Sure, the risk parity concept implies the goal of perpetual withdrawal rates. Basically a mini individual financial endowment.

1 Like

And if you want an advanced deep dive into risk parity concepts, listen to these guys:

Yeah, just recalled that thread, might have been repeating myself ![]()

Basically yes, still a great fan of the golden butterfly, because it provides great diversification, SORR mitigation and decent returns.

Of course, you could add some advanced fancy stuff such as trend-following managed futures funds, market-neutral, global macro, carry, long vol etc., but they’re expensive and maybe just not worth it (can’t get insurance against everything ![]() )

)

Or you can split your equity portfolio allocation into equal weight factors such as value, momentum, low vol, MCW. But the more I read about factor investing, the more I come to the conclusion that it’s just a zero sum game

4 Likes

Yes, gold, although not the sexiest asset in town, has been a great diversifier to increase total portfolio Sharpe, uncorrelated to most other assets ![]() And I’m quite impressed by the fact that it has maintained its purchasing power for millennia.

And I’m quite impressed by the fact that it has maintained its purchasing power for millennia.

1 Like

Choosing bonds makes my head spin. With regards to risk management / diversification, would it be wise to hold some international CHF-hedged bonds?

Or even international unhedged bonds?

Thinking of a worst case scenario here: Switzerland defaulting, being invaded, or a real bad natural catastrophe. It is, after all, just a really tiny place on earth.

1 Like

My take on this is that the best line of defense is family/close friends living in another country not subjected to the same risk, or unlikely to be hit by the same risk at the same time.

Otherwise, I tend to adopt a policy based on the level of the assets I want to protect:

-

with a low amount of assets, it isn’t worth it to try to protect them too much, what I aim for is growth.

-

with more assets, I might want to protect some of it from some kinds of losses. Broad based investment grade bonds hedged in CHF would diversify my exposure to defaults while keeping my investment tied to the currency in which I plan to do my expenses.

-

if at some point, for some reason, I assess it would be worth it to protect against catastrophic risks, then I’d put some of my assets in various categories of assets like:

.

small denominated CHF bills (10 CHF) in case of blackout, when no credit card/phone payment could be processed.

.

small denominated EUR bills, in case I need to go crossborder by my own means.

.

real assets, like food, warm clothes, useful various wares, easily transportable and tradable amounts of gold and the like.

.

A basket of currencies, which would best be kept in a broadly diversified basket of unhedged foreign bonds, in which case, I don’t care about their returns or market volatility tempering ability, I would just take them for the off chance that some of them might help me enough to make a difference when everybody is struggling as things are going very, south locally.

In short, my basic take is “know what you are trying to achieve and then find the best way to get that”. Most often, “relationships” is the best answer I can find to survivalism questions.

2 Likes

Imho, why not at least try to get some easy diversification for 25% of your portfolio if you can (to me, 25% is not exactly nothing ![]() )?

)?

I’m wondering how that might look like, maybe a third of

- CH-bonds

- US-bonds (IEF)

- unhedged ex-US intl. bonds (IGOV)?

1 Like

Sure, you’d have to have a close look at that.

Last I compared them, intl. bond fund returns seemed not to be significantly different, at least in the long run. So some international diversification makes sense to me, kind of a free diversification lunch. Just not sure yet as to how exactly I’d implement this.

1 Like

See first part of the thread for the discussion. Or the whole thread ![]()

3 Likes

The specific point is that corporate bonds in general and CHCORP in particular behave like a mixture of stocks and “real” fixed income instruments: government bonds, fixed term cash deposits, savings accounts. So it doesn’t deserve a dedicated allocation and it’s yield can be reproduced by other instruments.

Unless you want to capture the tax-free yield in form of bonds valuation being below par, which is a next level of cunning. ![]()

P.S. oh I haven’t noticed first. You miss UK stocks with juicy dividends free of L1 withholding tax. And Australian stocks, also no L1 tax. Also no Japan, which might have it come back.

And I would never put that much Switzerland, but this is your personal choice.

3 Likes

Consult with an independant financial advisor.*

The community here is great, but personally I would not crowd-source proof-check my FIRE investment strategy without a pro taking a look and them independently approving.

