I’d appreciate your help on my proposed equity portfolio. I am a conservative investor and have enough security by other portfolios and real estate. My goal with this Portfolio is long-term (20+ year) growth through global diversification and exposure to historically-proven factors (small, value, momentum, profitability). I’m trying to balance these tilts without taking on unnecessary, uncompensated risk.

Strategy:

· DCA: I contribute a fixed amount monthly. · Rebalancing: I rebalance individual ETFs only if their allocation drifts beyond a 5% absolute threshold (e.g., if my 25% allocation hits 30% or drops to 20%). · No Market Timing: I stick to the plan regardless of market conditions. This is my strength, I stick to even very bad ideas forever like a nerd.

My Portfolio:

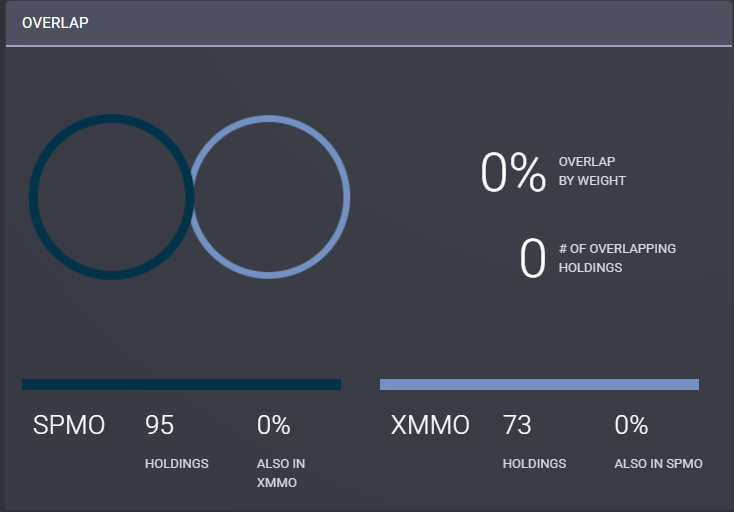

AVUV 25% US Small Cap Value / SPMO 20% US Large Cap Momentum / IDMO 20% Int’l Dev. Momentum / AVDV 15% Int’l Dev. Small Cap Value / XMMO 10% US Mid Cap Momentum / AVES 10% Emerging Markets Value

You will still do it for US ETFs, which are also US-domiciled securities, no matter what they hold inside. The layer 1 withholding tax from the domicile of ETF’s holdings to the ETF will be lost, but it would be the case also for IE ETFs.

Can you maybe explain how those two things go together?

I’m sure you are aware, that SCV is generally more risky than LCB. At least that’s the reason for the potentially higher “premium”.

I bet you have your reasons for every part of the portfolio? What are those?

It will be much easier to say whether the allocation makes sense.

What I meant by conservative is that I have already a nest egg, and my early retirement is secured whenever I would want do.

Now I have the luxury to take on more risk to enhance my returns, while not having any sleepless nights about it if it would fail. Still, my conservative nature does not allow single stock picking, crypto or volatility pumping or whatever the younger generation would enjoy. I want to take on more risk, but not burn money.

I read about factor investing since a decade and spent tons of time performing historic factor analysis and simulations. This portfolio was one of three outcome s of that time, aiming for distinct exposure to the HISTORICALLY four most profitable factor premia. However, good and cheap ETFs were not previously available.

I checked my sector exposure and that also looked nicely balanced, but clearly not like my regular MCW portfolio.

What I forgot to mention was the reason for deviating from MCW ratios between regions.

I overweigh developed international markets because their higher cyclically-adjusted earnings yields offer a better value proposition than the more expensive U.S. market. This positions my portfolio hopefully to benefit from the potential long-term reversion to the mean of this valuation gap.

Looking at MCW like VT, you underweight the US (55% vs. 63.5%), which is OK to me.

It’s quite obvious, that this portfolio is going to deviate from VT performance. But since that is what you’re looking for, I can definitely see, why you would put it together this way.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.