Yes, Revolut is absolutely nice for withdrawal if you are just focusing this part. How often do you withdraw cash abroad? One time, five times, twenty times? How high is each withdrawal?

With Revolut you can withdraw five times for free and it is also capped at CHF 200 in total. Above that, you have 2%, whereas CHF 1 is the minimum per withdrawal. Revolut had increased their costs in the last periods.

Neon charges 1.5% - irrelevant how high the amount is. Neon did not increase the costs, yet, and this seems also to be their credo; a company which increases costs permanently (looks to PostFinance) is untrustworthy in the eyes of the clients.

Even if withdraw in total CHF 10’000 in the next years (with Revolut always CHF 200 per month) I have no problem to pay this commission to neon and I won’t go bankrupt because:

it is a Swiss insitution with a very solid Swiss bank in the background (no billions in C-level salaries or bonuses)

I have an own CH IBAN

I contribute to the Swiss economy and pay indirectly the salaries, which I have no problem with. Solid systems should be rewarded. Imagine someone is asking you to work for free…

finally a Swiss company which disrupts the massively expensive and intransparent market

Swiss law applies.

Take Wise as an example: they are not free and show you transparent the costs of their (very inexpensive) model. Such revenue is sustainable and they are generating cash. Despite Revolut is young, their cash burn rate is incredible (what I red couple of months ago).

As @CHRad says: the costs/rates are so close, even if you have a very high turnover, it nearly makes no difference. And from what I read in this forum, no one is living at the existential minimum

Really happy to hear that I am not alone with that. And I can confirm both things, they are annoyingly woke and have a good customer service. The first ad I saw for them was when they ran a sign-up bonus. Don’t recall the precise sums, but it was something like 10 CHF for men and 30 CHF for women. Obviously sexist. When I complained to them, I got a personal reply, not some generic email template.

Only reason why I stick with them: It’s the only Swiss offer with cheap foreign transaction costs / low spreads. But I do consider switching to Wise. They are a bit more expensive, no deposit insurance, but they offer EUR accounts and I use them anyway for cross-border transfers. I would not consider Revolut, I have heard too many scare stories about unjustifiably frozen accounts and horrendously bad customer service.

