My company is offering me to choose between three options for my second pillar, and I’m not sure which one is the best financially speaking. The company contribution wouldn’t change, while mine could be either 1%, 3.5% or 8%.

I’ve checked this thread where most people suggest contributing the maximum amount we can to LPP, but my poor maths seem to indicate it’s the worst option overall.

Edit: Because my math was wrong obviously… See in the comments.

My assumptions are:

2nd pillar returns are 2.5% per year

Stock market returns are 6% per year

The diff between each plan has to be added to my taxes as it’d be more/less net income

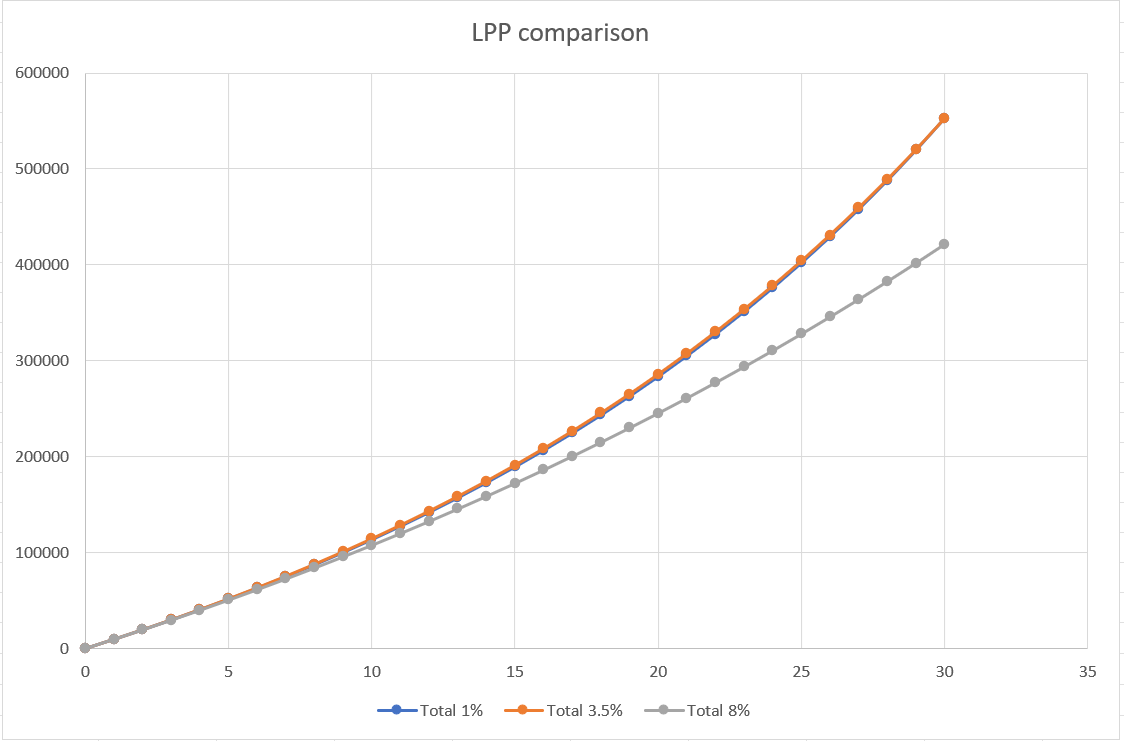

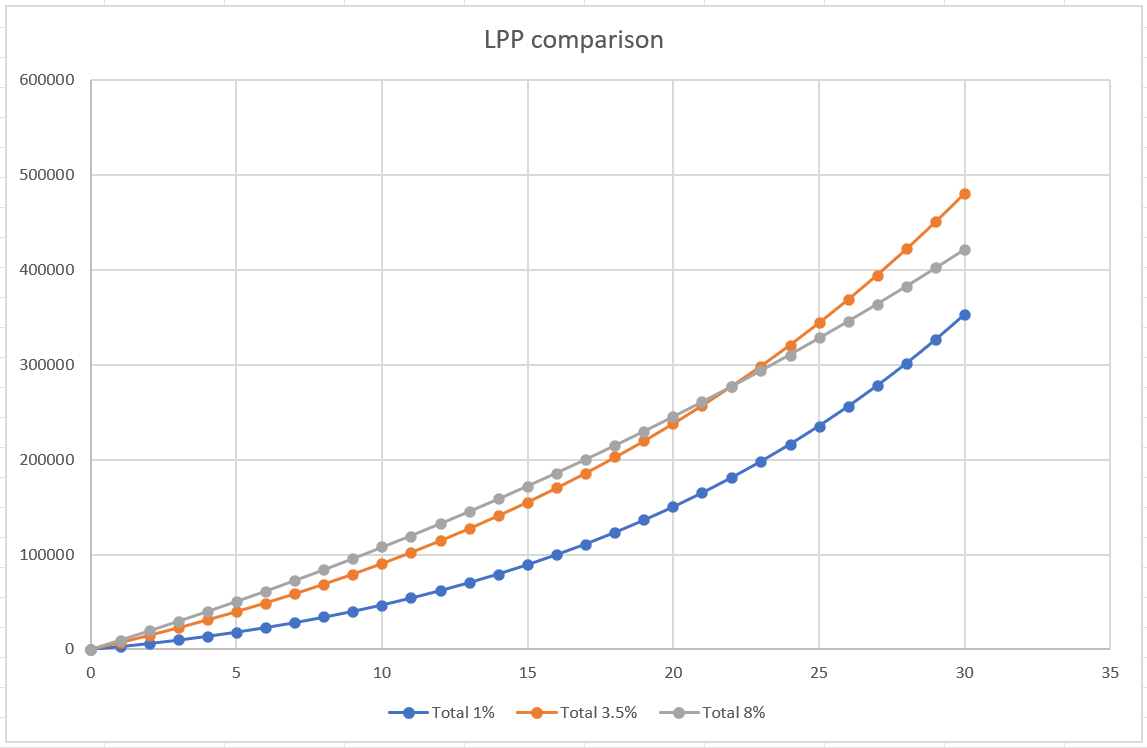

I’ve ran a tax simulation for each scenario just taking into account the family net income, and based on my assumptions I end up with this 30y plot:

For each model, I just take the sum of the 2nd pillar contribution + returns, I deduct from it the potential extra taxes (0 for 8% contribution), and I add as well the stock market contributions + returns (from which I also deducted the extra taxes to be realistic).

And while the 1% and 3.5% plans seem super close to each other, the 8% plan is way behind (for the 8% plan we basically just count 2nd pillar, as nothing goes to the stock market and it’s the minimal taxes I could get).

