Mastercard…

Aaand they just added an exchange fee:

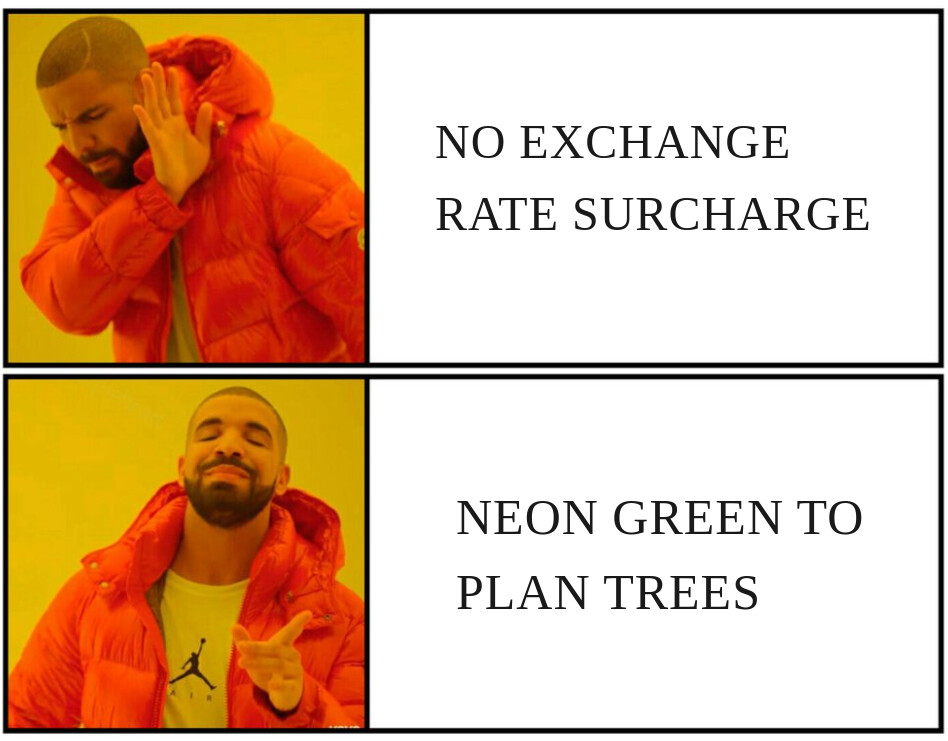

What will change for you?

As a neon free user, here’s what you can expect with the roll-out beginning on 13 May 2025 and continuing over the following days:

- Stay commitment-free: neon free will remain 0 CHF / month, 0 CHF / year. No base fee on the account or card.

- Keep your core features: continue to enjoy the key features that make managing your daily finances easy, including your neon free card, payment services (eBill, QR bills), Spaces, invest (with the same low-fee structure), email support, 24/7 card emergency support, and more.

- New pricing conditions: As card costs have risen for fintechs like us, we will apply a 0.35% exchange rate surcharge for card payments abroad (e.g., 0.70 CHF on a 200 CHF payment). In Switzerland, ATM withdrawals will now cost 2.50 CHF from the first withdrawal, unless you follow our tips to do it for free at Coop, Lidl and via Sonect, or for a low fee via Twint at many kiosks or supermarkets. We know that any fee is one too many. But we’re still far from the fine print conditions of traditional banks or even from other main neobanks’ pricing. We’ll keep pushing for the lowest fees possible with neon free. And, of course, for full transparency.

- More choice and flexibility: You’ll also be able to further tailor your neon experience: add the neon green extension and plant trees as you spend, or select another plan more aligned to your needs in a few clicks.

6 Likes

Blockquote[quote=“logitacher, post:399, topic:3150, full:true”]

- New pricing conditions: As card costs have risen for fintechs like us, we will apply a 0.35% exchange rate surcharge for card payments abroad (e.g., 0.70 CHF on a 200 CHF payment).

[/quote]

Well, I guess now it’s a waiting game until the likes of Alpian and Radicant will follow. Will slowly but surely make Wise or Revolut more competitive again (or even the likes of ZKB with a capped fee for large amounts)

4 Likes

Oh well. It was fun while it lasted.

6 Likes

Source? I’ve seen surcharges > 1% on their site.

WIR has still interbank rates w/o surcharge.

