Since the Revolut thread is growing in other directions and it always hard for new people to find information I open this new thread.

What is the best credit card to pay for stuff in foreign countries?

Note, I say “foreign countries” because most of the “normal” credit card will make you pay 1-1.5% surcharges even if you pay in CHF if the company is abroad. I am not sure exactly how this works, I suppose you should google if that company has an office in Switzerland? Weird.

It used to be Revolut, but from the (confusing) new information they have sent to their clients, it seems that from now on you have to pay 0.3% (minimum 0.30 usd if in usd or 0.3eur if in eur), not sure if it’s after a minimum. Sending money to other accounts in EUR/Sepa zone seems to still be free.

I dont think the payment fee changes are that confusing from Revolut.

If you send EUR within SEPA or to other Revolut users, it’s free.

If you send a payment in the local currency of the recipient currency, you pay a 0.3% fee (there’s a minimum & maximum, see table 1)

If you send a payment not in the local currency of the recipient currency, you pay a flat fee depending on the currency (see table 2)

There is no allowance for standard users, only for premium (one free payment per month) and for metal (3 free payments per month)

Neon is a general solution, their small surcharge applies to all (normal?) currencies.

TransferWise would be an alternative. They have a debit card and a multicurrency account. Whether or not you pay more than with Neon is a bit complicated to find out. The Mastercard rate, applied by Neon, is daily, the rate TransferWise uses is updated more often (real-time?). My feeling is, however, that Neon is a bit cheaper. Both should be in the same ballpark as Revolut and much better than normal Swiss credit cards.

