TLDR: Given the pillar 2 assets at the start/end of the year and the interest rate, how is the actual amount of interest calculated?

I’m taking a closer look at my pillar 2 statements and I’m not understanding how the interest is calculated. I get that there are two parts (obligatory, over-obligatory) and that a % interest rate is decided for each part. I don’t understand what this % is applied to though (just the assets at the beginning of the year? An average over the whole year?) as the interest I am seeing is much lower than I would expect.

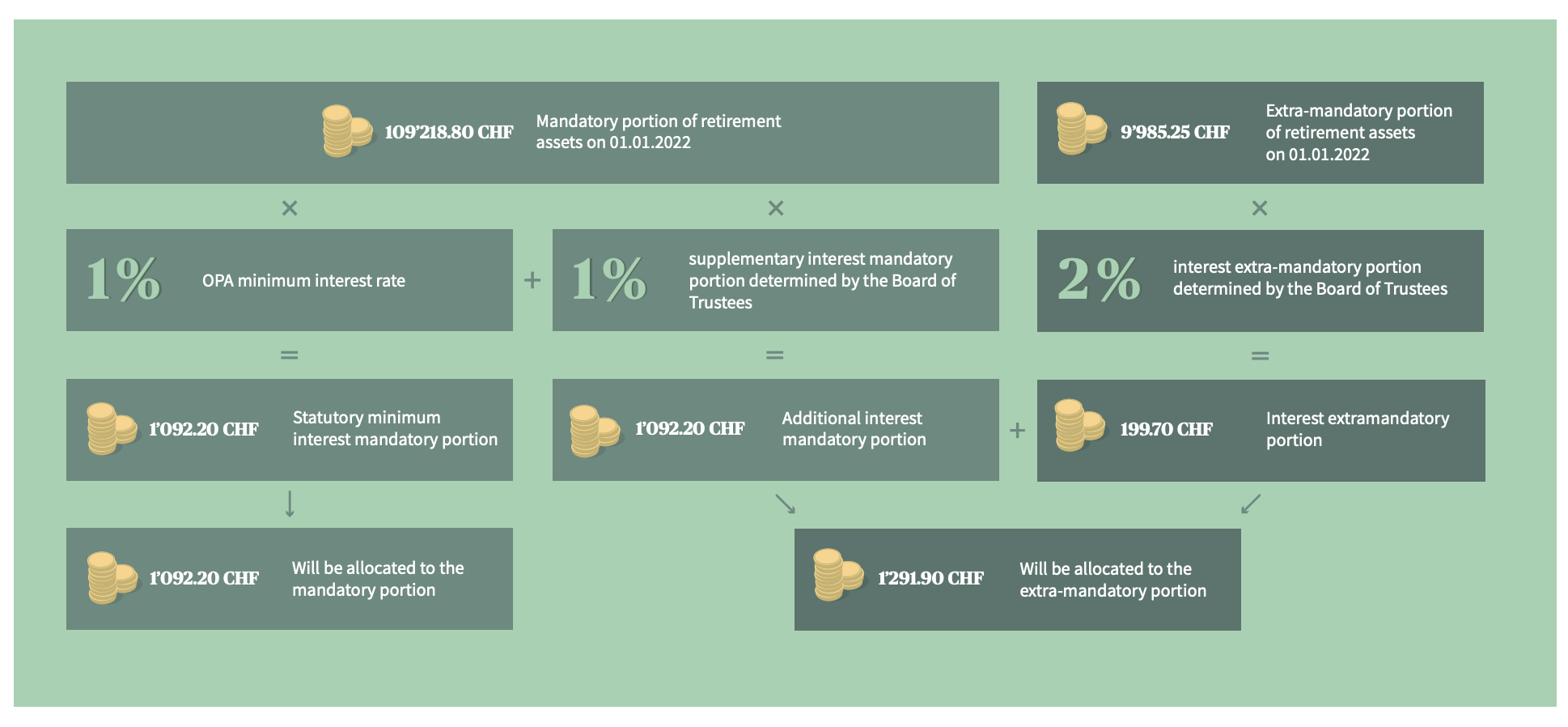

Example for obligatory part from 2022 statement from AXA (numbers changed but scaled consistently so %s still match)

Altersguthaben per 01.01.2021: 881.25

Zins 3%: 8.83

Altersgutschrift für 2021: 2133.00

Altersguthaben per 01.01.2022: 3023.08

To me this makes zero sense, I can’t think of a method of calculation that would lead to these numbers, other than that they both

only apply the interest to the balance at the start of the year, ignoring all that is paid in throughout the year

Thanks! That doc explained it, in particular this diagram. So in my case basically the mandatory-interest on the mandatory-assets is 1% but they give 3%, so 1% interest is fed back into the mandatory-assets while the left over 2% goes to the extra-mandatory-assets. That makes sense.

Any ideas what the rational is for applying the interest only to that present at the previous year end though?

I can imagine it helps the pension funds plan / gives stability, but seems also like it’s a subsidy of the old by the young / foreigners:

on the one hand, those nearing retirement who already have large pillar 2 assets relative to the amount they add each year get most of what they “should”,

on the other, people like me who are adding large amounts relative to the current pillar 2 assets get very little of what they “should”.

(where “should” means the setting in which you get the amounts pro-rated by the amount of time they were in the account over the year, like you do with normal bank accounts)

Follow up question: if you are going to do a pillar 2 buyback, is there ever any reason to do earlier in the year? The only thing I can think of is that maybe the 5-year-withdrawal-for-house-purchase rule would expire faster (but perhaps that is also done by calendar year and not the actual date it was made)?

Easier to calculate.

Also, the pension fund will regularly set its interest rates - but not in real time.

On the contrary, an older person will add more money to their old-age savings each year (that may remain without interest) than you.

The mandatory old-age savings contribution for a 60-year old is 18% of their insured salary - whereas for a young 30-year old (just assuming) like you, it’s only 7%.

What do you mean by buyback? Paying in additional funds or withdrawing for real estate or self-employment?

Buy in: In your case as late as possible because you won’t get any interest on the money until the following year. If your 2nd pays prorated interest it depends if you can get (1+marginal tax rate)% elsewhere.

Withdrawal: they pay you the prorated legal minimum of 1% on the compulsory part.

What makes a 2nd pillar generous, the % interest they offer (is that within the employer’s control?) or the amount the bank matches? Do you know what the range of conditions are? I have no idea what is possible

Contributions may be higher, interest rates, share of the employer etc. (though the pension fund will legally be its own structure though, so the employer can’t arbitrarily choose interest rates)

Many things are possible if only the legal minimum as are met.

I guess I’m asking for concrete numbers so that I have an idea what “bad” or “good” looks like.

My current employer pays a flat rate 8.5% of salary and bonus into my Pillar2 and last year it paid out 1% mandatory interest and 2% extra mandatory interest.

My last employer paid only 3.5% (I think that’s the minimum) and the bonus wasn’t included there.

Note: I work in tech and have a non-negligible amount of stock-based income but that is not part of the contributions as far as I know.

Is that good? Bad? Average? @Cortana what kind of situations can happen in your industry?

Keeping in mind that the minimum old-age savings contribution is 7% (25 and older employees), split at least evenly between employer and employee but also that old-age savings are not the only part of the mandatory second pillar, your employer should have paid more.

That risk insurance and admin expenses don’t come for free.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.