I’m learning more and more about these options. Thanks a lot for all your explanations!

1 Like

Keep also in mind that, depending on the option “style” you may be assigned at any moment and not necessarily at option expiration… hence you won’t always have the time to buy back / roll or whatever action you may decide to undertake

This is the case for American-style options (most equity options belong to this category)

1 Like

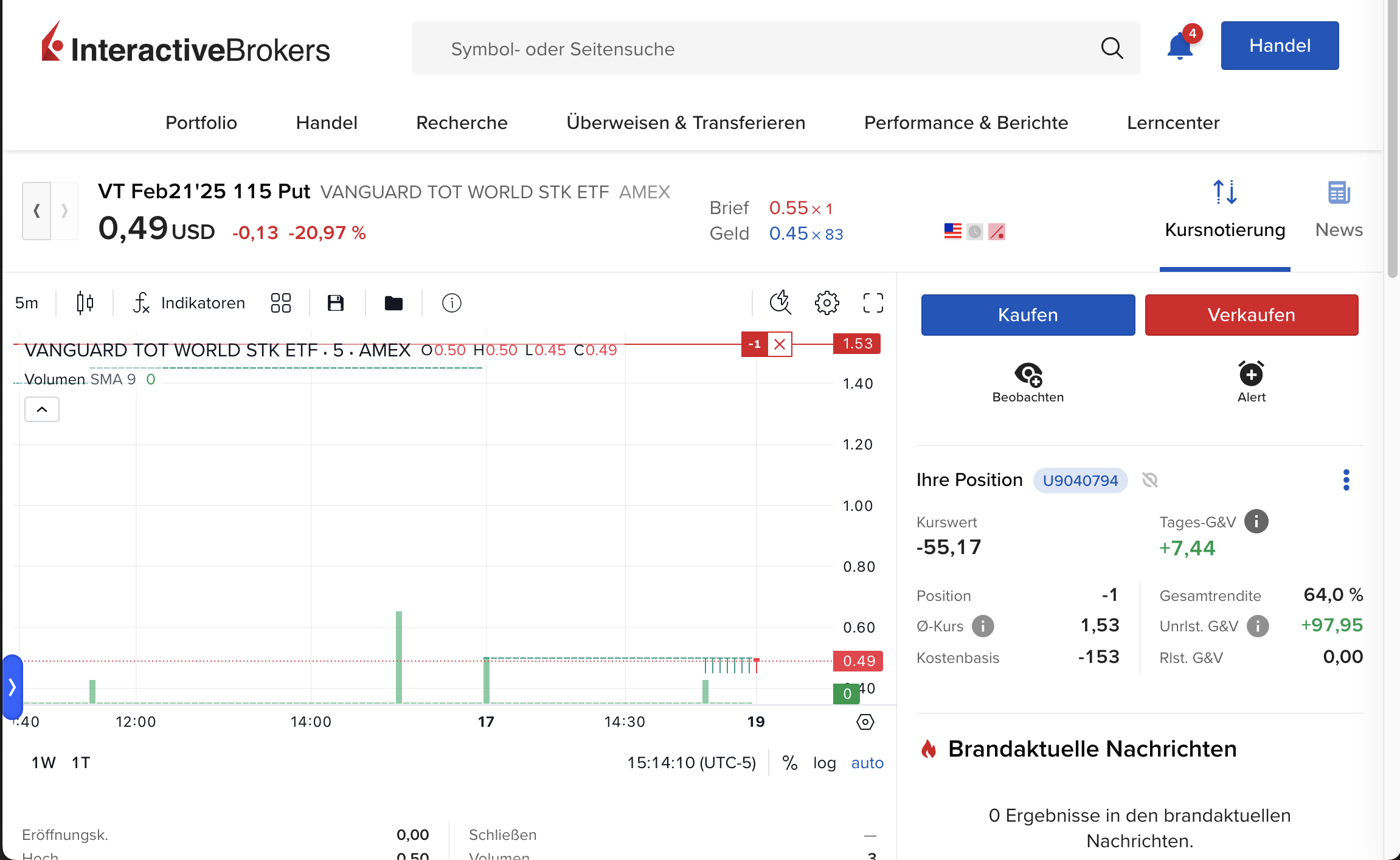

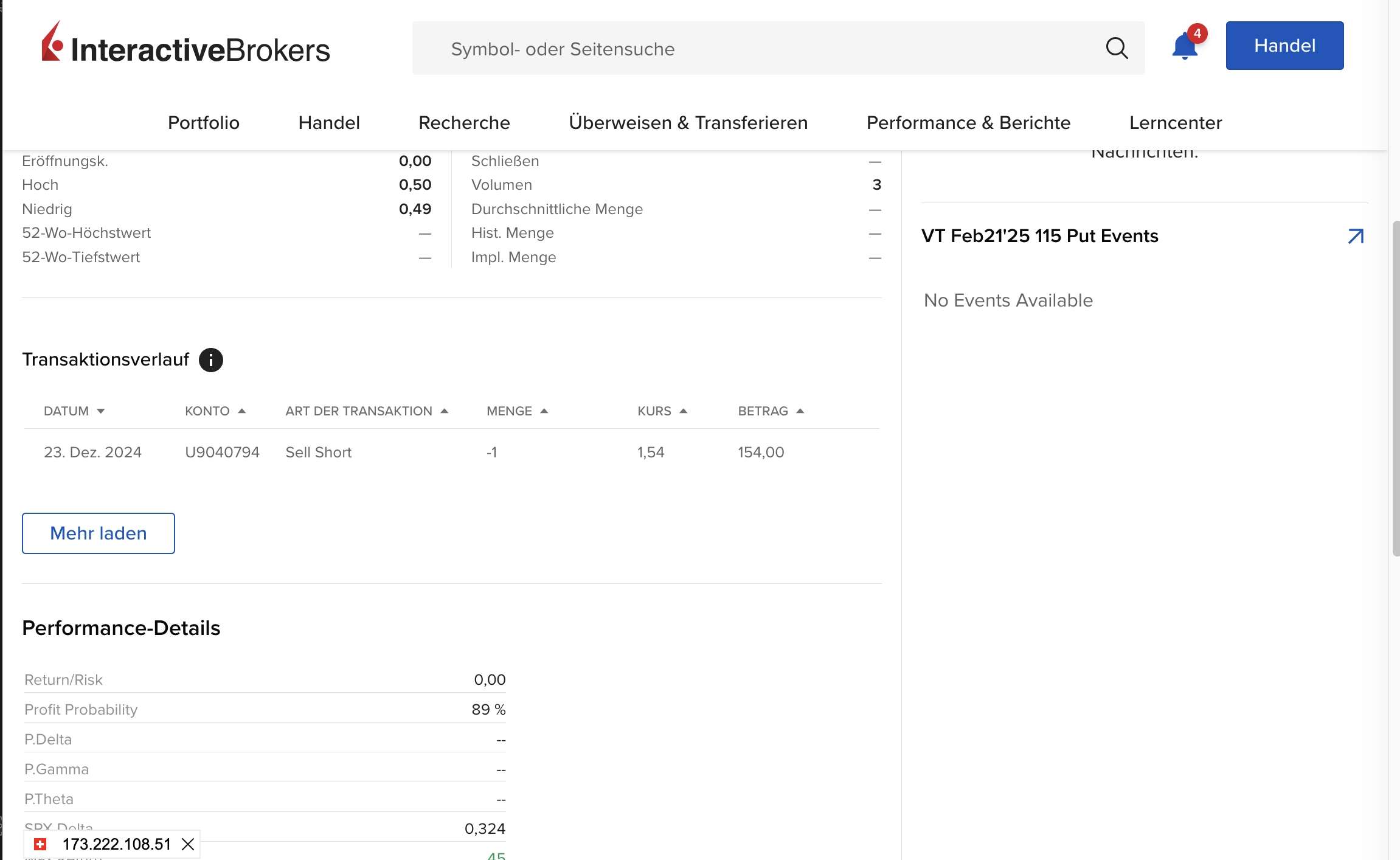

Thanks for this information. I am looking at the following option position but can’t find the style information. Can you tell where I can see this information?

