Agree with 20 chars.

I check on my salary and on the annual summary of the lpp2 fund and the annual contributions on both part are the same (legal min).

The employer contribution also match this number.

The management fees are detailled in their annual report 0,23%.

The cost of the invalidity/ death insurance on the documentation is not clear but some costs for extra option can be found in the plan details.

Inclusion of additional capital in case of death: cost: 0.2 % if the insured salary if once, 0.4 % if twice, 0.6 % if 3 times and 0.8 % if 4 times. Option Risk+: cost: 0.3 % of the insured salary. Contributions for risks (death, disability): from age 25, they amount to 0.6 % of the insured salary for all administration costs, contributions to the guarantee fund and compulsory adjustment of pensions.

1 Like

Which of the plans do you have?

In the overview you can clearly see based on your age and plan what the respective % is for the “risks” part. The risks part is “lost” money, meaning it will not be part of your savings. It is the insurance part for death and disability. That’s why you have differences between the amounts you paid and the amounts you see in your pension fund.

However it is not clear how much of the risks that you pay and how much the employer pays.

Shouldn’t we notice it by comparing the yearly pension fund’s statement with our salary slips and what hits our bank account? I know many (most?) people don’t do that but it seems risky for the employer.

I got the detail of the risk part in the annual summary and it is on average 12,28%.

So on employer and employee contributions, 87,72% goes on average to the saving part.

I never understood the risk part until today…

I will be able to redo my calculations based on that.

Do you know if the pension fund also take out the risk part on the over-obligatory contribution?

1 Like

Just got spouse’s numbers: 1% on mandatory part and 0.25% on the extra mandatory part! Maybe they mean 1.25% on the extra part??

Each plan is different. But most plans will take out the risk also on the over obligatory part.

1 Like

6.5% interest for all pension capital from last year

So my buy-in’s over the last four years will result in some additional payout.

With my employer I was expecting considerably less as it’s usually around 2%. They had some catching up to do.

Also there is no distinction between mandatory and non-mandatory part of pension capital with my pension fund.There is only one rate.