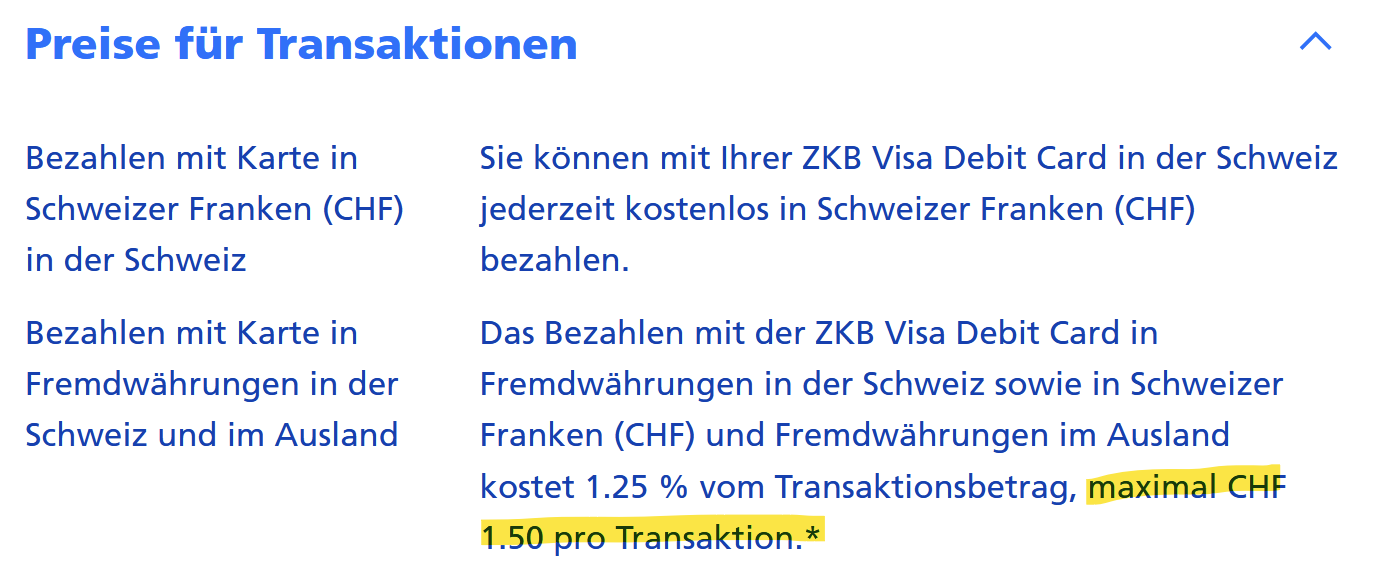

In German only unfortunately, but it’s basically 1.25% up to a cap of 1.50 CHF. So bad for small transaction, but ok for large ones. When I experimented the FX rates were better than all neon, Revolut and wise and on par with radicant.

2 Likes

Often they have a spread in addition to the fee, is that the case here?

Will quote myself:

Blockquote When I experimented the FX rates were better than all neon, Revolut and wise and on par with radicant.

I ran a number of test transaction at multiple points during 2024 (buying gift cards in EUR) with all those at the same time during the week. Conclusion was that radicant and ZKB pretty much used a rate that was equal to the IBRK rate at that time. Revolut, neon and wise (excl. fees) with a small markup.

But of course this is me just testing at 2-3 random times in the year with results varying a bit, but generally showing the same trend, meaning excluding fees neither had a large markup.

2 Likes

Still cheap for what it is IMHO so this isn’t going to make me switch.

However, they do need to get their act together when it comes to app access. I’ve been having to re-enter my credentials as if I had just downloaded the app for the first time every other day (or so) recently, and after that it was often still impossible to log in ![]()

1 Like

Until radicant offering changes, I don’t see any reason to use neon as a main free banking account anymore (I don’t talk about an investing offering).

- Exchange fees? Radicant wins

- Withdrawals? Radicant wins

unless you do it so often that neon integration with Sonect makes a difference

- E-bill integration? Radicant wins

- Interest? Radicant wins

- Additional EUR account? Radicant wins

- International transfers? Neither wins, just use Wise directly

1 Like

Wasn’t Radicant risking bankrupcy?

Also if Neon keeps screwing up with the “SBB” blunder, I might switch as well. I was almost an Alpian fan until my laziness ruined me.

Would be interesting to see the data, if you happen to have them in some tabular format (anonymized of course).

Sounds like something moneyland do in their comparison blog posts.

Good to know, since ZKB is capped might be a good option for pricey items.

As Adele said:

“This is the end

Hold your breath and count to ten”

So long neon you were fun and useful the time you last ![]()

Neon has a nicer Investment part than Alpian I believe. I didn’t see any review of Alpian or Radicant

I’m using IBKR so I don’t mind, but sure it could be a strong argument ![]()

0.35% is still quite cheap compared to the big banks. I need to look up my foreign purchases from last year to get a sense of the actual impact of this change.

5 Likes

UBS key4 debit card has Mastercard rate +0.5%. So UBS’ entry package is pretty much comparable to neon now.