1 Like

I also did search quite a lot in the past but didn’t find reliable information… it is not evident from the ticker

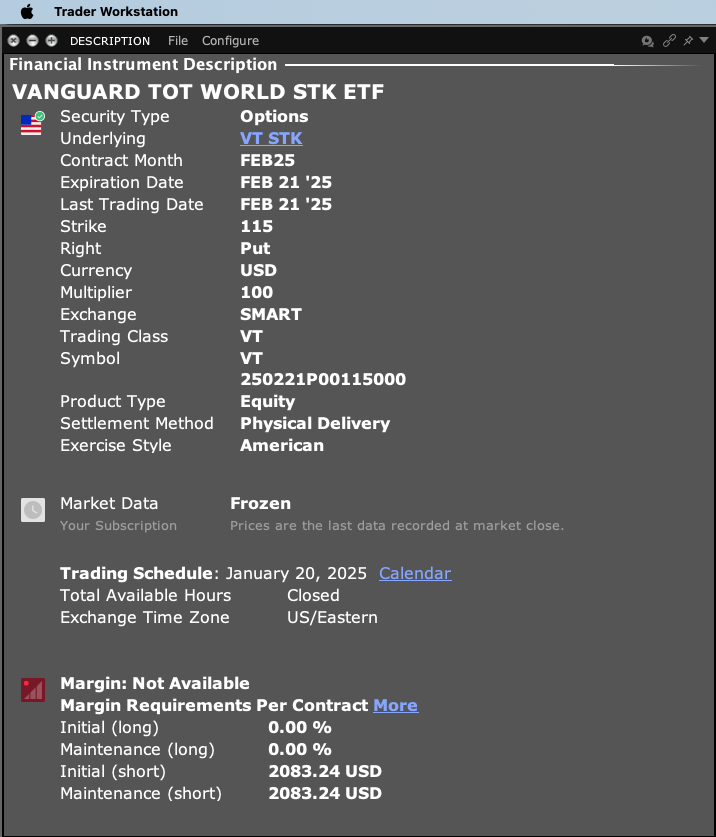

The only way I’ve found so far is through the IBKR TWS (cf. screenshot below, field ‘Exercise style’)

Happy to learn if there are other ways to tell ![]()

1 Like

On IB I would say TWS is the place to go to find those information, the web interface is not really a trading tool especially for options…

1 Like

I have a question at the experts for options. Since quite some time I use covered puts to buy shares at a price that I think is reasonable. I have done this with US stocks, US ETF like VT and swiss shares. So far so good. However, I would like to own now beside my RIO also BHT and I would like to buy it via covered call with a strike at 1800 pennies. as the UK shares are always in the weird “format” with pennies I have googled it several times what the “real” value in $ terms is.

Therefore, I came to 3 options which would make it 300 shares times 1800 pennies equal 540’000 pennies equal 5400 pounds which is approx. 7000 dollar. IBKR now shows me that the shares have a potential value of 700’000 dollar.

Is that just a calculation error from IBKR or did I mess up???

You mean cash-secured put?

A good indication would be the premium you received for the trade.

1 Like

You probably mean BHP (not BHT), that is traded at several stock exchanges, including London (LSE)

Yes, with LSE, there is a risk of mixed and unspecified units, between pounds and pennies; here, my interpretation is that the 540’000 pennies were converted to 700’000 cents, but the system “forgot” to convert from cents to dollars.

Perhaps you could check different user interfaces (TWS, mobile,…), they may show things in a different way…

2 Likes

Friends, it’s been nearly six months since my 2024 report. A lot has happened in the Trump market so far, but things have been slow in my options portfolio.

