That “einmalig” is weird. Of course when you order you pay once.

Somewhere else I saw the “First Card” costs of 20chf for the printing of the card.

That “einmalig” is weird. Of course when you order you pay once.

Somewhere else I saw the “First Card” costs of 20chf for the printing of the card.

But you can also select one of their other cards for free through can’t you? Isn’t it just the colour of the card that changes?

In theory, you can change plans monthly and in some plans the replacement card will be free.

So the thought did cross my mind that maybe it’s cheaper to switch plans for a month just for the free replacement card ![]()

But I couldn’t find out anywhere whether you could keep the higher-plan card when downgrading, so just coughing up 10 CHF seemed like the safest option to me.

I only use Neon with Apple Pay. I’m curious to see if Apple Pay will continue to work after the card expires. As far as I know, however, this is linked, as Neon does not support virtual cards.

The others in the list are more expensive.

Never had a card that I had to pay for when it expired. Bothers me, not so much 10.- every few years, but that they still have their website as neon-free and not even this is free.

Sorry to crash the party, but try out Yuh-Free.

Ah wait, there is no Yuh-Free as all packages of Yuh are free*. ![]()

*Yes, I know, forex at Yuh is worse than Neon, but for the basic bank account + card, I only see advantages. I was on the brink between Neon & Yuh a while back before opening an account, but since then the balance tipped more and more towards Yuh.

Multi-currency on same IBAN at Yuh is great and practical as well, especially since you can spend them from the debit card (à la Revolut). Use IBKR for fx once in a while if you want to optimize fees.

As a free package, debit card, twint, bill, Apple Pay, multi currency, it’s great.

Invest, saving plans & 3a are worth a look if you want to shrink everything down in terms of providers. It’s a free mobile-only swissquote for dummies.

Also, it is great to have a low cost low fee for fx, but if you are planning your fx operations in advance, you may as well gain/lose from market timing. Especially nowadays when currency vol is pretty high.

And if you spend once in a while some small amounts abroad directly from chf account and want the least overhead possible when fx occurs, it’s not like a few bips will be the end of the world.

Then there’s the case where there are huge amounts and you don’t want to/can’t plan and just want to save on fees when it occurs.

So I sent them an email. Yes, they will charge 10chf for an expiring card on the free plan. New cards are good for four years, so it’s 2.50chf per year.

I use Neon exclusively for their Mastercard for payments abroad. I brief check of their competitors suggests that they’re still competitive there. Though I’m not happy to see them add fees without telling their customers in advance or even updating their price list.

What if you don’t? It looks like you can order the new one, but you don’t have to.

I have an inactive neon-free account, just keeping it in case something interesting pops up.

I arranged my cash-flow with bills/ebills/recurring orders paid from my salary every month, rest is invested to reach exactly 0, and daily expenses paid on credit card (so that’s a bill for next month).

So I don’t have any use for debit cards, except large fx expenses which is very occasional.