First, does it make sense ? And second, assuming the 1% and 3.5% plans are fully equivalent, is there a good reason to go with one more than the other ? I feel like going 1% allows me to have more control over my money as it’d just be on the stock market. On the other hand, putting more on 2nd pillar gives some (ridiculously) little guaranty, and opens the door for voluntary contributions further down the line, although it has the inconvenient to complicate a potential real estate transaction.I’m also thinking, this is very dependent on my tax rate, and if in the future my tax rate goes higher due to better family income, maximizing LPP would help, while if we choose to have kids and work part-time thus reducing our tax rate, stock market + minimal contribution would work the best. Is the logic correct?

Not adding much advice, but congrats for arriving at your level for asking yourself the question (worrying about optimizing taxes).

I personally also found it hard to see the benefit of paying into pillar 2 (also comparing the tax advantage to the “market return”).

I ended up paying a ton into pillar 2, but I am also rather close to retirement (or at least close to being eligible to payout of pillar II).

Other thoughts:

your assumption for stock market returns of 6% seems ambitious. It’s not unreasonable, but you will pay taxes on the income (dividend/coupon) portion of that return. The tax will of course be dependent on your income bracket.

your money paid into pillar 2 of your employer will be protected from downside on market downturns. Of course, it also won’t benefit from upturns as much as the market will.