I’m still holding onto my 300 AMD, which were assigned last autumn at approximately $150, and I was assigned 100 NVDA at $129 in February. I also managed to sell 100 KO for a small profit.

My trading account (including $700 in cash) is now worth $48,600, still down from approximately $54,000 before the significant AMD drop last year.

During the tariff chaos in April, my maximum drawdown was 36% in Swiss francs. With AMD and NVDA considerably up in May, I was able to cautiously sell covered calls again (albeit at low premiums, i.e. $50-75 per week).

I’m going to stay the course, holding onto AMD and hoping for a prolonged recovery while selling far out-of-the-money covered calls. I should be able to sell NVDA at a nice profit soon.

My interim conclusion:

- Is options trading interesting and challenging? Yes, definitely!

- Is options trading a great source of low-risk additional income? Not really. Since I started in February 2023, the internal rate of return of the options portfolio has been 11.9%, while my “boring” ETF portfolio has made 8.6%.

6 Likes

Quick update:

- sold $3’145.76 worth of Puts in 2024.

Up until about May '24 they were cash secured. Then, they became Treasury secured (see my TSP topic dedicated to discussing this), which added another about 5% yield on the “cash sitting there” for the C in CSPs. - sold $1’790.23 worth of TSPs so far this year.

The lion share goes to a UNH Dec25 160P that I sold on May 15 for about $900. It’s currently worth about $200. I keep contemplating to buy it back already, but then again, UNH currently trades at over $300 … might as well sit on this put a little longer as I don’t see the underlying going to $160 anytime soon. - Uncle Sam dutifully paid back the Treasury I bought in May last year (which appreciated to the nominal, garnering about 4.5% in capital appreciation, and paying out the interest coupon of 0.25%, which I’ll have to pay income tax on). After it matured, I bought a new Treasury (a note expiring in February 2026, with a coupon of 0.5% this time).

So, still a side gig for me, and you might laugh at me, but I’m happy for the premiums collected.

Since my last update I also picked up a book which succinctly explains options (quite dense, not recommended for beginners), discusses trading strategies, but although I sympathize with the proposed option trading strategy of selling SPY put spreads, I haven’t implemented it myself so far.

2 Likes

Thanks for pointing out your TSP strategy. I’m actually contemplating holding BOXX instead of cash in my options account.

Wouldn’t that be easier than handling treasuries directly (wouldn’t even know what to buy exactly on IBKR…)

1 Like

I’d definitely try to hold “something-else-very-safe” instead of cash since IBKR doesn’t pay interest on the first $10k (and way below the Fed rate for the tiers above $10k).

Possibly. Not sure how BOXX is accounted for towards margin calculation since it’s a little bit more complicated than a Treasury and probably nowhere near as liquid.

Also, if you select Treasuries with really low coupons, you’ll be paid very little interest only … but the Treasury is still as rock solid and as liquid as it gets.

You launch the Bond Scanner in the TWS, pick instrument ‘US Treasuries’ and select your desired expiry end date and the coupon range you want to see.

It does not matter when the bond was issued. The only thing relevant is time to maturity and the coupon it pays.

If they have a low coupon, say 0.5%, you will be able to buy a $1000 Treasury for a lower price than the nominal to make up for the difference of the current overnight interest rate set by the Fed, i.e. say 0.97 x $1000.*

On the results list displayed you’ll also see the total yield you’ll make on a given bond, aka the yield through appreciation of the bond to the nominal and the interest you’ll be paid.

When you buy a bond, you’ll also have to pay the accrued interest (this is accounted for in the yield displayed). If a bond has a coupon of 4% and pays half-yearly with interest payments on Dec 31 and Jun 30, you’ll have to pay the seller 1% accrued interest if you buy the bond on Sept 30. That’s the part of the interest that belongs to the seller for the quarter of the year that the seller has owned the bond. You, the buyer, will get 2% on Dec 31 even though you’ve only owned the bond for a quarter year.

