There are many ways to earn little interest with low risk. Most people here are not interested in this. There is a certain equilibrium in the financial system, efficient market or not. There are no miracles and no shortcuts.

What you are describing is just a complicated way to earn on cash deposits, and I am sure that after you calculate all costs, you are probably going to lose money.

Again, that is not the point I am trying to make.

The point I am trying to make is that a focus on TER and the Vanguard “brand” is not always a good idea.

I read here that V3AA @ 24 bps is a fair deal. I fail to see why.

The construction of a tracker does matter and influences its long-term performance. For example, XSPX is a synthetic ETF that tracks the S&P500 more reliably and with better returns compared to equivalent funds.

TER and Vanguard brand should not hide long-term underperformance.

On top of a misleading focus on the TER and the Vanguard brand in this forum, I often feel that there is an underestimation of financial engineering of tax optimization in accumulative synthetic funds; and as a consequence, an overestimation of the importance of tax.

I completely agree with you.

I am just saying that there are many parameters and that “just go for the cheapest distributing US Vanguard” might not be the best option for us

Those are not synthetic fund though (they tend to be in Luxembourg), right? I don’t think funds with physical replication can have much advantage compared to US funds, it’s basically the same structure.

Synthetic funds can potentially do a lot more, but it’s not always sustainable (tax authorities may revisit how they handle them and remove any potential tax advantages).

Edit: since it’s actually the exact same underlying fund, in your example the discrepancy is most likely due to a mismatch with the tax year vs. the fund reporting detailed data.

And also, just be aware that synthetic ETFs carry the additional credit risk vs the issuer(s) of the underlying swaps. Yes, they are likely to be collateralized, but when the shit hits the fan (which in this case would usually be a major systemic bank going down) it’s far from guaranteed that collateral covers the full exposure.

It might seem like a minor detail, but equal NAV doesn’t mean equal sensitivity to market changes. There’s bound to be a significant difference - no point in collateralizing an equity TRS with a basket of the same equities Without knowing which assets classes / quality are provided and against which haircuts (if any), difficult to say if it’s negligible or not under extreme stress.

The same holds for sec lending activities of course, in that you’re totally right.

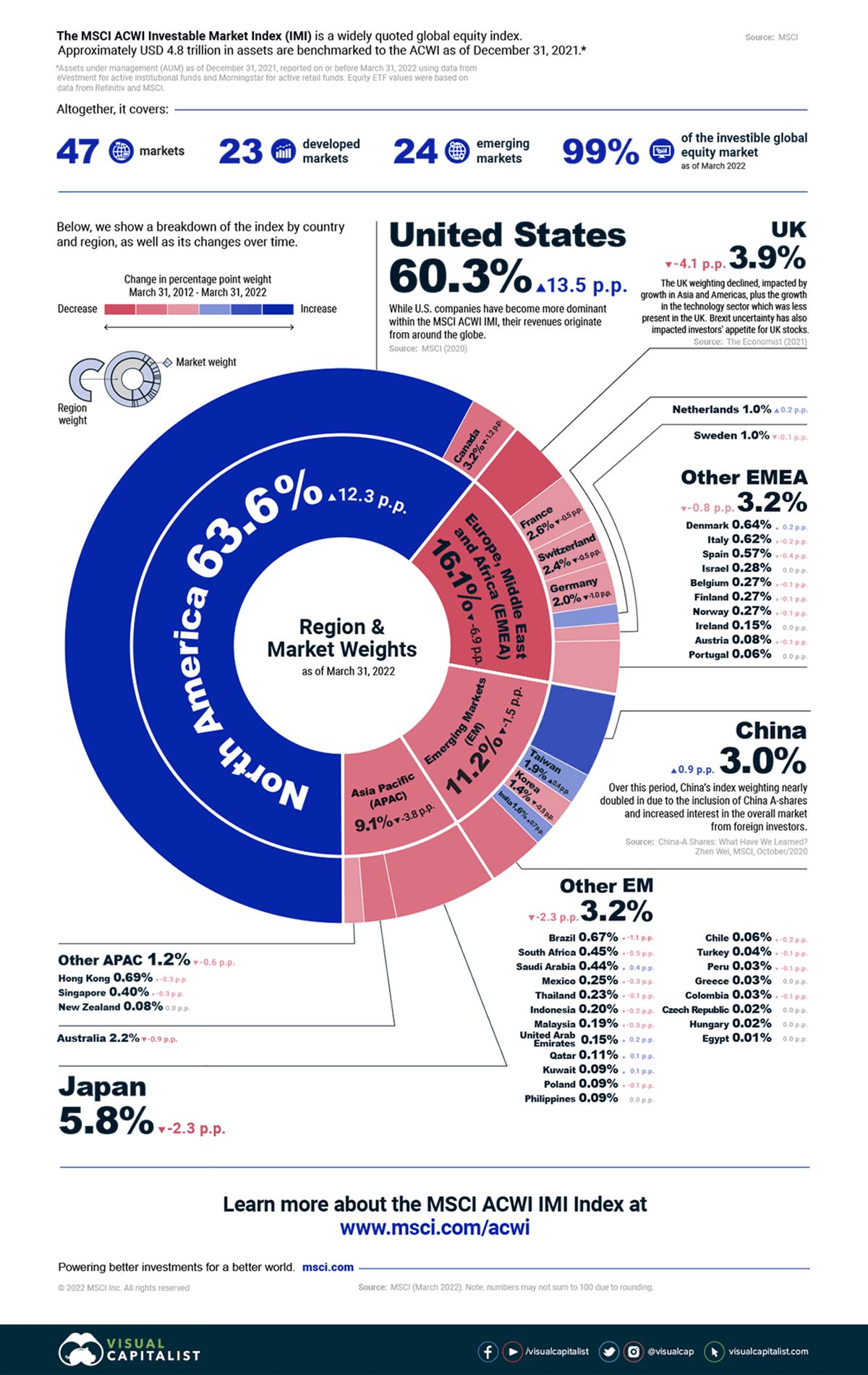

Thanks for the information. However, it’s important to note that this ETF tracks the MSCI ACWI IMI SDG Impact Select, which is substantially different from regular ACWI or ACWI ESG. The TER is 0.35% p.a. AUM is only USD 5 Mio.

No, SSAC is not currency-hedged. An ETF can be traded in various currencies without hedging. Also VWRL is never hedged and it’s traded in USD, GBP, EUR and CHF.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.