* Not a bank or financial advisor associated with a bank or similar.

2 Likes

As with everything in life in the end everyone cooks with water (does this phrasing exist in english?).

2 Likes

Fair, wealth managers are pros.

They might be pros at at managing money, but …

… from my personal insights of currently working myself at an asset management company with many billions under management, I would claim they’re even better pros at something different: selling you their products / funds / ETFs.

The explanation is quite simple, actually. As always, it’s all about the incentives: they earn fees on assets under their management which determines their company’s income and ultimately determines the advisor’s raise and/or bonus.

Thus, ideally, you (their customer) buy their products; in the worst case, they sell you competitor products and garner a kick-back from the competitor for that. Even if they don’t have any products of their own, they might still aim for selling the 3rd party products with the largest kick-backs to themselves.

These incentives explain why they’ll propose to you solutions that are optimized for their return instead of yours. IMO this is why some of their proposals might look a bit funky to someone with a slightly above basic financial background.

I didn’t do a lot of research, but at the time (couple of years ago) I only came across one independent advisor near me that offers wealth management, doesn’t have their own products, and re-imburses kick-backs of 3rd party products they purchase for you.

I consulted with them and paid dear money for that (mostly on financial planning, less on wealth management). I honestly don’t think you’ll get independent advice without paying for it.

Going back to the start of this question: you probably are better off by asking this forum about your target portfolio rather than one of those not-sure-how-exactly incentivized wealth managers.

(I’d personally still go to a truly independent advisor with the limited knowledge I had a few years ago. These days I feel comfortable enough making these decisions myself - famous last words … ;-).

8 Likes

Why quiet? Thanks for your contributions!

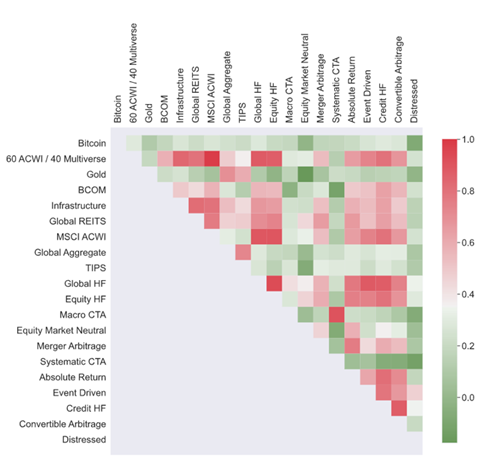

I’d very much recommend this podcast. Traditional stock/bond only portfolios are a thing of the past imo, because historically, they have been largely correlated.

Whether you own small/large, US only/global, REITs, private equity, corp bonds etc.: It’s basically all highly correlated and therefore, highly risky

")

3 Likes

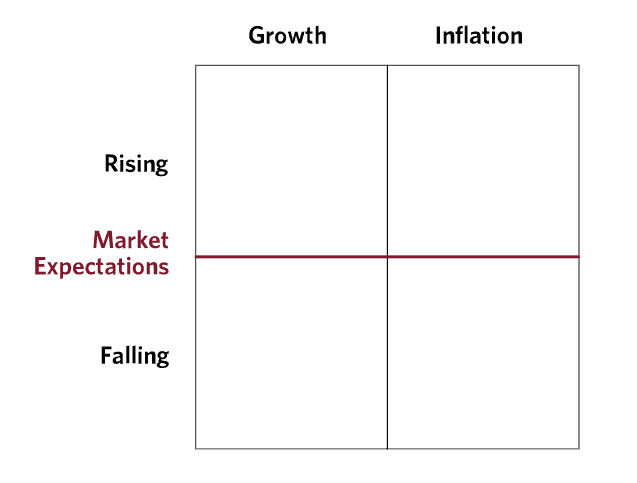

It’s worth listening to. In short: Stock/bond portfolios suffer from recency bias due to the bond bull market (falling rates) since the 80ies. Bonds can yield negative real returns for decades. More often than not in history, stocks and bonds have been positively correlated, not negatively (bonds providing bo downside protection). Stock/bond portfolios perform poorly in stagflationary periods. Hence, the goal is to construct a portfolio that can cope with all four market environments: rising/falling growth, rising/falling inflation.