When I left my former company in 2020 I paid 1/3 into Freizügigkeitsstiftung 1 and 2/3 into Freizügikeitsstiftung 2. When I accepted a new job in 2021 I moved the funds from Freizügigkeitsstiftung 1 to my new company’s BVG, and, ahem, forgot about the rest at Freizügigkeitsstiftung 2.

My BVG at my new company has since appreciated a few percent, my assets at Freizügigkeitsstiftung 2 has depreciated about 5% (lows were at over 10% in 2022). This is completely normal, but you should make sure you can stomach the drawbacks in your personally managed money compared to if it were tax sheltered and drawdown protected in your pillar 2 (for me, the drawdown was 6 figures, and I had to keep re-assuring myself using the sentences I just preached to you).

Similarly, you’ll have to be able to live with assets tanking in your personal funds (and hopefully soaring when Mr. Market is happy), while you’ll see your assets shoved into pillar 2 will be protected against any (well, most) downside while being limited in participating in soaring upsides in “the market”.

I think those assumptions paper over a lot of things: the risk profile and volatility of those is very different.

If your investment strategy is 100% stock and you’re happy with the risk that’s good. Many people prefer something more balanced (e.g. mix of fixed income / stock), in which case pillar2 can often be a good substitute for fixed income (similar return, huge tax benefits).

Edit: I wish whenever people assume 6% or more in any model, they’d use a monte carlo simulation instead, it’s much more revealing if you know that you have e.g. 20% chances of losing money over a decade.

Thanks @nabalzbhf and @Your_Full_Name, you’re right, 2nd pillar has much less risk and volatility and is probably more of a slow but steady increase, whereas stock market can have huge increase and decrease. For what it’s worth, at the moment I have no reason to be risk averse as my wife and I both have good income, good investments and good 3rd pillar. We’re decades away from retirement, that’s why I count 6% on stock market, I guess/hope on 15-20+ years big downturns have good chances to have recovered already (I already started investing in late 2021 and only went to positive numbers this summer, I managed to ignore the huge negative unrealized P&L).

Now even with all that in mind I’m still a bit hesitant. But since the 8% case seems to be losing by a lot, maybe a conservative 3.5% is a good compromise.

I also have a kind of (probably irrational) fear that in the next decades, some money put in LPP could be “lost”, e.g. if there’s a change in the retirement system. This fear comes from a lack of both trust and understanding of the retirement system. While the stock market could go in any direction, it feels more transparent to me, I know better where the money is and have more tools to control it.

As per Cortana’s calculation and summary here, max out your contributions if you withdraw it in the next 10 years or less, otherwise go minimum contributions and invest yourself. Don’t choose the middle ground, as it’s the worst of both worlds.

Edit: number of years are highly dependent on your marginal tax rate, your pension fund’s performance, and the stock market performance.

Are you sure? Voluntary payments as in buying should be available either way. It’s calculated based on your current insured income and the “missed” years.

How so? If you plan to buy in a few years, you could combine tax savings now, a stable return and getting the money out if you want to. Stock market wins with your values only in the long run, and the risk is not suitable in case the money is needed in a few year.

Maybe better to start with what your overall allocation looks like (stock, bond, etc.). And once you decided on that you can figure out how to implement it (which can involve Pillar2 and 3a).

My overall allocation is approximately 7% cash in bank (emergency fund), 35% 2nd pillar, 21% 3rd pillar (all invested on VT-like fund) and 33% invested in VT. The rest is some assets we can ignore.

I think the chance we want to buy real estate in the next 10 years is high indeed, we’d love to have a house, but live in a HCOL area, so we’re not quite there yet and even when we’ll be, we’ll have to ask ourselves if it’s really worth taking the risk putting 2M there (+ we’re not the most DIY-ready people, so owning is especially scary). Oh and should we get kids, we’ll probably start working part-time, which would highly reduce the kind of loan we can get. Could force us to keep renting (not that bad).

Well I feel very stupid but I did a horrible mistake in my spreadsheet, and counted the taxes as income instead of expenses. The outcome was completely wrong, here’s what it looks like now:

Sorry for starting a thread based on a mistake, at least now it makes sense since the result is well aligned with all your advice and the ones of the other thread.

