I’m quite amazed at the level of expertise and thought-provoking material to be found here! Coming from a background which is far from financially or business-oriented, I’m trying to “put order” in my investments. 3rd pillar is being “fixed”, thanks also to the advice I got here, but there is more than 3rd pillar.

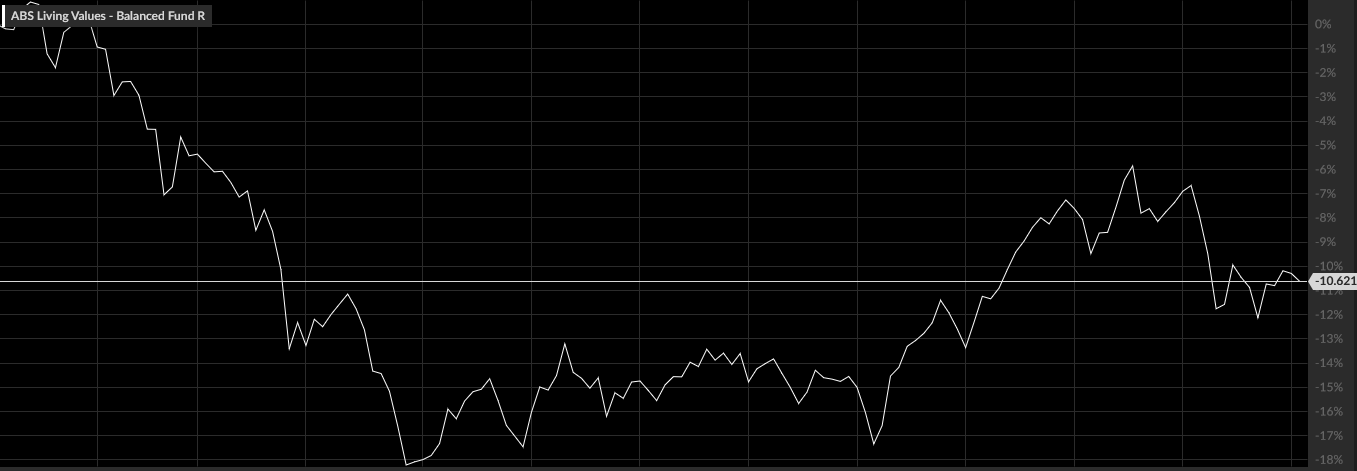

I have a relevant sum (ca. 30% of what I can put aside now middle to long term) invested in the “ABS living values fund” (CH0460045054) since August 2021 - very bad timing, the fund was at an all-time high and it quickly went down more than 10%… Now it moves around -10%. It’s an unusual fund, as heavily focused on sustainability parameters as it can get, actively managed (TER 1.50%, plus 0.30% deposit fee at the bank) with ca. 55% bonds, 35% equities and some “Liquidität”. What I like about it is that, if (big if) there is a logic in pursuing “sustainable” investing, this fund is targeting it with much stronger focus than the usual “ESG” (marketing-)products. But besides “sustainability”, what to do? To keep it long term and give it a chance to recover from the present loss, or sell it and invest differently, given the high TER and the not good past performance (also before I bought it)?

similar question about a similarly old, similarly sized investment in two similarly expensive active funds (in EUR) in a bank in the EU: in this case the returns have been positive (ca. +18% since summer 2021), but the tax situation there isn’t good (value increase is taxed at the moment you sell, and it’s hard to get back those taxes from Switzerland) - am I right in not seeing any reason for holding this investment any longer…?

It’s actually very simple… New knowledge makes clear to me how old decisions were just as good as the very little I knew about investing at the time. And exactly this pushes me to ask for advice before taking further steps, as my knowledge still needs to grow…!

I think for each of these investments you should neutrally look at it and think “would I buy into this fund today vs investing in something else”. It doesn’t matter whether it’s currently in minus or in plus.

Personally, I wouldn’t hold onto investments with such high fees, and from your sentiment I sense that you probably think similarly?

You had a thesis when you bought that fund. Is that thesis still valid? Are there events that have occurred that have allowed to test it and it has prevailed or failed? Is the amount of time you’ve held it enough to assert your thesis?

