.ch/saeule-3a/vorsorge/analyse/vorsorge-bank-versicherung

Sorry for the delay in responding.

Yes, many on the forum have advised me to cancel outright. By doing that, I incur a loss of approx. CHF 9,000

I am trying to get the annual premium reduced to CHF 600 and also trying to investigate of to utilise the eventual maturity value of the policy, approx. CHF 32,000 now and if reduced, around CHF 20,000 could be used against puchase of a house/apartment.

I have a meeting with Axa on 06 Dec and will update the forum when I come to know of the exact next options presented.