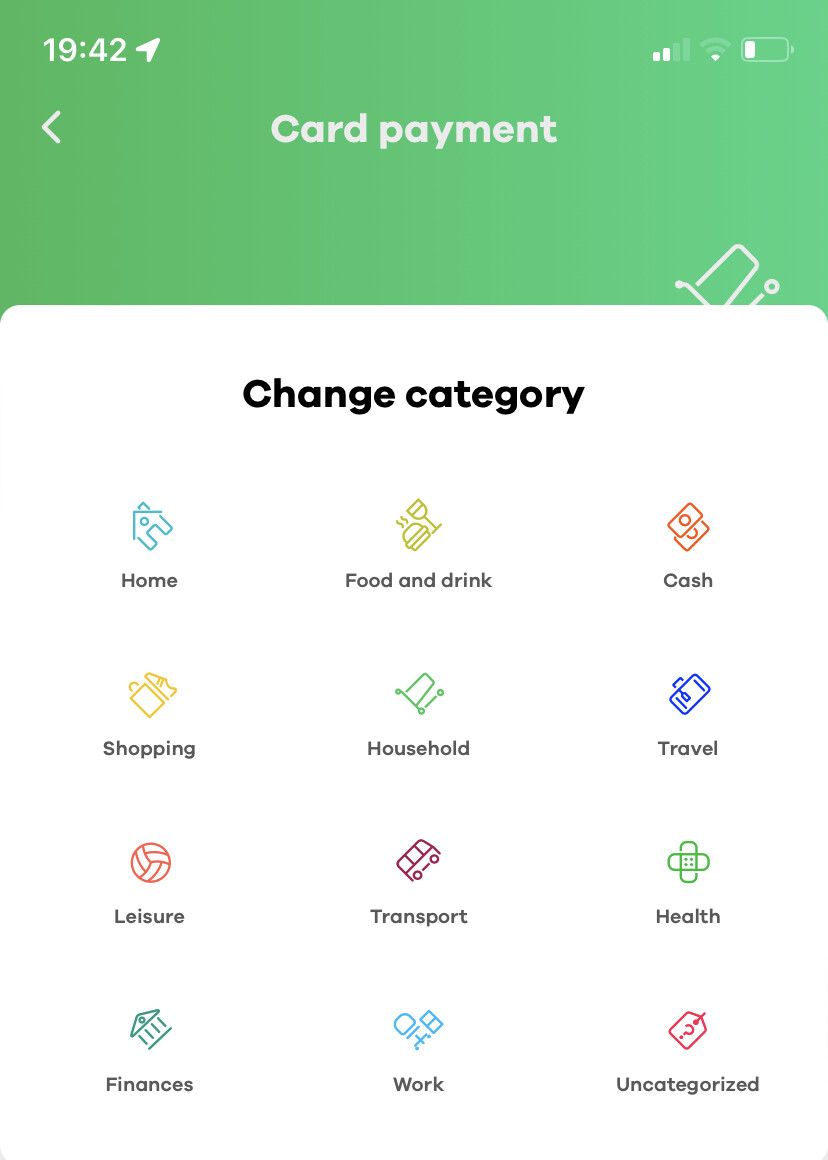

One more thing that bugs me with Neon is their categorization engine being super simple.

Where do I put my childcare expenses (e.g. Kita)? → Household

Where do I put my Food expenses (Coop/ALDI)? → Household

Where do I put my cleaner’s fees (quitt)? → Household

Basically as it stands today, 75% of our spend is the category “Household”, which kinda defeats the purpose.

At least you can download the data in CSV, that’s good.

I guess “food and drink” is what you define it. Personally, groceries is much closer to “food and drink” than the “household” category. Alternatively, you could use a category you barely use (e.g. work category) for the grocery stuff.

I know that the categorization in neon is not perfect, but considering it’s a free bank account with very favorable exchange rates: I’m really happy with it. They also introduced “spaces” not too long ago, a feature I was hoping for. So maybe they will soon also introduce the feature to create your own categories as well.

And in the end: the categorization is nice to have. Most of us here in this forum don’t have a huge problem when it comes to expenses, otherwise we wouldn’t be here. I know very well in which areas I could still save more, when life gets hard. So it’s more of a “nice to have” than an absolute necessity, at least for me.

One additional nuance - TWINT only goes via the UBS TWINT app, and there’s fix monthly limits on top

spend monthy 500CHF / yearly 5000 CHF

receive monthly 1000CHF / yearly 5000 CHF

Changing this would require to open a bank account - with UBS.

Also I’m getting other nuances

sometimes the card just goes into Declined via Apple Pay. Happened already about 5 times in the last 3 months

the web interface is really missing

the categories they give you are semi-useless for a “household” account

I have a running log of transaction entries, but it doesn’t show what my balance was at each of them, making it hard to figure out a monthly required balance

I have to tell I’m trying to stick to Neon but it’s getting inconvenient at more places than I’d like. I’ll probably degrade them to to a “travel and overseas purchasing” card, which is should’ve been in the first place.

Which other banks can you recommend on a “household shared account” principle?

Shall I just go to UBS and assume the costs?

CSX would be an option, but CS is … just no.

BCV was free as well last I checked, if you keep a certain amount with them (10k, 15k?). Credit Agricole as well, but not anymore.

Otherwise CSX would be my go-to full-service free account. Neon is my foreign-transaction credit card, I don’t use or need the attached account. CS has a sh*t reputation right now, but I really dislike Neon’s woke agenda, so I’d rather go with CS than Neon. Different people, different preferences…

ZAK would be another alternative for a free account with decent foreign-exchange costs, but also no native Twint.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.