The fund provider obviously thought this fund could be marketed but do they also have a track record to warrant the high TER? Some fund managers can be worth it but many aren’t.

I wouldn’t have bought this fund and I would be selling it today but it isn’t my money. What matters is how you build your thought process about choosing your investments.

Whenever I make a new investment, I’d write down the reasons why I’m making it, what I am expecting out of it and, if I know them, potential events/behaviors that would get me to have to reassess that decision. Then I’d get back to that note whenever I’m questioning my investment and see if it still applies. If I end up doing many investments and most of them turn out to be duds that I want to get out of shortly (a few years) after having bought them, I’d resolve to a simple low cost passive strategy, using a broadly diversified index ETF.

I would also be very dubious about using past performance as a decision making or breaking metric: our investing time is limited, even if the performance ends up being consistent in the long run (which many active funds don’t manage to do), periods of disturbance can last for a huge chunk of our investing life.

After having watched the fund fact sheet (sorry, should have done it earlier):

This doesn’t strike me as an investment returns question but rather as an investment ethics one. The fund actively screens for companies they expect to be worth the money for the impact they have on the world, rather than pure financial returns. I’d use such funds if I considered myself an activist investor more interested on having my money impact the world in which I live rather than on bringing me actual returns.

I consider that a valid approach and plan on doing some of that in the future. I would consider that part of my portfolio more like a charity donation than a financial investment.

Edit: Then again, the fund has Microsoft as it’s third biggest position, with a note of 1 on their own sustainability scale. They seem to try to do both: screen for sustainability according to their own assessment and provide acceptable returns. That has signigicant chances to conflict with my own assessment of what companies are truly sustainable and I’m not sure I’d consider this fund for an ethics investment either.

In the US, at least, there is no official definition of ESG (environmental, social and governance) investing. If you advertise that you are an ESG fund and put all your money in coal stocks, the US Securities and Exchange Commission can’t stop you. […]

Sounds like a fund that insurances put into portfolios of marks that buy their indexed insurance solutions. Designed to be sold, not to be bought. ESG or not, there is no justification for this level of fees, and especially with this amount of fixed income. I don’t even want to think what kind of bonds they have.

My recommendation is to define your investment strategy, liquidate these positions and invest funds into your new portfolio. The longer you wait, worse it will be. And check out for “sunk cost fallacy” to put the label on what you experience and cope better with it.

OP touches on several topics

ESG: I get the idea, but am struggeling with any ESG definition and its intention. Microsoft, for example recently signed a deal to re-activate a de-commissioned NPP (3-Miles), to lower it’s CO2 footprint. Fine. Yet the funds explicitely excludes nuclear energy as against it’s ESG definition. Just one of many inconsistencies on any ESG investment.

It also excludes construction, traditional cars or chemistry. Fair enough. But if you want to actively influence companys sustainability, aren’t those the sectors where you could make the biggest impact?

Expensive mixed funds: I’d avoid expensive, active funds in general, but mixed ones (along with funds of funds) seem the worst. If you like a mix of equity and bonds, just do the mix yourself.

Past performance: Other have already said it, doesn’t matter.

You are, even if for somewhat different reasons. If your funds had a spectacular return purely out of luck due to the mix of companies, I’d still get rid of it

This is a very good observation. It will probably help to avoid performance chasing, since you recognize that decisions and outcomes are two separate things.

Usually, lateral changes (e.g. IMID → SPGM) in assets are less critical than changing strategies and asset classes.

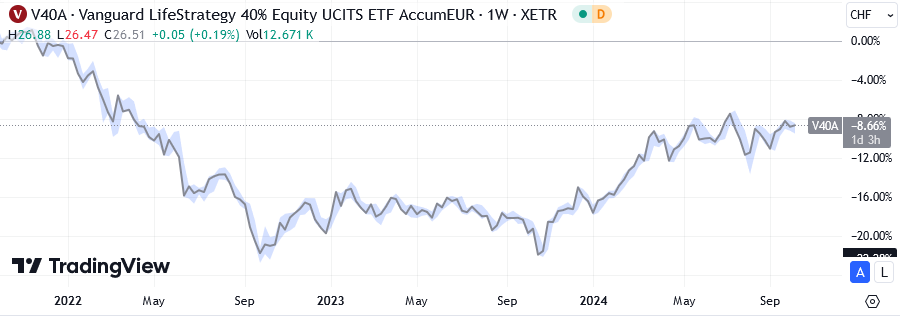

Comparing the returns of ABS Living Values - Balanced Fund R with, for example, Vanguard LifeStrategy 40% Equity UCITS ETF Accumulating (which holds a similar 40% equities and 60% bonds), we see similar total CHF returns for the last 3 years:

This should be switchable quickly. The certain 1.50% negative alpha (= the TER) of your fund gives you a massive margin of error.

Then you probably want to gradually change your asset class allocation over time (maybe 1y) to your desired target. So many bonds seem to be too conservative, but I don’t know what the rest of your portfolio looks like at the moment, nor do I know your goals.

If you want to do something ESG/good with your money, commit to donating the difference in performance to such causes.

Rather than looking it as investment, I would just focus on the current value of the fund. Let’s say it’s X

Now for the next 10 years. Where do you think is X going? Let’s say X* is expected value based on all the knowledge you have

And if you invest X in alternate investment, what’s the expected final value. Let’s say Y

If Y > X* , time to exit

If Y < X* , no point to sell

I have to say bond ETFs expected returns really depends on which bonds they actually hold. So it’s important to look into details of underlying instruments.

Although I think 1.5% TER makes it tough for them to do anything better than pure index funds with similar durations

Wow. I’m deeply impressed by the care and generosity put in each one of the comments and valuable suggestions this community is giving to a newcomer. Thank you!

Yes, I definitely messed up “investment” and “quasi-donation” at the time. But since some time I clearly see that for the “non rentable charity lending of money” there are much better options. Now I really think that anything related to “ethical investment” needs much closer ties with the desired outcome than such a fund or any fund with a label on it can have.

I’d say, lending money to an institution like Oikocredit, though for sure not “perfect”, makes much more sense than investing in any “ESG fund”, even if it’s a (in the marketing) “stricter” one like the one I bought at the time. Or for example a bank which eases access to credit to socially valuable businesses on a regional scale will have some measurable impact - positive in a structural or more “naive” way, but it’ll be possible to see what it is actually doing. Banca Etica in Italy has a network of small, but really nice projects to which they give credit (things like: high quality biscuits production in a prison - it changes the life of those people, eases reintegration in the society when they get out, and the products are very high quality…). The ABS fund… It’s just a big incoherent bubble.

But: it didn’t occur to me to compare the ABS fund (which is explicitly “without benchmark”…) to something similar as @Helix did! Thank you! In any case, it makes no sense to hold that amount of bonds for me now (maybe in 20 years, who knows), so it won’t even be just a lateral move…

Yes! There’s a new account on Interactive Brokers since one hour. Preparing the logical changes.

Totally agree. The problem with ESG and similar investments is that I cannot see what difference I’m making. Just because I buy a share with high ESG score, doesn’t really benefit the company. Furthermore, the ESG rating is subjective.

Providing capital to actually finance investments that do good for the environment is more debt / capital raises, which is more in the direction of private equity. Actually see private equity helping sustainable investment because they have more control and are involved in impactful decisions.

For me, if I want to do something good, I can help in the local community, donate to a charity (which has actual impact) or invest (e.g. insulation, solar etc.) in the house. All activities where I can measure / see my inpact.

Unfortunately, ESG and sustainable investments are just marketing terms to sell products. Having experienced this first hand at a financial institution who created such products.

It does benefit the company, as it raises the share price.

A high share price is very desirable for a company as it lowers its cost of capital for example. Makes it easy to finance new endeavours.

Makes attracting talent easier (also talent compensation with stock options).

It‘s really really good for companies to have high valuation.

Not advocating for ESG at all, I think it‘s articifial nonsense and companies cheat as much as they can to get high scores etc. (Due to the reason above)

Just wanted to point that out.

My own position is that if I want to truly support a company/a country/an economy, the way to do it is to buy bonds. Stocks also help a company get better financing conditions but do so in a lesser extent.