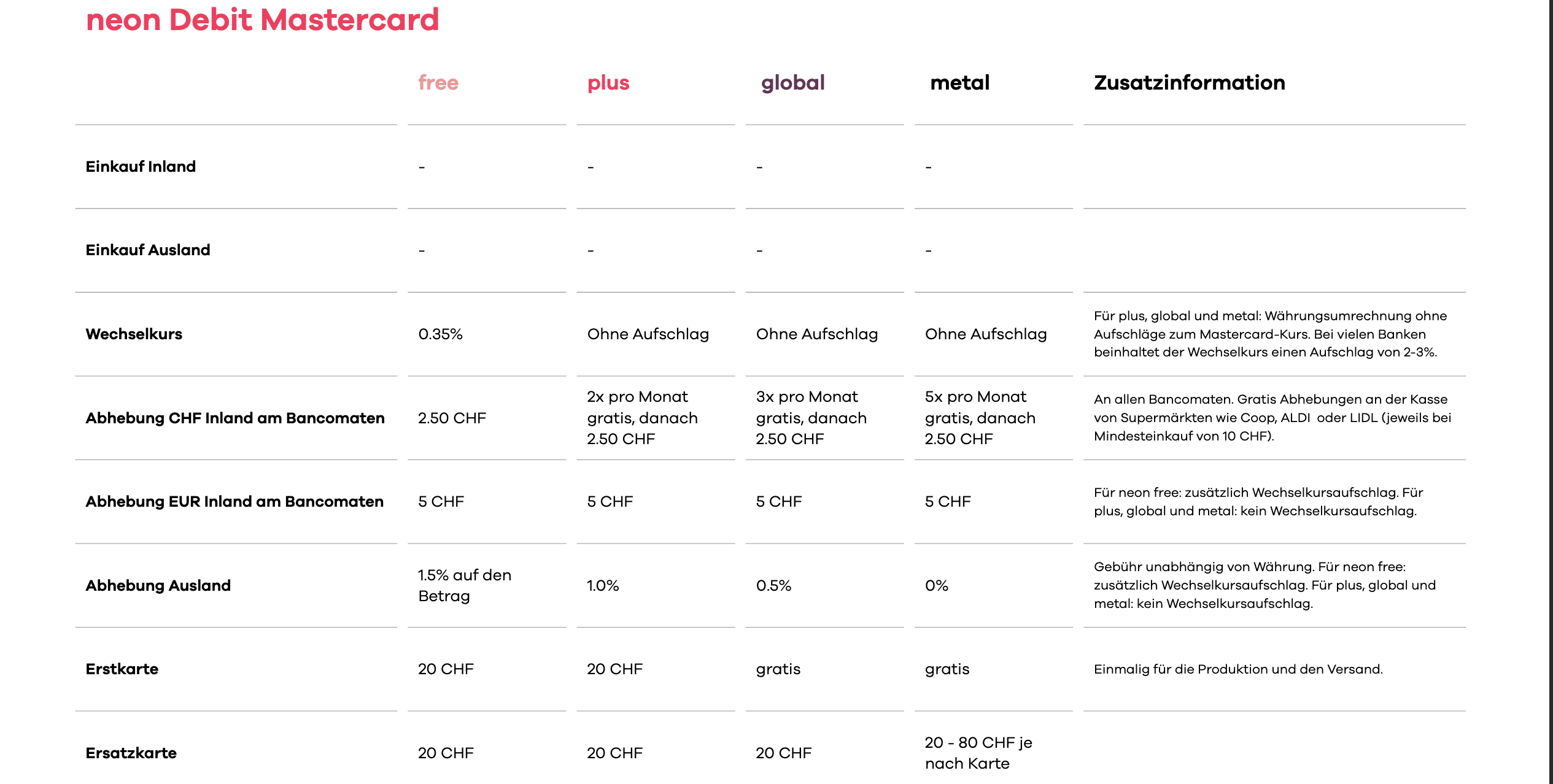

The pricelist of Neon does not seem updated yet. It still says: “Einmalig für die Produktion und den Versand.”

If you don’t order a card, you will only be able to do bank transfers etc but not card paiments (shops, restaurants).

And for the suggestion to switch to yuh…

If there are swiss bankers on this forum, listen:

I don’t want my bank account to become like my mobile phone subscription, where I feel bad thinking about it, because I know younger me would have switched, but older me doesn’t want to invest the time every few years to re-setup everything.

Does Neon also offer virtual cards?

It seems this is becoming the new standard. Banks are moving away from physical cards to cut costs, since virtual cards are essentially free compared to producing and managing plastic ones.

I stopped using Neon a while ago to simplify my setup, but it feels like the company is betting on survival and hoping for a takeover by another bank. The app itself was solid.

Source?

Yes, they haven’t updated the price list. Which is, for me, the worst about this. I don’t really mind paying 10chf every four years, if the entire package is still good for me. But please tell me in advance and be transparent about it!

Which is quite difficult. The customers are all with Hypothekarbank Lenzburg. Neon uses their Finstar Banking System. I wonder whether Neon can even be taken over seriously. The acquiring bank would also have to become dependent on Hypothekarbank Lenzburg or migrate all customers (new IBAN, etc.). I don’t think the app has any value without Finestar Service.

But that’s just speculation, I’m not in that industry.

This is strictly my impression. It feels as though the company is focused on survival and possibly positioning itself for a takeover. I’m not presenting this as a fact, but rather sharing how the situation comes across to me.

That’s a fair observation from a technology standpoint. However, in an acquisition, the customer base and the technology stack are two distinct layers. The infrastructure can be replaced or integrated, while the customer base can be transferred or migrated. The dependency on Hypothekarbank Lenzburg adds operational complexity, but it doesn’t diminish the acquisition potential.

For a bank considering an acquisition, the key question is whether the expected return on the transferred customer base justifies the investment and the migration effort. Maybe yes, maybe not ![]() .

.

I am happy to have closed my Neon account and moved to ZKB.

This is how it starts, first a forex conversion fee, than you pay for your card, then you pay for your account. I don’t understand what is the value proposition that Neon is trying to do

agree… moved to WIR and happy.

Even with the SBB error (@#$!!) , the Fx fee and the card fee (weird that it lasts only 4 year btw), I’m still happier than with Alpian (which btw did upgrade (imho) their UI). But I’m biased because of my Alpian accident (didn’t order the card in time).

But at the end it all depends how you use it. Mine is a Revolut/PF backup.