Hi,

I currently have a 3a with VIAC, and very happy with its performance.

I understand it is good after reaching a certain amount to open a 2nd 3a. And it is good to have 3-4 3a once we reach retirement to withdraw it.

So I am looking for my 2nd one.

My partner is working in an Insurrance company (a large swiss one ), and as a family member I am entitled to a “discount” on those products. They finance 20% per month of the maximum amount for a 3a. So it would be something like: 7258/ 12= 605. I pay 484 (+ a monthly fee for the insurrance line 15), they pay CHF 121 approx.

As I read it, this means a “free” 20% ROI per year garantueed. 20% is quite good, even compared to the VIAC products fully invested on the Trade Market.

I am not even speaking of the Life Insurrance product behind, it is quite untransparent. And I am not expecting to make a real profit. Just benefit from this deduction.

I know those products are quite unpopular on this forum, and I agree. But I would like some opinions on this “deal”

Thanks so much all!

PS: otherwise I will probably go with a 2nd 3A at VIAC

The “deal” here is that you would just lose less initial money with it (e.g. -10% vs. -30%).

Its “performance” over the long term will still be rubbish compared to a 3a under your control.

Simply skip.

No, not 20% ROI.

It’s 25% extra of your invested money that goes in.

Returns will be what they are (i.e. probably close to 1-2% p.a. over 30 years, and definitely negative in the short term once you decide to get out of it).

I have the same suspicion as these companies are usually not well aligned with customers. Have a look at their funds/ETFs and compare their TER with best-in-class TER of other 3a offers. Could there be any extra cost for buying and selling?

I would also check how conditions change after moving to a different employer.

That’s definitely not a viable option, you’ll pay a huge penalty for these insurance linked solutions if you quit before the contract ends. I work for a large swiss insurance company.

I am assuming OP has not yet asked for an offer, and thus, does not have the full details.

And just to be clear, as @Burningstone mentioned already, the penalty comes from the share of the contribution allocated towards the insurance component of the contract (which is usually 100% in the first years).

And there are other factors to consider, like higher management fees for the investment product in the insurance contract, feeding/withdrawal fees of the funds, etc.

I tried finding some details on the ETF or other financial products behind the Insurance product itselft but I don’t find any, I will ask. Same for the conditions to terminate the subscription (probably the usual for 3 A, if I buy a house, etc)

Over 25 years they indicate a possible returns between -1.5% p.a. up to 6.5% p.a. (this is a simulation)

I must take into account the monthly fee CHF 25.00 of the insurance that comes on top.

And you are right, if my partner leaves the company this contribution ends, maybe it is allowed then to quit with less strict conditions, I will try to get some info.

Seems to be too many variables that would impact a potential decent returns…

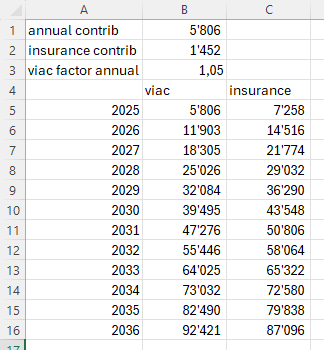

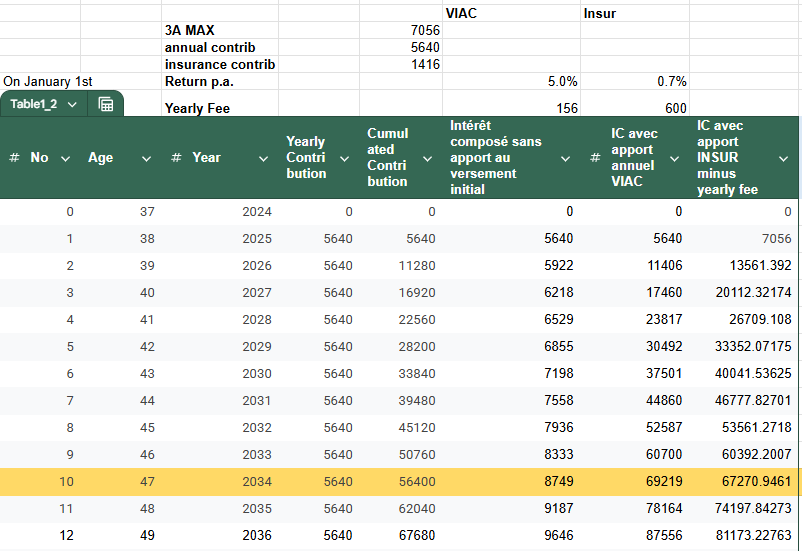

Hi, So I crunched my number based on the template you did @prodent thanks for this!

With this simulation, if I understand correctly, in 2034, it becomes more interesting to be on viac at 5 % p.a. than on the insurance at 0.7% p.a

We checked the conditions to transfert to another 3A and this is without any cost it seems.

So is it fair to say that it is interesting to keep this product until 2034 ? And after to leave?

PS. No I don’t need the life insurance product itself.

PS2. I took the decision to open a 2nd 3rd pilar at Finpension, to diversify from Viac. The main reason is the committment expected by this product.

I will still continue my analysis of the above, but for my partner as she took this product already some years ago. Thanks all for your help!

Wow that’s very odd for the insurance company (imagine if this “employee benefit” was common practice for the public ).

For your own assurance, please double-check and confirm in writing (that surrender value is not “70% of what you paid in”) before commiting to anything, “it seems” is not enough.

I would also be very cautious as they might not classify money missing from the surrender value (compared to the sum of non-insurance contributions and returns) as fees. At least for regular customers, insurance companies can be very sneaky.

In order to provider further guidance we would need the offer & their avb (insurance terms).

Usually the devil is in the detail and all reviewed insurance 3a so far are close to scam.

But lets be open and check the one youve mentioned, once you can provide more details.

That’s very possible. The question is rather - what would be the surrender value by then vs. how much have you paid? Did you see the table with guaranteed surrender value?

Hi all, thanks for the last messages, didn’t reconnect in a while.

I went with a Finnpension, as it is more flexible.

It could be that my partner pull out of her own contract, before that she would of course check as much as she can the conditions. If I can I will provide some specific details here (surrender value, etc.), so far you are right I didn’t see anything in writing about those… it is so obscure! Quite hard to have “on paper” details about anything…

Indem du dieses Forum liest und daran teilnimmsch, bestätigsch du, dass du d Forum-Richtlinie glese hesch und damit einverstande bisch, sowie mit em Haftungsausschluss, wo uf http://www.mustachianpost.com/de/ präsentiert wird.