Considering its implementation, maybe it should be called „with Neon“ instead of „in“. ![]()

That said, I‘ve used it and it works well enough, IMO.

Considering its implementation, maybe it should be called „with Neon“ instead of „in“. ![]()

That said, I‘ve used it and it works well enough, IMO.

Hi All,

I searched but not found this question already answered in other conversations ro recent, though please apologize if this is posted already somewhere, and kindly share where.

I’m currently looking for a “solid”, sistemic bank where to open a private and a saving account + 1 credit card in Switzerland. For Europe travels I use Revolut and if happens to be purchasing services abroad not accepted with Revolut I will accept the fact I’ll use the swiss credit card…

I am located in Ticino, therefore I am excluding ZKB and other cantonal banks.

I am oriented to either:

UBS me or UBS Key4

or

Reiffeisen

what’s the orientation of you wise people of the forum that may live in Switzerland since more time than me, or who have experienced multiple major banks than me?

Any “don’t go!” or excessive expenses, or limits?

my only experience so far was C.Suisse Bonviva pack earlier, now CSX pack.

thanks a lot for any suggestion

There are a lot of possible solutions:

Just some thoughts. @Dr.PI has posted some good links, have a look on there as well.

I think UBS is a good, multilingual bank and not too expensive. They even offer a basic free credit card - though other credit cards that are available separately may be a more attractive option.

A combination of Bank Cler’s Zak for your private account, and Bank Cler’s Savings Account Plus could be an option. Those are both favorable solutions, and it’s a bank with a countrywide presence. But Zak no longer includes a credit card.

Alternatively, you could use the banking bundle comparison on moneyland.ch, and select Ticino under “Providers with branches in:”

It is worth mentioning though, that while bank packages are convenient (having everything at one bank), you do pay for that convenience. Getting the best available credit card, private account, and savings account separately from different banks and issuers can be a better move, from a financial point of view. For example, there are credit cards which are better than Bank Cler’s.

Hi @Daniel,

I will check moneyland.ch thanks for the tip.

Regarding the approach of different issuers, what combination are you thinking of?

if later during 2023 I open an I.Broker account (which I am planning to do), would the private account be okay for -in and -out transfers -from and -to I.Broker?

thanks

This would be my recommendation:

It may seem like more hassles to use several different financial services providers, but in practice, it’s very simple, because you can automate everything with standing orders or direct debits.

If you are planning to open a brokerage account, then take a look at Yuh. It’s a good all-round solution for a bundled private account and brokerage account, both at solid banks (Postfinance and Swissquote respectively). It also comes with a payment card (Debit Mastercard) which has very favorable exchange rates and fees. The brokerage account is more at the beginner level, with franctional shares, and no options, futures, short-selling, registering shares, etc. so it depends what you need. But on the whole, Yuh gives good all around value for money.

Hi Daniel,

thanks for the extensive feedback.

Only one question open for me: I think I understand that Wise is equivalent of Revolut more or less. which I already have. Both Revolut and Wise don’t have a credit card with a given monthly limit. they are rather prepaid cards, dependent upon the amount available on the Revolut/Wise private account.

Is my understanding correct?

In case, I only miss to find the best credit card solution to pay in EUR or USD. Though consider that the monthly credit card bill I will still pay in CHF … not sure what could be the best option in my scenario.

…in other words: a debit card.

Wise‘s card is a debit card.

The lines between debit and prepaid can be very blurry, with some payment providers having issued quasi-debit cards that disguise as prepaid (e.g. Neon) or even credit cards. And prepaid card providers having released bank account-like functionality. That said, Wise‘s card is marked as a debit, not a prepaid card.

I just want to add some info here on that topic:

UBS 4 Key saving accounts typically offers a 0.1% on the savings account, but now it’s up to 0.6%.

Not sure if you can take only the saving accounts, but the whole UBS 4Key package it’s about 8CHF and it includes 1 debit card, 1 prepaid card, 1 personal account and 1 savings account. Also, first 6 months is for free.

Of course, comparing it to a bank with 0CHF fees, might not be worth.

Hope it was helpful

According to my quick calculations, comparing with YUH (free account, 0.5% interest), the savings interest minus the account fees are going to be higher than the interest from Yuh if the value of the savings account exceeds 96k CHF.

Just wanted to let you guys know: Neon’s offering 0.4% interest as of April 1, but only on money invested in “spaces”, not on your main account.

Honestly don’t know the reason for this separation of main account and “spaces” in terms of interest. Guess it’s got to do with daily withdrawal limits of 50k in “spaces”.

Also, they’re planning a savings account with higher interest and higher limits (currently 25k).

This. The more restricted the withdrawal the higher their own profit on it.

Your “main account” is a “space”. The only news here is that again they limit it to the first 25k.

For now. They plan to have a saving account soon.

let’s call an expert of languages here. ![]()

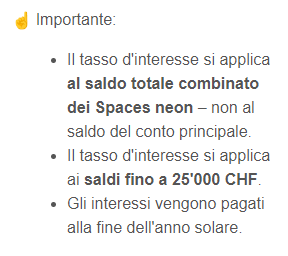

the “aber” in the german version is missing in the italian version.

Shall I start again my f#$# rant about how they threat the italian language? Isn’t here any lawyer available?

The italian text is maybe ambigous. It means that it’s not for the main account, but for the whole spaces accounts (of which your main account is part of). The second part “non al saldo del conto principale” is meant to highlight that it’s more than just the main account.

edit:

The normal interest is 0.15, whichi they say will be updated to 0.4. Since the interest is on the main account, i suppose the new one is as well. It seems the italian text is more correct than the german one.

According to FAQ, the 0.15% interest is not applied to the main account. And I think the statement matches in all 4 languages.

I agree with you, unfortunately.

So I see two issues:

-100 internet points for Neon. I’m so annoyed by this.

Yuh increases the CHF/EUR/USD interest rate to 0.75% p.a. on April 1st but only up to 25k (per currency I believe). The interest rate stays at 0.5% p.a. for cash in the range between 25k and 100k.

In contrast to Neon, Yuh applies the interest to the whole cash balance, main account and savings, as far as I can tell.

I see the following in the English PDF. Did they add this later?