There is a market over all stocks or bonds. If you manage to raise the price of one, investors optimizing for return and risk will shift to the companies that are cheaper now. They will fill those holes like water. The effect of ESG will be severely diminished.

Buying large stakes in the worst offenders and forcing effective measures (low cost, high impact) seems more promising.

While a good ESG rating is certainly not negative, I would say that the operational / financial aspects have a significantly stronger impact on the share price. I just don’t see how an average investor can improve the sustainability profile of a company through sustainable investing. To impact a business you can: take control (large company stake required), provide capital to finance investments (debt) or become a shareholder activist.

Mostly things that can only be done with lots of capital or institutional setup.

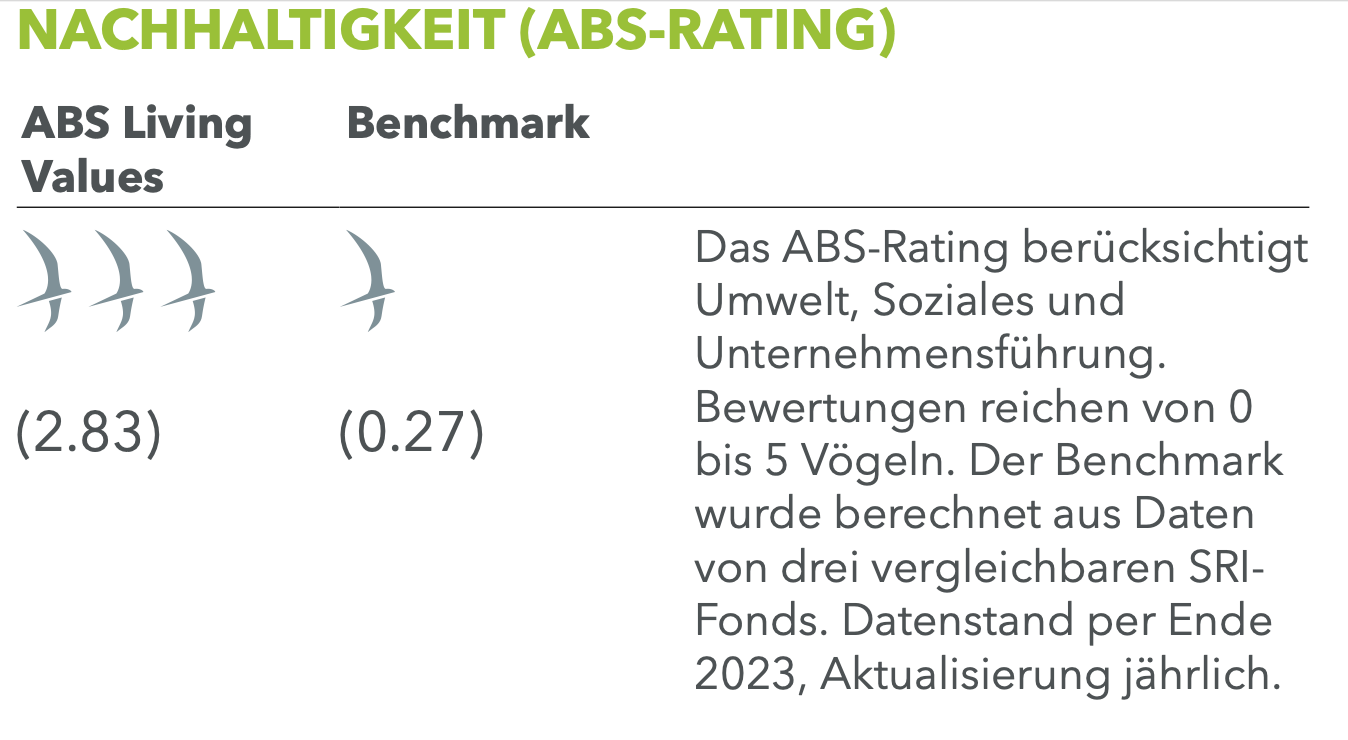

Who in their right mind uses “Vögel(n)” as a rating measure in their reporting … so many fun connotations in German, beyond just the main one people with associate with “the bird” in English …

