I think I’ve asked it already several years ago with less people on board so I ask again.

Anyone has already calculated the possible outcomes with Pensions (1 and 2) if you FIRE between 20-58 years old?

All 2a I’ve seen they let you calculate what happens if you stop working between 58-65. Is there a calculator that can show you what would happen if you pay 2a even without a job? I think the loss by stopping at 58 are hight and it might make sense to pretend a job or something like that. 5-10k paid this way might earn you 200-300k more on 2nd pillar.

The same with 1st pillar. I know you must pay it anyway, but I wonder if there is a simulator, other than this site: https://www.acor-avs.ch/requerant

where again you should probably select to go to pension at 65 and pay the years you won’t work. You ca put by hand some values on the table it generates. Probably not 0 since you must pay something anyway.

Are you trying to figure out how much you pay in or get out?

Pay in

1st pillar: mandatory to pay until legal retirement age (65 men, 64 women). If you don’t work, they will calculate a mandatory amount based on your pension and assets, with a cap of maximum amount due of 25’150.-/year !

2nd pillar: only is mandatory to pay if you are employed (with a certain minimum salary, 25’095.- in 2021). You cannot pay in without a job.

Get out:

1st pillar, at earliest 3 years before legal retirement age (with each year you anticipate, you lose 6.8% forever). The amount you get varies between 1’195.- and 2’390/month (2021 figures). If you’re married, you get max 1.5x those amounts both (not 2x !)

2nd pillar, officially only from 58 years old. Before that, at certain conditions (house payment, establishing an independent position). The amount you can get depends on your paid in capital and employer’s pension regulation. Most of the time you can get your full capital instead of pension.

I’m trying to optimize the amount of money I get back. For 1st pillar it’s better to do at 65 or maybe later. The amount you pay in is less than what you get out. If you exit earlier, you lose a lot.

For the 2nd pillar, if you can’t continue paying will you get the same (projected) amount or there is a certain part that get lost?

I think you have to move it to a vested benefit account and then (from 58 onwards) you will withdraw (and be taxed) based on the type of vb account (cash, stocks,…) and its earnings.

I’m also interested in additional info on this as I think it will be the case for all of us if we RE…

From what I now, if you stay in Switzerland and FIRE before 58, you cannot cash out your second pillar. You have to move it to a vb account. The gains of this type of accounts are tax free, but you pay the lumps sum taxes when you cash it out (between age 60 and 65). Since this tax is progressive it is better to split your 2nd pillar to 2 separate vb accounts and cash them out in different years.

About the projected amount, it will be different than your actual pension statement. You have to reduce for the missing contributions between FIRE date and 65 (they are the biggest between 55-65). On the other hand, you can probably use a higher return assumption than the projected interest from your statement if you choose to invest your vb accounts in something with high stock allocation (possible with viac, valuepension, maybe others)

If you stop working your 2nd pillar will be held in a Vested Benefit account and when you reach retirement age it can be withdrawn as a lump sum and taxes paid. It won’t be converted to a monthly payment https://www.valuepension.ch/faqs

If you expect to live longer than 82 years, I would:

Take SS as late as possible (67 right now).

Keep your pension fund assets in a vested benefits account (Finpension/Viac and keep it invested) as soon as you leave your last job.

Take out your 2nd pillar when you are 70 years old. Immediately reinvest it in IBKR as soon as it’s available to prevent being out of the market too long.

Live with your taxable portfolio (IBKR) till 60 and then use your 3rd pillar accounts year by year to cover some or all of your yearly expenses.

Gives your taxable portfolio some air to regrow and ensure that there will be enough by the time you take your 2nd pillar at 70. AHV starting from 67 will help too.

Live happily after till you are dead. The higher AHV will ensure that your portfolio will last in the case you get much older than expected (90-100).

Edit: I just saw that you can take AHV at 70 and increase it by 30% that way. So do that if you are 65 and still in very good health.

Quite easy assuming you don’t work, even part-time and don’t own a company.

AHV

You need to pay AHV based on your wealth. Based on the current trend, I would assume that the amount you’ll receive will be near zero It’s impossible to know how much you’ll have

If you are afraid to run out of money before you die or even not to be able to manage your money, you can convert a lump sum into an annuity. Insurers offer that, but the rate is low. I’m not sure that I will still be able to manage an IBKR account at 90