5 Likes

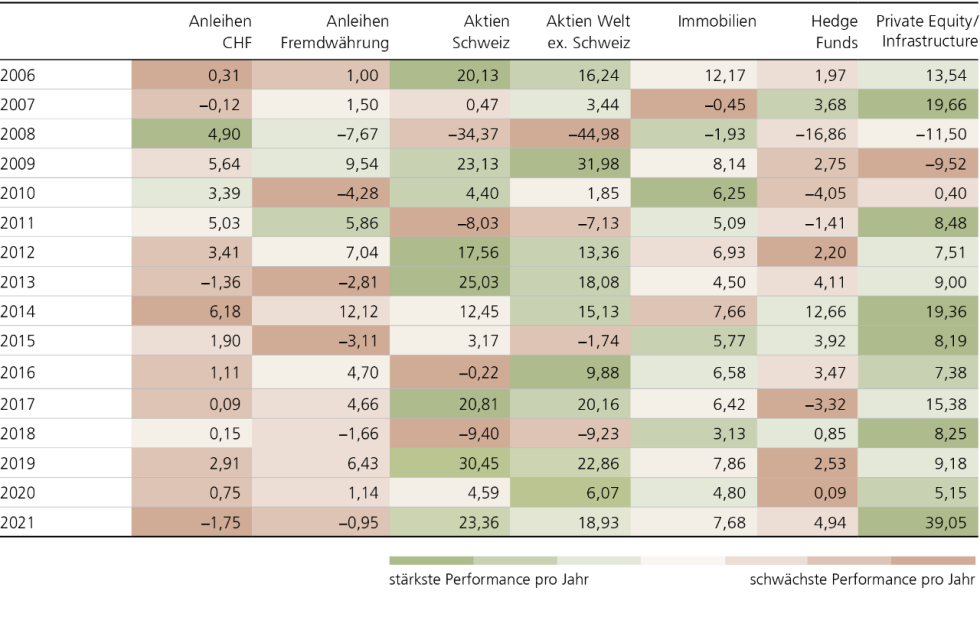

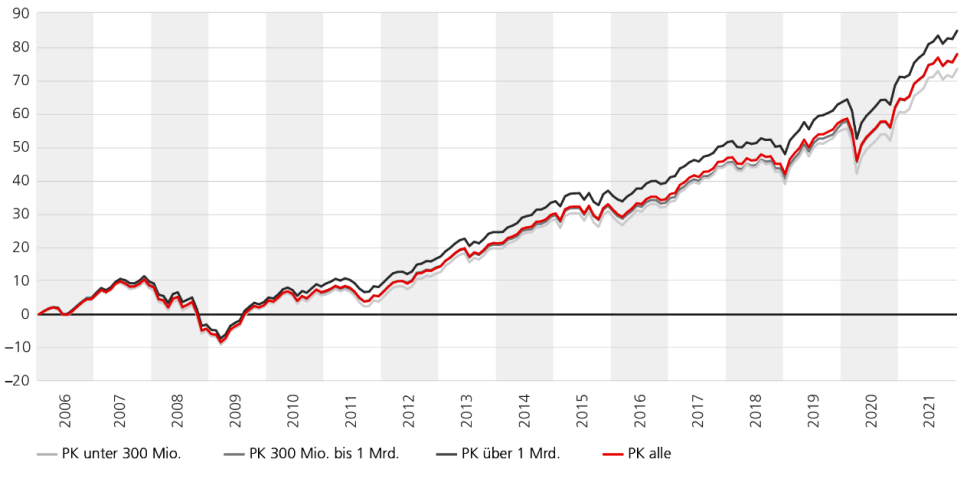

https://www.ubs.com/microsites/focus/de/markets/2021/pension-fund-performance.html

Interesting stats.

6 Likes

Now after we bought our apartment, I’m thinking about switching back from 8% down to 2% again.

I will pay more taxes, so I’ll get ~4.5% net more. But those 1.5% will be compensated by the higher yield of the stocks I would invest in ![]()

I would say staying with max contribution is sensible if you did withdraw money (WEF), but since you pledged your pension, this does not apply.

I guess it also depends on your future plans and how well the pension fund’s returns will be vs. investing individually. If you can beat pension fund returns +1.5%, then it’s worth it, but I guess you never know in advance. ![]() But there have been voices here that your employer has a high chance that it will have a couple fat years in the future.

But there have been voices here that your employer has a high chance that it will have a couple fat years in the future.

Another factor might be that you could still pay max contribs and do a WEF for renovations or reducing the mortage at some point in the future, while saving on income tax. On the other hand, Swiss regulations for withdrawals might change or you might switch to an employer with a shitty pensions scheme, were your future returns will be crappy and there’s no way to withdraw your money. In this case I would rather go with minimal contributions.

Personally, I would probably bit the bullet and pay a bit more taxes but have the flexibility with liquid cash. But really hard to tell.

1 Like

I think I’ll go this way. I don’t know if it will be the best financial decision (like you said depending on pension fund performance, maybe WEF etc) but at least it will give me more liquidity and flexibility.

In the end we are talking about a ~ CHF 300 per month difference. And who knows, maybe my next employer won’t have this option anyway.

Another aspect to take into account is that contribution is “paritaire” (parity in English?)

If you pay 2% from your salary then your employer pay 2% as well.

If you pay 8%, your employer contribution is 8%.

Employers matching isn’t the case in Switzerland. No matter which option I go for, my employer is always contributing the same amount.

4 Likes

According to BVG the employer has to pay at least 50% of the mandatory part.

If you can choose your contribution %, it is often the case, that everything above a certain percentage is for the voluntary part, and your employer always pays the same percentage, no matter which plan you choose.

2 Likes

OK thanks.

This was the case with my former employer. Some firms does pay 50% also on the voluntary part.

The way I look at it, your higher yield in stocks should compensate your first year marginal tax rate. Which for vast majority should be around 35-45%. Plus you will have to pay yearly wealth or dividend taxes on savings, so overperformance should also cover that.

In 20 years to break even you need roughly 2.5%-3% overperformance vs PF. But if you plan to move that contribution to mortgage covering or to stock based fund like finpension in 10 years → you need to overperform by +5%.

So for me PF contribution is more guaranteed vs betting on overperformance, the downside is it’s nominal, not flexible and highly dependent on your time horizon

He is talking about marginal tax rate, not overall tax rate and I assume he was talking about the people in this forum, which mostly have a salary way above averagr.

4 Likes

While I agree with your point, @sammiz is talking about marginal tax rate (as that’s relevant for tax deductions), not average tax rate.

In ZH, 63.8% have a taxable income of 40k+¹. With a taxable income of 44k, the marginal tax rate in Zurich is 16.33% for singles (lower for others). And the highest tax bracket in Zurich has a rate of 41.7%. This is highly canton-specific, of course, however, the marginal tax rate of the vast majority of the population is most certainly not in the range of 35-45%.

2 Likes

In Zurich with a salary of gross 130k, single, no children, no religion, you have a marginal tax rate of 30.7%.

3 Likes