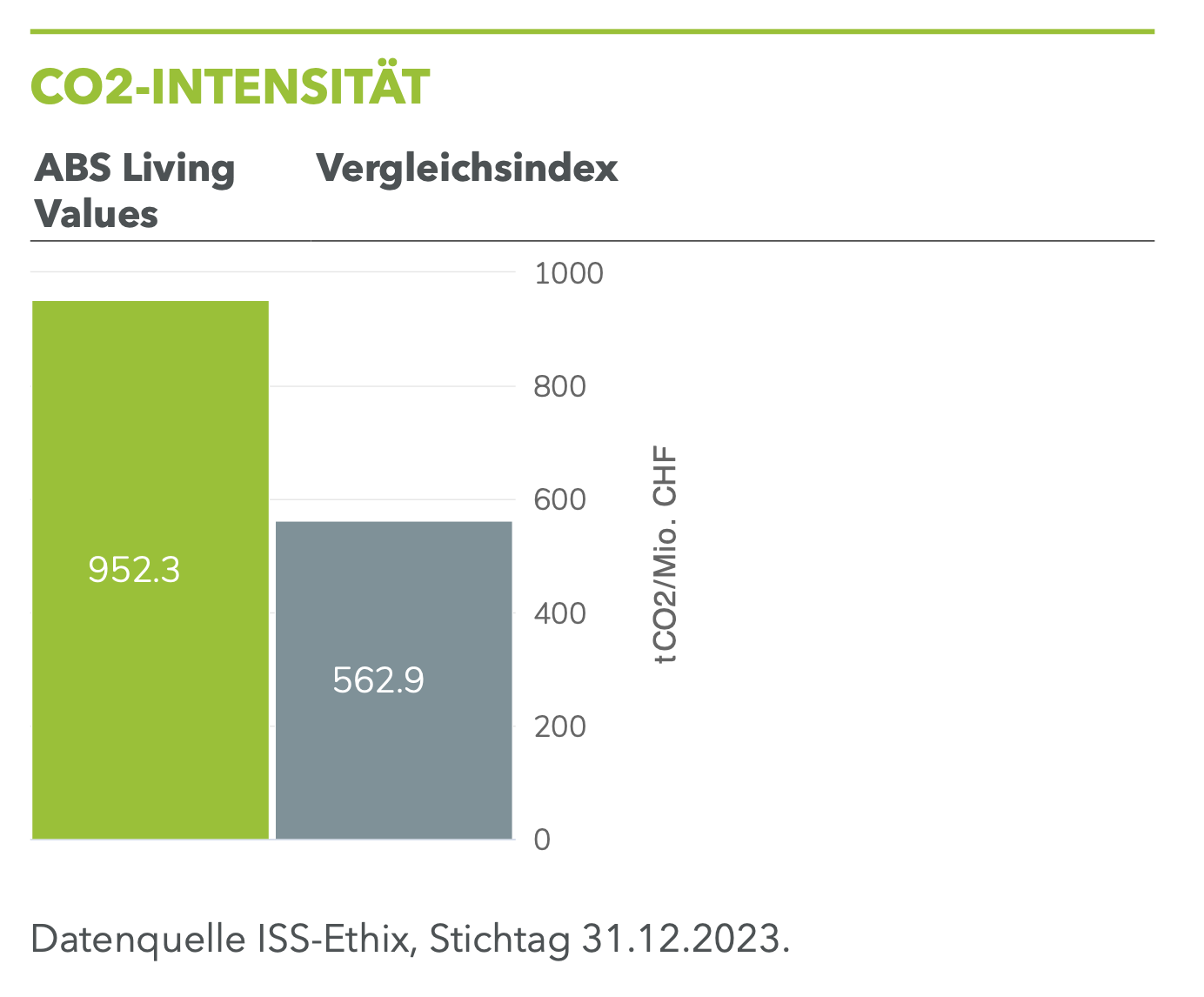

Also, they produce more CO2 per invested CHF than their benchmark?

One of their most sustainable (in the top 5) bond positions is CNP Assurances (French multi-line insurance company). The company has a Bloomberg ESG score of 3.63 (scale 0-10).

I could go on, but I’ll instead again just quote @Wolverine:

Seems OP @msci-li already made the right conclusions – good luck with your future investments!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.