I doubt that anyone is going to rally and gather enough signatures against such a limited, rather innocuous change in a voluntary retirement scheme.

Edit: would be nice if it came in force this year, with the current bear market we‘re seeing. That said, for me, I‘m currently only about 7000 Francs shy of the statutory maximum amount for my age - so this new law would basically only allow me contributing one additional year (unless my balance takes another hit due to a bear market).

There’s even a very real chance that I‘ll surpass them eventually (once the markets are on an upswing again) and I don‘t get to benefit at all from this.

One consideration is that the 25-50% not (fully) contributing to 3a might be dominated by younger people. If they can catch up when they earn more as their career progresses, it can actually benefit at least some of these people as well, just not right now.

That said, I would definitely not be surprised by a referendum. It seems likely that this requires a change in law, not just a decree. And the SP will likely collect signatures for this. However, too early to estimate the result of a potential vote, in my opinion.

Say you’re broke this year or your marginal tax rate is much lower than what you anticipate for next year and pay 0 into your third pillar, in 2024 do you get that year’s limit + the unused 2023 amount for a total of around 14k? Or is it rather a “use it or lose it” situation?

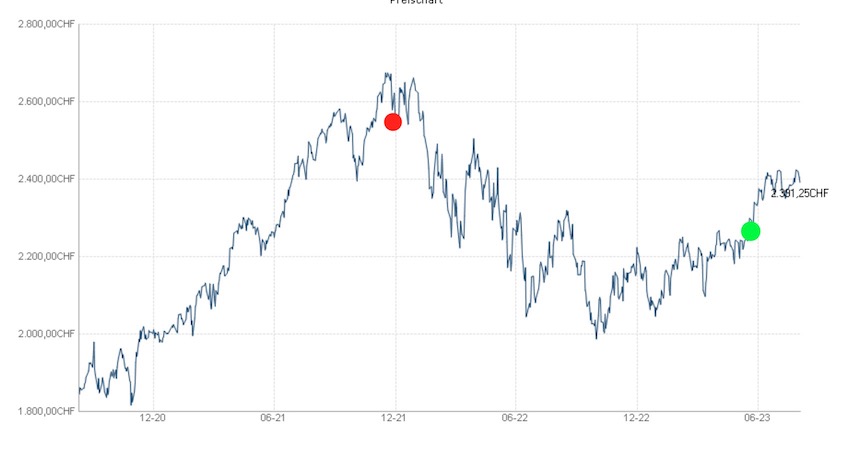

I recalculated my maximum buy-in again, and it likely would be just about CHF 2’000 at the moment. Even though I did not start at 25 and had my 3a funds in plain interest-bearing accounts or more expensive fonds for a couple of years.

They have discussed it several times and it always got declined.

One of the reason is, that only the ones with higher incomes will benefit from that. There must be a solution, where everyone can benefit.

So, contribute your maximum and don’t hope to be able to contribute voluntarily with higher amounts.

Did you go with 100% shares from the start? And for how many years have you been contributing?

My gap is around 45k. Maybe with a bull run I’ll be able to buy in the maximum.

Some people with lots of shares in 3a might be able to take advantage of it when there’s a huge drop in value… Timing the market would be good for once

There’s a Rational Reminder episode called “Praying for a bear market”. As long as you are in your accumulative phase, it’s in one’s interest to have low valuations.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.