Other trading parameters behave the same way as with any instrument traded, e.g. low spreads mean high liquidity, etc.

I typically buy bonds with maturity in 9 months to a year out (to limit interest rate risk**) and pick the one with the lowest coupon within the maturity range I’m interested in, usually 0.25% to 0.5%.

[*] That’s why you typically want low coupon Treasuries as you’ll pay income tax on the coupon but not on the appreciation of the bond to its nominal.

[**] If the Fed hikes the price of your bond will go down. This isn’t an issue if you hold till maturity (but if you need to sell Treasuries because you got assigned a Put, your Treasury price will be a little lower than if the Fed rate remained constant). The further out the maturity of your Treasury, the larger the effect of the price falling on your Treasury if the Fed hikes.

And what about when at year end you have, say, tripled your account and you are not showing those options, ok, but they ask you to show how you got so much upside? When reporting on 31.12, do you show screens and send them already upfront? Or just the general screen or report of your situation vs. last year?

I send them the year end statement (not including any trades during the year), but unfortunately I have not tripled my account and have therefore avoided any pesky questions by the tax officers.

If you actually have tripled your account via options, I – as the Steuerkommissär – would probably take a closer look at your tax report, and, no offense, would probably look at the option – no pun intended – of classifying you as a professional trader.*

As mentioned before, if unsure, talk to the tax office directly, or get a tax consultant? You are most likely not going to get an answer here.

* Unless, of course, your income from derivatives was just a small, let’s say, single digit percentage (I am making this up as I write it) of your total income

This year for the first time I was asked by the tax officer to proof how my assets did grow that much more than my income would explain. They asked for documents of inheritance or whatever to proof where the money came from.

I did send them a mark-to-market performance and cash report from IB, cash to proof that I did not pay in cash. Options would show up there and are one point of Kreisschreiben 36.

In other words: if they don’t ask for it it is probably not worth it. If it is worth it they will ask for it. If you made a lot of gains with your stocks they probably will ask for proof and if you don’t keep your option business at a separate broker they find out.

2 Likes

So, digging further - do you have any knowledge how it looks like when someone is being qualified as professional investor, has to pay tax and insurance premium for that year, but then totally changes strategy. Can he be prof investor for 1 year only?

As per my situation, there is a lot of variety, so overall unrealised gains, realised, options, crypto etc. everything went much up + business as well. Options in this mix are fairly not much for 2024 (as an amount). But 2025.. is totally different and options are already besides other gains on top of the top in amounts.. But still.. I can prove them to be long-term hedges for me ![]()

Thanks for your explanations ![]()

I have no experience with that, as I fixed my trading rules according to Kreisschreiben 36, adhering to all 5 points.

But I suppose you can ask to be qualified as private investor again if you fulfill all those 5 points during a calendar year.

1 Like

When retiring I think everyone with a big stock portfolio violates the following rule?

“The realization of capital gains from securities transactions is not a necessity to replace missing or lost income for living expenses. This is regularly the case if the realized capital gains amount to less than 50% of the net income in the tax period.”

Yes, that one is difficult. I usually try not to take out more than the dividends. But the realization of capital gains may be a problem, even if it is immediately reinvested.

I usually sell the losers and keep the winners, but sooner or later winners have to be sold too. And I do partial sells to reduce risk. And obviously one day I will take out more money, what for should I be the richest man in the graveyard.

But then I live in Switzerland only a few months per year. My tax residency could switch to a country where capital gains are not taxed, but I would have to pay more tax on dividends then, 30% withholding. I just wait and see…

Hey, thanks for your detailed explanation! As I was able to sell 100 NVDA and 100 AMD, I bought BOXX for roughly USD 30k. So I’ll continue selling BSP (Boxx secured puts).

I’ll let you know about my experience (trading costs, distribution, taxes…)