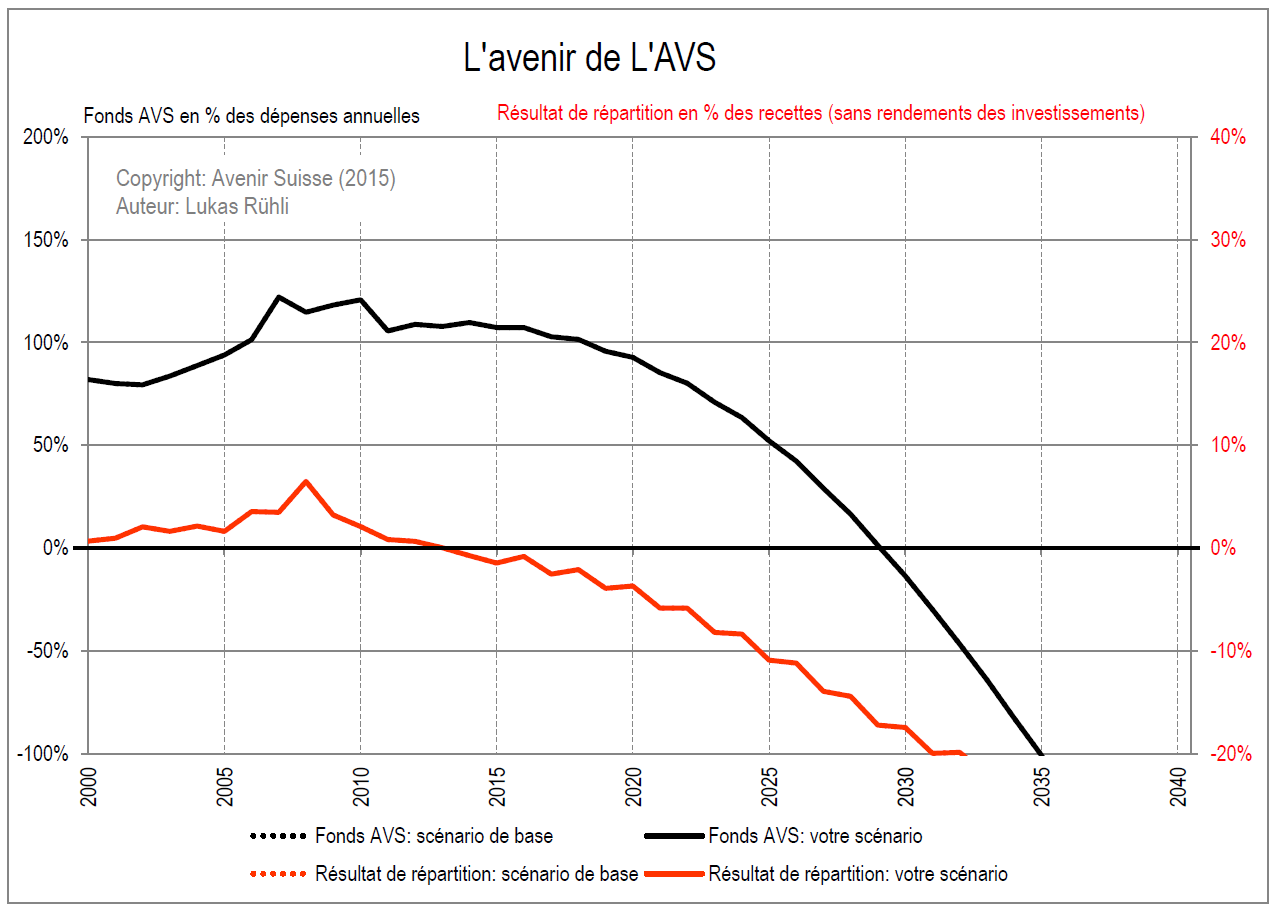

I’m not sure how the percentage used in the graph is calculated.

(In german it’s “Umlageergebnis in % der jährlichen Einnahmen (ohne Anlageertrag)”, but I can’t really see how we arrive to these percentages with that.)

My current plan is to retire at 50-55. The exact age won’t change anything I’m planning on doing, but lets assume I retire at 53. By this time I will have roughly: 1.6M IBKR, 400k in Viac and and 500k in my pension fund, so 2.5M in total. 90k/year would mean a withdrawal of 3.6%. Now always speaking about inflation-adjusted 90k:

53-61: 720k from IBKR

61: 90k from Viac 1

62: 90k from Viac 2

63: 90k from Viac 3

64: 90k from Viac 4

65: 90k from Viac 5

65-69: 360k from IBKR and whats left of my 3rd pillar assets

69/70: Now taking my vested benefit accounts (probably 2) and transferring it to IBKR. AHV/SS will start at this age too.

Expenses go down to 55k because of AHV/SS. Withdrawal rate probably below 3% at this point because of that. Ensuring that the portfolio will last for the rest of my life.

I tend to think like @wapiti. If you can use your 2nd pillar at 70, maybe it’s better to convert it to a pension even if it’s not theoretically the best solution, as long as you can still pay your expenses and as long as it is possible.

Not sure about the trend of AVS/AHV. I believe they will bail it somehow, maybe by raising VAT

Killing the AVS means chaos.

You can by voluntarily contributing (though of course course the question is if it’s worth it).

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.