Based on this, I’ll go all in LPP (8%) since even if on 20+ years it’s not the best, while taking into account low volatility and availability for real estate, it’s indeed much better. And that’s without even counting potential taxes on dividends, or withdrawal tax for real estate.

Your conclusion is legit, but the chart still seems off. With 2.5% and 6% net return, the lines should cross sooner, around 10 years at 30% tax.

And the 1% option take the lead (highest investment in high-yielding stocks).

How are you calculating the tax effect? One simplified option, with an insured salary of 100k could look like this after 1 year:

8% contribution: 8k * (1+2.5%)

1% contribution: 1k * (1+2.5%) + (8k - 1k) * (1- 30% tax) * (1+6%)

My formula is almost the same, except I take into account the increase in tax rate for the 1% and 3.5% models. I didn’t do this through the formula, but with a simulation on my state tax platform.

The final formula looks like this for a 100k insured salary:

8% contribution: 8k * (1 + 2.5%)

3.5% contribution: 3.5k * (1 + 2.5%) + (8k - 3.5k - tax_35) * (1 + 6%)

1% contribution: 1k * (1 + 2.5%) + (8k - 1k - tax_1) * (1 + 6%)

Where tax_1 and tax_35 are constants, worth respectively the yearly difference in tax between the 8% plan and the two others.

Comparing pension funds with stocks is pointless. Swiss occupational pension fund benefits belong in the bond portion of your portfolio.

If higher contributions to your pension fund would result in your portfolio having an overinflated bond component compared to the stock component, then you should choose a (lower) contribition that matches your portfolio.

But if the stock/bond ratio will remain balanced even with the highest possible contribution, then I recommend you use the highest contribution.

A Swiss occupational pension fund is one of the most secure bond investments you can make, and the interest rates are generally higher than those of bonds with the same creditworthiness. At least when compared to bonds in CHF. Then there is the tax saving which adds to the yield. Personally, I would choose a Swiss pillar 2 pension fund over just about any corporate bond and most government bonds.

Also keep in mind that you will still pay a tax on 2nd pillar money in the end. A much lower rate, but at the final total that include the gains.

The difference in wealth tax could be added as well, but it is mostly a negligible difference.

As a rule of thumb, paying extra into 2nd pillar can make sense if a) you are too low in bonds within your asset allocation or b) if you are getting within 5-8 years of RE (where you can then transfer it to e.g. VIAC & invest more freely), the closer the more significant the one-off tax benefit.

Before concluding that pension funds have bond-like characteristics I suggest you look into your fund’s portfolio strategy. Mine has an allocation of 50% stocks, 30% real estate, with the rest distributed among bonds, cash and alternative investments.

So that payoff will be very much not like corporate bonds – and, correspondingly, you’ll want to factor in higher growth rates

(c) If you sleep better with no downside volatility in pillar 2 compared to missing out on potential further upside on pillar 3 and you are therefore able to stick to your plan.

Without your emotions it’s just numbers on a sheet going up and down and usually stabilizing over years, sometimes a fair bit longer, and statistically, things work out just as @ChrisL describes, but your personal outcome will depend on how you personally will behave in protracted (or even short downturns), or if your planned RE start date collides with a downturn or sideways market in your pillar 3.

Anyway, complicated way of me saying that in (investment) theory everyone has a plan until they get punched in the face by the market.* I (now) tend to err on the risk adverse side (pay into pillar 2) at the cost of missing out on (probably only slightly) better returns. YMMV.

But for you it might behave like a bond even if it doesn’t consist of bonds, the fund takes a very long term strategy and has reserves that reduce the volatility/risk massively.

edit: as you say there’s a good chance it returns even more than bonds, with lower volatility than holding equity yourself.

Sure, there are subtleties, but in terms of an investment portfolio, a Swiss pension fund is a fixed-yield product, so it belongs in the bond component.

The stock-to-bond ratio doesn’t have to do with optimizing returns, but with managing risk.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.