Any specific reason for this ? It has lower TER and is more liquid.

You are right asking why not to do that with the other. It is for simplicity reason. I am ok to rebalance between 2 portolios, but I prefer not to do it with more. I also think in term US vs the rest of the world. I don’t mind having the EX-US grouped all in one. It is purely subjective.

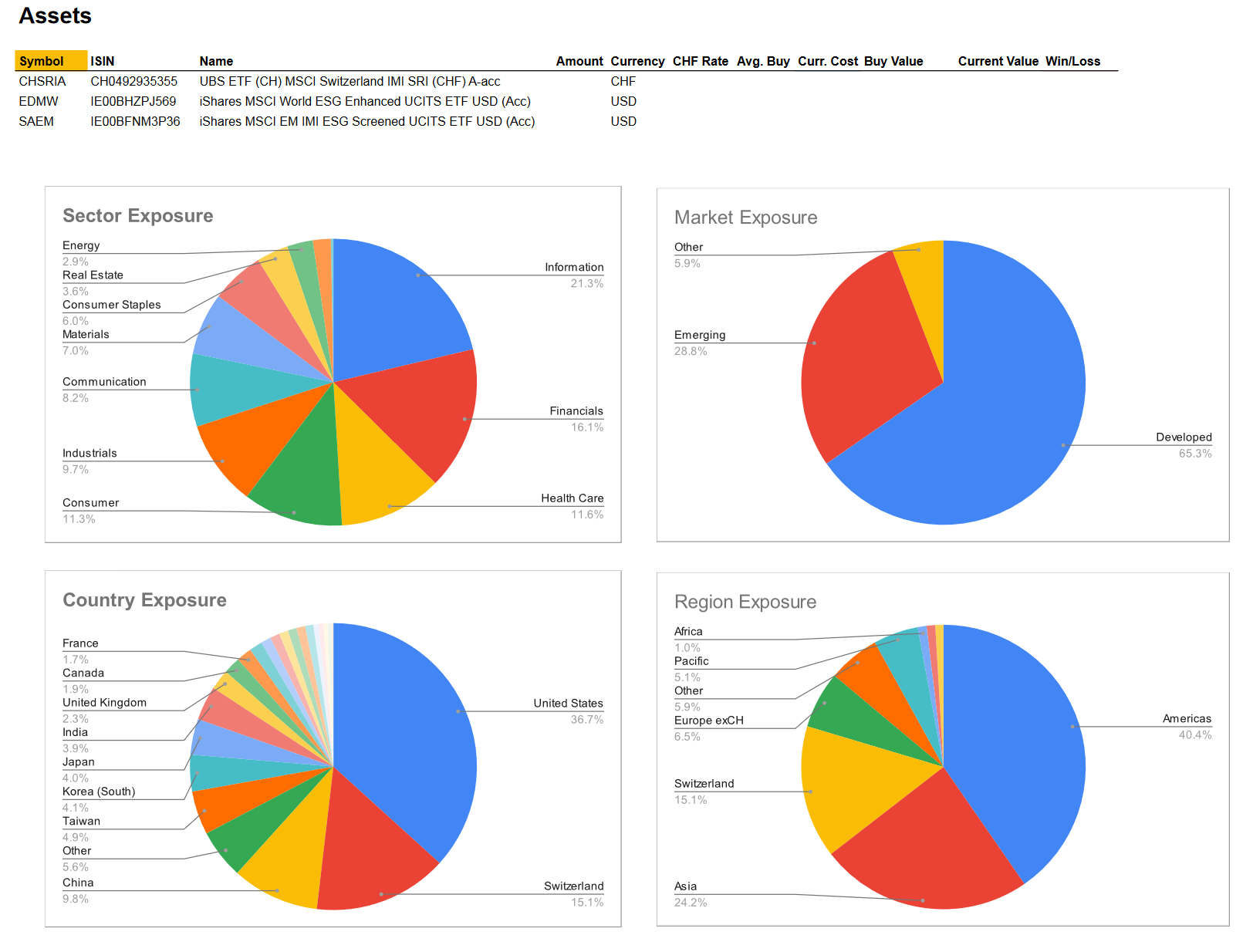

I currently completely ignored my 3a pillar VIAC in my strategy. (except for picking MSCI Switzerland IMI to complement the SMI ETFs in VIAC)

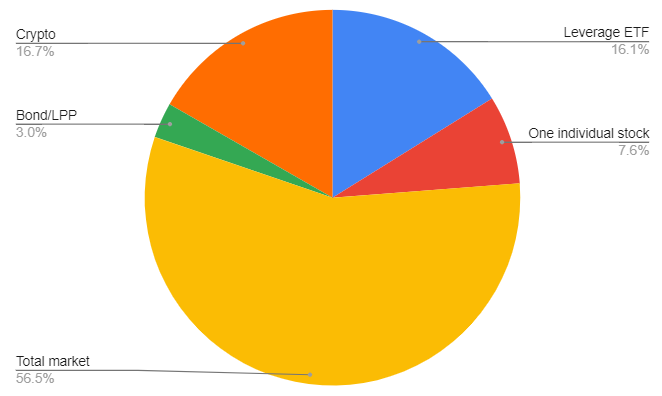

And of course my (currently still) large cash assets that I will need to shift into stocks over the next 6 months.

I will definitely increase my US/EU and EM positions and not any more Swiss stocks.

And also somewhere include my cash,bond,equity in my portfolio, to have a better overview of all my assets.

A pension fund has an asset allocation, they earn money on these assets, pay pensions, create reserves and so on. So inside it is a complex portfolio. But from outside, for you as a user, its function can be understood as that of bonds. You get some small, guaranteed non-negative return.

So a simple way is to count 2nd pillar as bonds allocation in your portfolio.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.