Here’s some further food for thought, explains it better than I ever could ![]()

3 Likes

Depends on your net worth. If you’ve got significantly more than 25x of your annual expenses, your sequence of returns risk (risk of portfolio crash shortly after retirement, getting you on a long-tern low return path) is pretty small. So I think you should be fine with as little as 10% non long-only stock/bond assets. Cheapest would probably be gold or commodities. Personally, I’ve come to like pure trend strategies due to their ability to go long or short on bonds, commodities and currencies. This makes them less path-dependent and able to opportunistically profit from both favourable and unfavourable market environments. They basically open up a second dimension to classic long-only investing: shorting. Disadvantage: It’s a relatively niche strategy with high costs. People don’t like it, because it can underperform for years (lots of small pain, then possibly big gains, aka positive skewness or right tail).

You could have a look at the SG trend index to check if you like the results. Important: Don’t look at the performance of trend alone, but how it enhances performance of your total portfolio (avoid line-item thinking). What matters is total portfolio CAGR and/or Sharpe, not single asset CAGR/Sharpe. Also: There’s a nice rebalancing premium to be gained in a total portfolio context, which does not show up when looking at single-asset performance.

2 Likes

You can’t directly invest in an index, but there are some relatively new ETFs you could have a look at: KMLM, DBMF and CTA. I prefer KMLM because it’s based on a passive index that’s been around since the 80ies. Also, it does not contain equities, which makes it a better diversifier to your long equity allocation.

For backtests with Portfolio Visualizer, you might want to use some of the long-standing (and more expensive) trend mutual funds, such as AMFAX, MFTFX etc.

2 Likes

I want to begin by thanking you for the information provided. Now on to more critical words:

They seem to be hard selling CTA Trend strategies. Especially the hypothetical All-Terain graph at the end - smooth as a baby’s bottom and with a CAGR double of 60/40 - reeks. They don’t happen to sell such products?

I don’t claim I understand what is happening here. I saw that AMFAX had high returns where stocks had losses and okeyish CAGR. MFTFX had bad CAGR.

It is important to note that producing uncorrelation or anti-correlation with stocks is not hard (just use cash or buy an inverse S&P500 etf). Doing so whilst having good returns is. So good that you can beat other portfolios in returns and risk (potentially by using some leverage).

Diversification for diversifications sake doesn’t bring much to the table. Tail risks that bring the MSCI World to zero should be hedged with ammunition. For everything else focusing too much on reducing risk destroys return. You can stomach bad years if the good years make it worth the wait.

They also provide monthly index data from 1988. (link to FAQ) ![]()

I didn’t have time to analyze it, but if someone wants to make some pretty graphs with comparison to other asset classes…

As far as I understood returns are generated by absorbing the price risks of others, market irregularities, and more. Of course someone must do this arbitrage. I’m just not sure how lucrative this is for an investor.

5 Likes

@oslasho Yes, I think you get my point, it’s modern portfolio theory. The question is: Will adding a certain asset improve overall portfolio CAGR and/or Sharpe. The beauty of trend is: It’s been very much uncorrelated to both stocks and bonds (more so than gold or commodities). And yes, it lowers total portfolio vol, which is great for decumulation.

@Helix Take MFTFX, add 10-20% to your favourite portfolio instead of bonds, and then tell me if you like the results

Of course, I don’t like anything but stocks, but that’s not the point here. I need diversifiers because I’m heading towards FIRE. And adding bonds alone to my equity is far too risky imo, there’s inflation and interest rate risk people tend to forget. And I understand why: bonds have had an unprecedented run since the 80ies, combined with deflation. Of course, you don’t need trend, gold or commodities might do just as well.

And that’s all for now, need some digital detox ![]()

2 Likes

I do, but 10 years are not much for a backtest. Could simply be luck that it complements stocks nicely during the last decade. I mean longterm Treasuries are dubious in 40 year backtests. Interest rates have been going down since the early 80s, undeservedly skewing everything in their favor.

KMLM has longer data. Good looking one too. I might consider it after some further due diligence. Tracking error due to cost, and any strange risks (they are leveraged 3x), the profit of the strategy comes from absorbing risk during market panic.

Still, I’m very interested in how and why did you find this fund?

1 Like