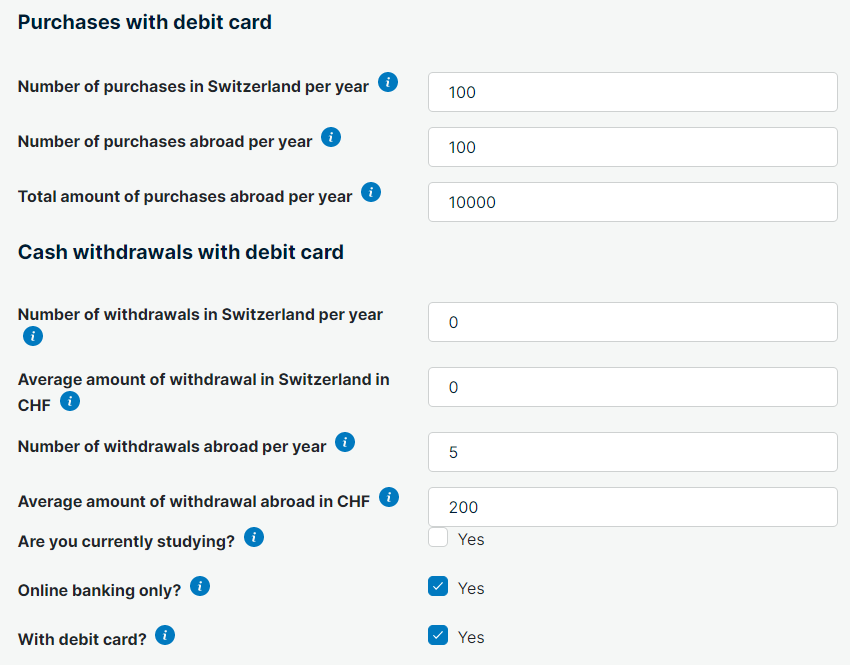

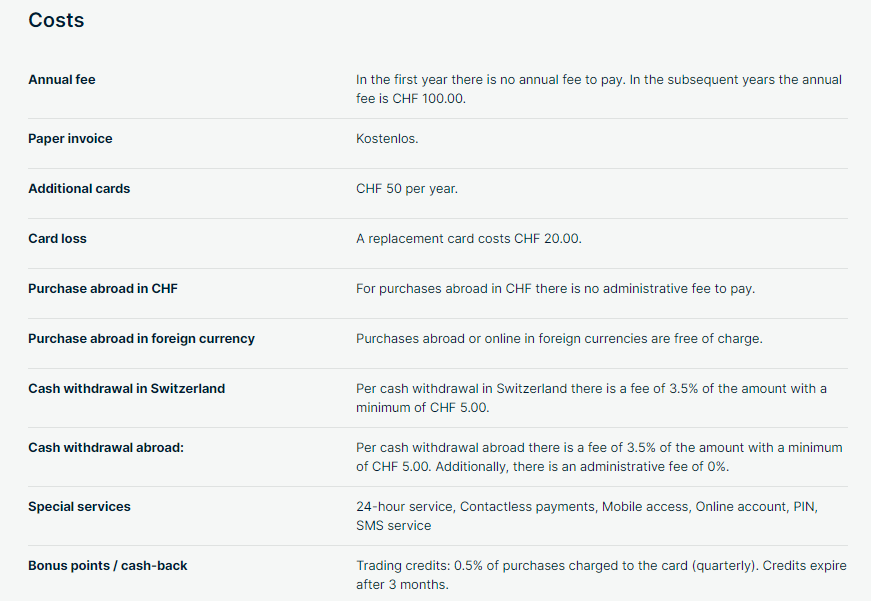

I fixed the thread title. By the way, I ran the comparison tool on Moneyland and there the “cheapest” card for usage with foreign currencies was the Swissquote card. 100 CHF annual fee, 100 CHF fee for paying 10’000 CHF (equivalent) and 50 CHF for withdrawing 5x200 CHF (equivalent). However, as you mentioned, debit cards (prepaid or not) are probably cheaper.

So if I would go to Poland and pay an equivalent of 10’000 CHF in PLN, they would charge me 150 CHF for it. But Moneyland calculates 100 CHF, so I don’t know. Maybe they take a “mix”. Anyway, 100 CHF annual fee is already high. Would be OK if everything else was free.

We use the Mastercard reference rate. This is a bit complicated to explain. Suppose it’s Monday, you are abroad and you pay for a croissant with your neon card. The croissant costs 1 euro. The euro exchange rate at the time of your payment is 1.10 CHF. However, your payment is only booked on Wednesday. During these two days the exchange rate moves up to 1.15 CHF. Your croissant is suddenly 5 centimes more expensive. To take account of this difference, Mastercard retroactively calculates an average exchange rate for the day you bought the croissant. The average rate on Monday was 1.11 CHF per Euro. Thus, the croissant is only 1 centime more expensive. Of course, the reverse is also possible: If the average exchange rate on Monday is 1.09 CHF, then you have saved 1 centime. If you now buy a croissant abroad every week, the differences should even out at some point, because sometimes you have to pay a little more and sometimes a little less.

They definitely do (since it’s fixed for the day, they have to price the risk of currency moves). Depends on currency but iirc it’s in the 0.1% - 0.5% range. (the schwab debit card uses the visa rate, I use it sometimes when I’m abroad, esp. nice for withdrawal since they reimburse the ATM fees).

Isn’t it great how this thread again highlights the need for a online service where you can set your owned credit cards and then actually input the transaction you’d like to make to get the best card to use?

Neon is one of the best alternative to Revolut if you are looking for a swiss based bank (or services that is covered by a swiss bank).

I used neon during a 10 days trip around Czech Republic and didn’t withdrawn any cash since I could pay all my purchase by card for nothing… (well ok maybe not for nothing because the FX rate was fixed by MasterCard but at least I didn’t pay an extra during the weekend).

I also used their Transferwise solution (0.4% commission for neon) to send money to a friend in Czech Republic.

If you don’t mind to over optimize everything, I think that neon is a good solution. I prefer that than having 4-6 differents credit card for each purpose… Simplicity sometimes is better.

PS : neon is also my “everyday credit card” (I don’t have a real credit card and I don’t see the benefit of having one, for now at least).

Transferwise works great for me… I regularly use it to transfer money to/from others in EUR/USD/CAD/GBP and to buy things online in those currencies + CHF. I always keep some money on it for online purchases. A lot of EU- and UK-based retailers will charge you in CHF (e.g. snowleader in FR, bergzeit in DE) but credit card companies charge the 1.5% fee on this so it is better to pay with Transferwise. Conversion fees are cheap, although maybe not the absolute cheapest for all currency pairs. You also get 200 GBP equivalent in free monthly cash withdraws, which is useful in certain countries where cards are not accepted everywhere.

I have a spouse from the US and we still have a US credit card that gives 1.5% cash back on all purchases with no annual fee. We put all non-CHF denominated purchases on this card. The forex spread for EUR is approx 0.6% and there are no foreign transaction fees, so we make approx 0.9% on each purchase. We could also do this for Swiss purchases too but for some reason that just feels dirty

To pay off the bill each month I send cash to Interactive Brokers, covert to USD, make my ETF purchases, then withdraw (minimum 3 days after deposit per IB terms) the card balance to the US bank account.

Convoluted? Yep…but it’s routine for us now.

For any of you that have access to US banking, you could try this. The bank has never complained about our lack of contribution to their bottom line in the nearly 5 years we’ve been doing this.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.